Recently, I read a comment that suggested we skip 2020 altogether. This new decade has not really started well—if only we could jump straight to 2021. Amid the overwhelming impact of the COVID-19 pandemic on public health and on the economy, perhaps what resonates best is that “this too will pass.”

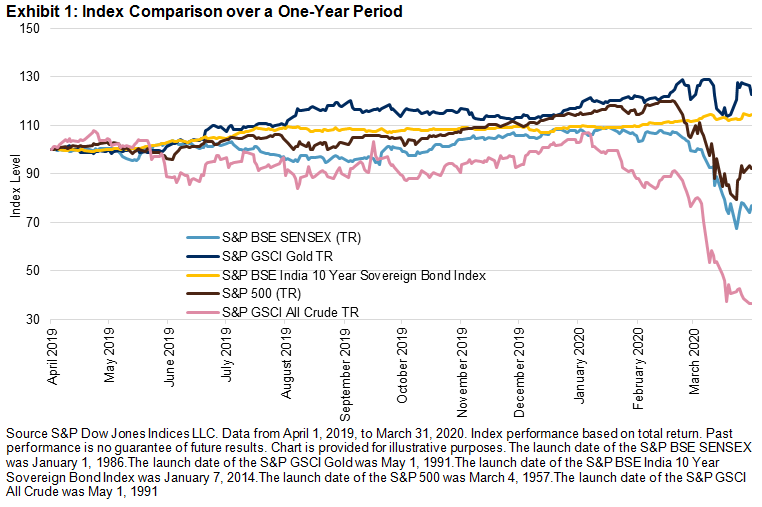

U.S. equities, which serve as a guidepost for the global economy, surpassed prior all-time highs in volatility. VIX®, also known as the “fear gauge,” has not reached similar highs since the global financial crisis (GFC) in 2008. The higher the uncertainty, the higher the option prices that are used to calculate VIX. The precipitous drop in oil prices following a price war between Russia and Saudi Arabia threatened a collapse of the Energy sector, adding to the uncertainty in the U.S. and globally. Unemployment in the U.S. continued to rise—in the last two weeks of the quarter, nearly 10 million Americans applied for unemployment benefits following the shutdown of thousands of businesses. It’s expected that this number is only a sign of further job losses to come and that unemployment filings will double in the coming weeks. Many impacted businesses are in the travel, entertainment, restaurant, retail, and real estate industries.

What about Latin America? Like a tsunami that started in Asia and then ravaged Europe, COVID-19 and its effects are now flooding the Americas. Despite the closing of borders and quarantines, the pandemic continues to sweep the continent. Governments have started to institute policies to minimize the public health and the economic impact. Similar to the U.S., which has approved a USD 2 trillion stimulus package to help mitigate the effects of the pandemic, Brazil has approved around USD 30 billion. Peru is also reviewing a similar package. In Chile, the president approved a USD 12 billion package. In Argentina, the World Bank will lend USD 300 million in emergency funds. Colombia and Mexico have not yet announced any major economic measures at this time. The question many ask is, will all this be enough? In the midst of uncertainty, the answer depends on how quickly the pandemic recedes and life goes back to normal.

According to S&P Global’s rating analysts, it is expected that the outbreak will push Latin America into a recession in 2020, recording its weakest growth since the GFC. They have also forecast that GDP will contract by 1.3% in 2020, before bouncing back to a growth rate of 2.7% in 2021. Finally, the length of the recession—although potentially worse in some countries—may be much shorter: only two quarters are projected versus six quarters during the GFC.[i]

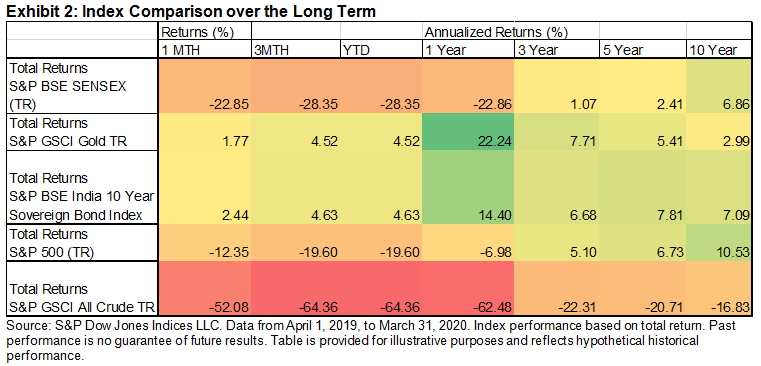

Latin American markets underperformed global markets during the first quarter. All gains from the previous years were completely wiped out. The S&P Latin America 40 posted the worst quarter on record, ending at -46% in USD terms. In comparison, the S&P 500®, which also had the worst quarter since 2008, lost 20%.

No economic sector was spared in the rapid downturn, as companies in important industries like energy, mining, and financials were hit hard. The average stock price drop for members of the S&P Latin America 40 was around -45% for the quarter. The Energy sector of the S&P Latin America BMI performed the worst among the 11 GICS sectors (-61%). Health Care had a difficult quarter (-45%), but thanks to its strong past performance, it lost a lot less for the mid-term periods.

Looking at individual markets in local currency terms, Argentina’s S&P MERVAL Index lost 41.5% for the quarter. Brazil and Colombia followed, returning -36% and -32%, respectively, as measured by the S&P Brazil BMI and the S&P Colombia Select Index.

In a sea of red for the quarter, in Mexico some indices were able to stay in the black. The S&P/BMV IPC Inverse Daily Index, which seeks to track the inverse performance (reset daily) of the S&P/BMV IPC, gained 23%. The following three indices also did well: the S&P/BMV MXN-USD Currency Index (26%), the S&P/BMV China SX20 Index (9.4%), and the S&P/BMV Ingenius Index (9.4%). The latter two indices are designed to measure international stocks trading on the Mexican Stock Exchange, and their strong performance is largely driven by the depreciation of nearly 20% of the Mexican peso relative to the U.S. dollar in Q1.

The first quarter is done, and the second quarter is looking gloomy. Comprehensive relief efforts are underway to help citizens and support our economies, and we can only hope for the best while we continue to tread carefully.

For more information on how Latin American benchmarks performed in Q1 2020, read our latest Latin America Scorecard.

[i] Elijah Oliveros-Rosen, For Latin America, The Path To Economic Recovery From COVID-19 Remains Uncertain, March 31, 2020.

The posts on this blog are opinions, not advice. Please read our Disclaimers.