The launch of the S&P/ASX 200 ESG Index provides a transparent, rules-based foundation for market participants looking to reinforce their core while aligning investment objectives with their ESG values. S&P DJI’s Stuart Magrath joins SSGA’s Meaghan Victor to explore the data powering this innovative index and how its ESG framework influences risk/return.

https://www.youtube.com/watch?v=RS98nRdvaQY

Learn More: www.spglobal.com/spdji/since-2000

The posts on this blog are opinions, not advice. Please read our Disclaimers.

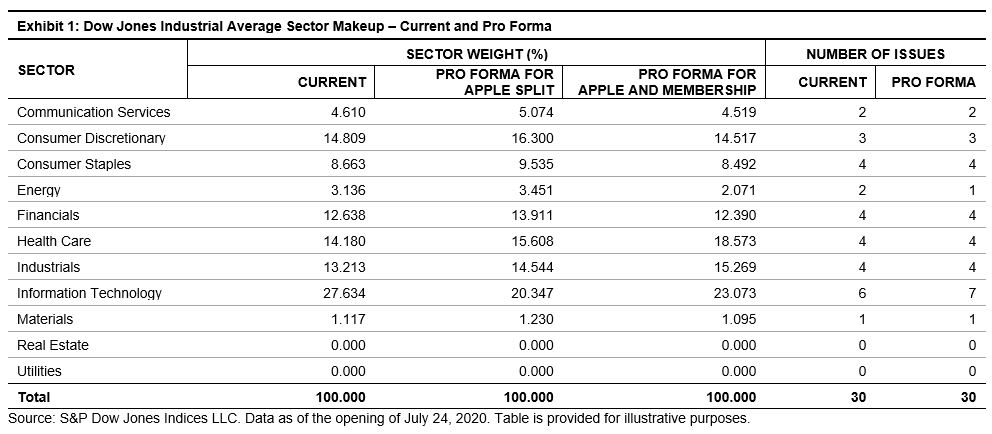

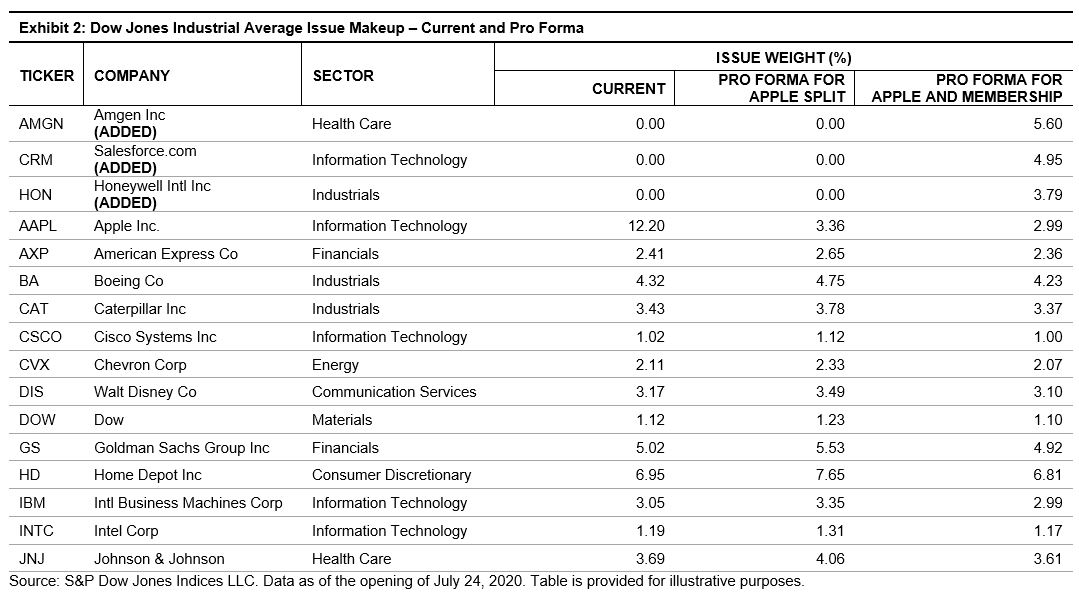

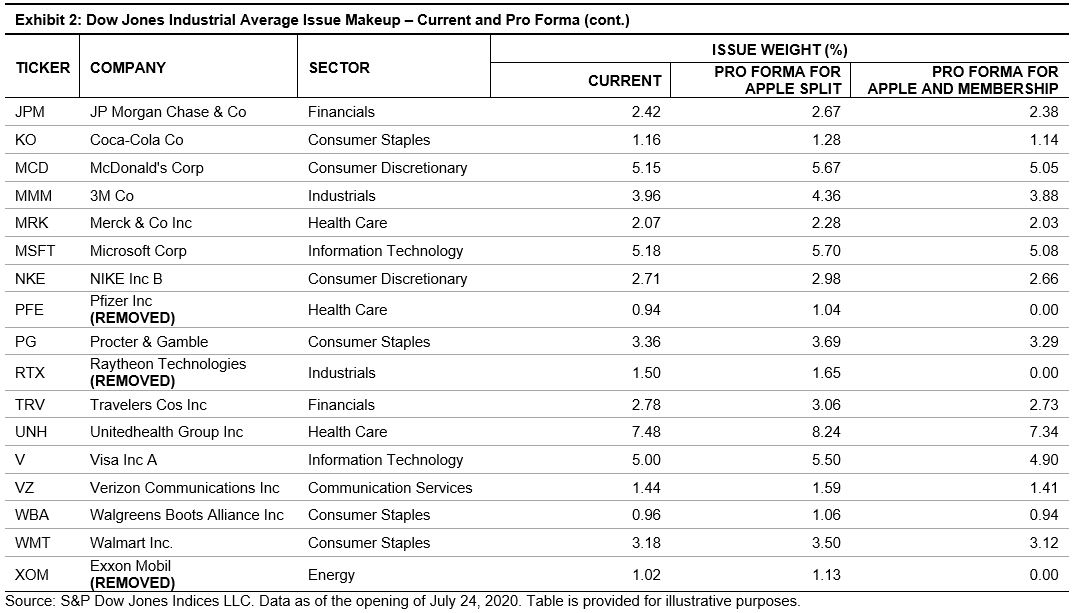

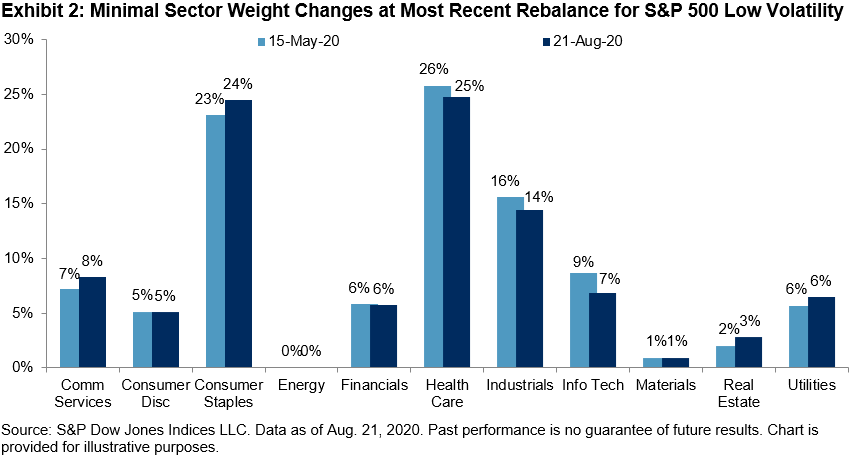

As a brief review, index modifications to the

As a brief review, index modifications to the