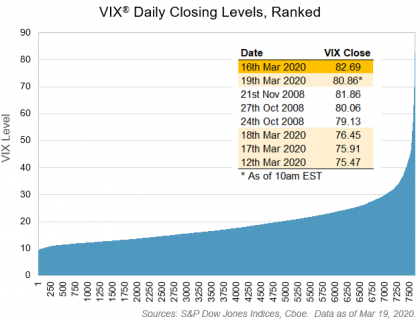

While ski resorts in the Northern Hemisphere were hampered by a mild end of winter, the downhill we are all experiencing has introduced a level of uncertainty and volatility beyond the slopes. The week of March 9, 2020, will go down in history as a time of unprecedented challenge and change. The spread of the COVID-19 virus globally led the World Health Organization to declare a global pandemic. Across the globe, governments and businesses have postponed or cancelled business travel, conferences, flights, festivals, sporting events, and political gatherings. Couple the pandemic with an oil price war between Saudi Arabia and Russia, and you’ve got your hands full.

The total return of the S&P 500® was down 22.9% YTD on March 12, 2020, at a value of 5,051.97, but it bounced back by 9.32% on Friday, March 13, 2020, returning -15.73% YTD. When comparing the total return equity performance to debt, investment-grade corporate bonds as measured by the S&P U.S. Investment Grade Corporate Bond Index returned -1.16% YTD, while the lower-rated S&P U.S. High Yield Corporate Bond Index was down 8.88% YTD.

For the month until March 13, 2020, the S&P 500 was down 8.13%, on a total return basis, while the S&P U.S Investment Grade Corporate Bond Index and S&P U.S. High Yield Corporate Bond Index returned -4.76% and -8.0%, respectively. Much of the return story can be found within the industry sectors of the underlying indices. The common theme among equity and fixed income sectors was the decline in energy. The S&P Global Oil Index lost 13.16% for the month as of March 13, 2020. WTI crude oil went from USD 61 per barrel on Jan. 1, 2020, to its current level of USD 30. Though the oil feud is between Saudi Arabia and Russia, the U.S. and its shale market are getting caught in the middle. U.S. shale firms announced a number of drilling and investment cuts that will negatively affect a number of energy businesses and their employees. Energy support companies that provide supplies, machinery, and exploration services will all be caught up in this downturn.

Exhibit 3 shows the option-adjusted spread (OAS) and the change in OAS year-to-date for each of the industry sectors for the S&P U.S. Investment Grade Corporate Bond Index and the S&P U.S. High Yield Corporate Bond Index. All 11 GICS® sectors for both indices widened out, resulting in higher yields and lower prices. The energy sector again clearly stands out among the sector comparison.

As the economy continues to suffer at the hands of the pandemic and oil shocks, fears of a recession increase with each day. The cancelling and postponing of global events should help curtail the spread of the virus, but the aftereffects experienced by small businesses, restaurants, retail, and employment will likely have a damaging effect for the foreseeable future.

The posts on this blog are opinions, not advice. Please read our Disclaimers.