On Monday, Oct. 29, 2018, Andrés Manuel López Obrador, president-elect of Mexico, announced that he would cancel the construction of the new airport in Mexico City, which had reached 30% completion. After a four-day unofficial referendum, in which less than 2% of the voters participated, the upcoming president (who will assume office on Dec. 1, 2018) decided to let people choose the future of the USD 13 billion project that was financed with public bonds. Markets did not respond well and Mexico took a big hit in all aspects: rates, currency, and equities.

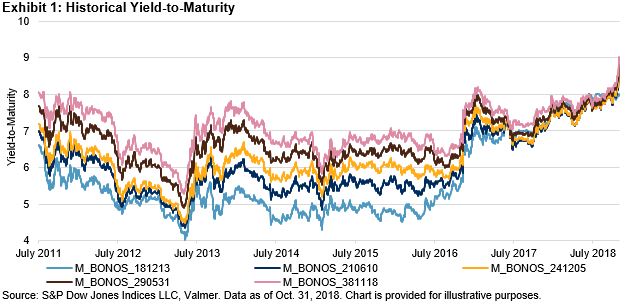

In terms of rates, the sovereign bond that matures in December 2024 widened 39 bps on Oct. 29, 2018, the third-largest one-day increase after the U.S. elections in November 2016 (when the bond increased 94 bps in two days), bringing its yield-to-maturity to an all-time high (see Exhibit 1) since November 2008, at 8.76% (as of Oct. 31, 2018). The nominal curve increased 88 bps on average and the real curve increased 58 bps for October, making the sovereign indices fall the most since November 2016 (see Exhibit 2).

As for currency, Oct. 29, 2018, marked the Mexican peso’s sixth-worst day in the past 10 years, with a depreciation of 3.6% against the U.S. dollar. The indices that follow sovereign and corporate bonds issued in U.S. dollars benefited from this depreciation, as shown in Exhibit 2.

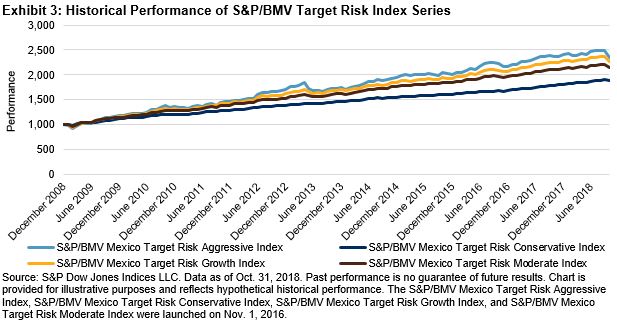

The third hit came in equity market, which marked its sixth-worst day as the S&P/BMV IPC—which seeks to measure the performance of the largest and most liquid stocks listed on the Bolsa Mexicana de Valores—fell 4.2%. Exhibit 3 presents the historical performance of the S&P/BMV Mexico Target Risk Index Series—which comprises four multi-asset class indices, each corresponding to a particular risk level intended to represent stock-bond allocations across a risk spectrum from conservative to aggressive—all of which presented their biggest monthly losses since February 2009.

I don’t know what will happen to the new airport, but if I were still to be in the Risk Management Department, I would use this event as a stress test.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

Source:

Source: