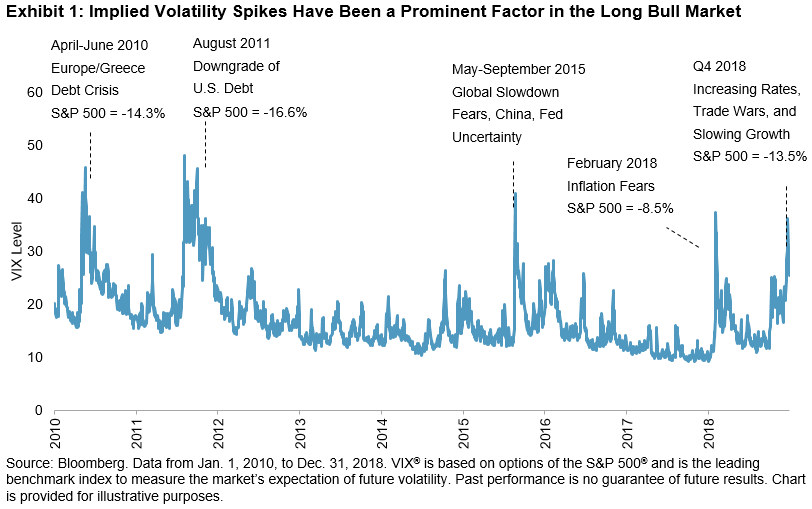

Fluctuating periods of “risk-on” and “risk-off” mean that spikes in equity market volatility and large drawdowns are increasingly common in today’s economy. Exhibit 1 shows events throughout the current market cycle causing notable rises in volatility and large drawdowns. With more of these likely in the future, as our long bull market cycle ages, how do investors best position portfolios to respond?

Many investors are familiar with the passive indices that exist to gain broad market exposure in a low-cost, liquid, and transparent manner. But one question worth asking is which passive strategies have the potential to outperform during periods of negative equity performance and increased volatility? The good news is there are several.

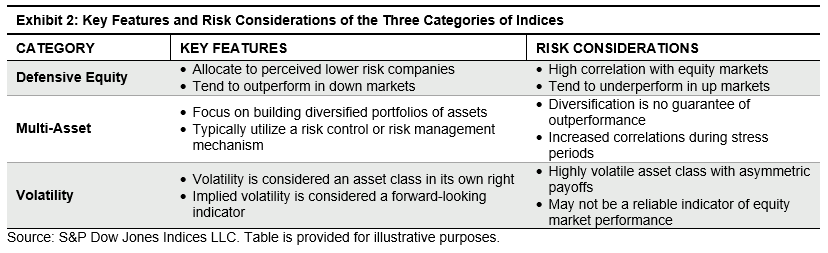

S&P DJI offers a variety of indices specifically designed to help smooth out equity market drawdowns and improve risk-adjusted return. These indices can be divided into three broad categories: defensive equity, multi-asset, and volatility.

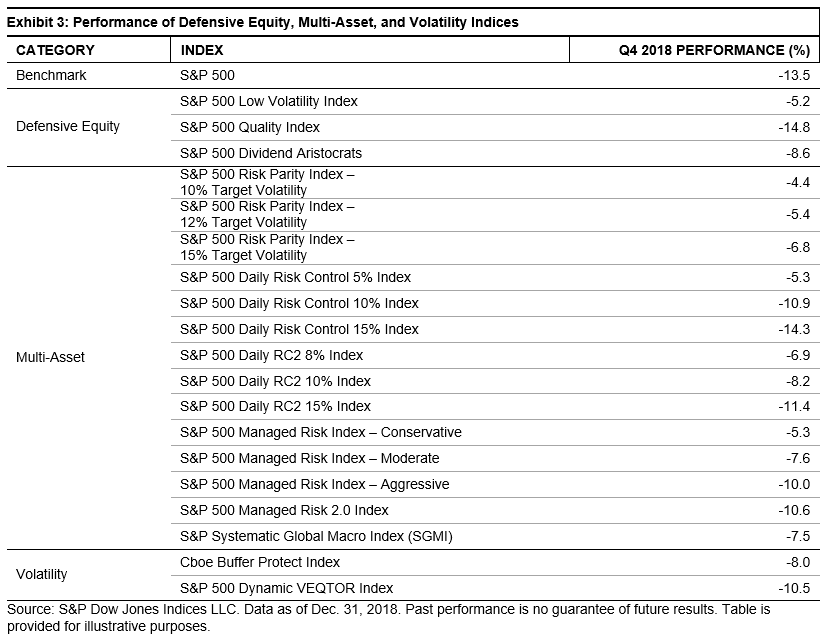

Exhibit 3 highlights and provides links to some of the indices that fall into these categories and shows their performance during Q4 2018—the most recent high volatility event. Many of the indices listed in Exhibit 3 posted material outperformance in Q4 2018.

Passive strategies can take on a much more dynamic role than simply offering broad market exposure. Investors can consider these strategies a valuable tool as they seek to weather periods of increased market volatility and large drawdowns.

For an overview of the indices shown in Exhibit 3, as well as an examination of their performance during other notable periods of increased volatility, please check out our new paper, “Seeking Volatility Protection Using Indices”.

The posts on this blog are opinions, not advice. Please read our Disclaimers.