Market Conditions Indicator and price-to-rent can locate overheated metros

The S&P CoreLogic Case-Shiller Index has documented that home prices have risen in all metropolitan areas over the last few years. While price gains vary considerably across urban markets, some places have had especially rapid appreciation that put values above their pre-Great Recession peak, even after controlling for inflation. Examining the markets included in the 20-City Composite, all 20 markets are up substantially from their trough, 10 markets have surpassed their pre-Great Recession peak, and 5 have surpassed the earlier peak after inflation adjustment.[1] With prices setting new records, it’s natural to wonder whether the housing market is on the verge of another valuation bubble.

The CoreLogic Market Conditions Indicator provides a gauge to identify urban areas that may be overheating. The Indicator is based on straightforward intuition: home prices should generally rise in line with income growth of local residents. If prices grow too fast, then homes are less affordable and price growth should slow while incomes catch up.

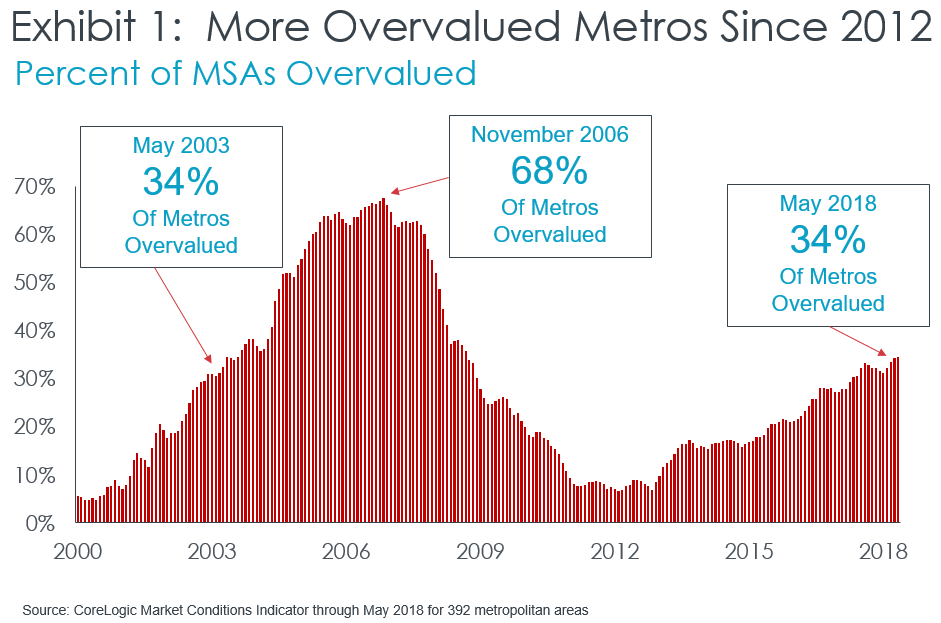

The Market Conditions Indicator found that 34 percent of MSAs in the U.S. were potentially ‘overvalued’ by this metric in May. (Exhibit 1) The last time that one-third of metro areas were overvalued in a rising price environment was Spring 2003. While many metros were frothy 15 years ago, the valuation bubble was still localized and not national; however, rapid price growth during the following three years led to 68 percent of markets overvalued by 2006. Thus, while we do not have a national valuation bubble today, continued rapid price growth raises the specter of a new bubble forming within the next few years. For metros that the Indicator has flagged as ‘overvalued’, it’s important to look at other metrics for confirmation. A price-to-rent ratio can provide additional perspective on whether prices are out of sync with valuation fundamentals.

To construct a price-to-rent ratio we used the S&P CoreLogic Case-Shiller Index and the CoreLogic Single-family Rent Index, set the ratio equal to one in the first quarter of 2001 when homes were fairly valued in nearly all metros, and observed how the ratio has evolved to today.[2] That ratio shows that home prices have grown more quickly than rent in most metro areas, which would provide confirmation of overheated values if cap rates had remained roughly the same, but they haven’t.

A cap rate is used by real estate professionals to convert net operating income on an investment property into a market value.[3] While a cap rate is relatively stable over short time periods within a metro area, cap rates will vary across metros and over a long period will fluctuate based on the level of long-term interest rates, the perceived riskiness of real estate investments, and tax code changes that affect real estate profitability. Of these three factors, the one that has changed the most between 2001 and today has been the level of long-term interest rates. Consequently, cap rates for single-family rental homes are down significantly since then. The cap rate decline implies that the price-to-rent ratio would need to grow by more than 60 percent since 2001 before today’s prices are disconnected with rental income fundamentals.

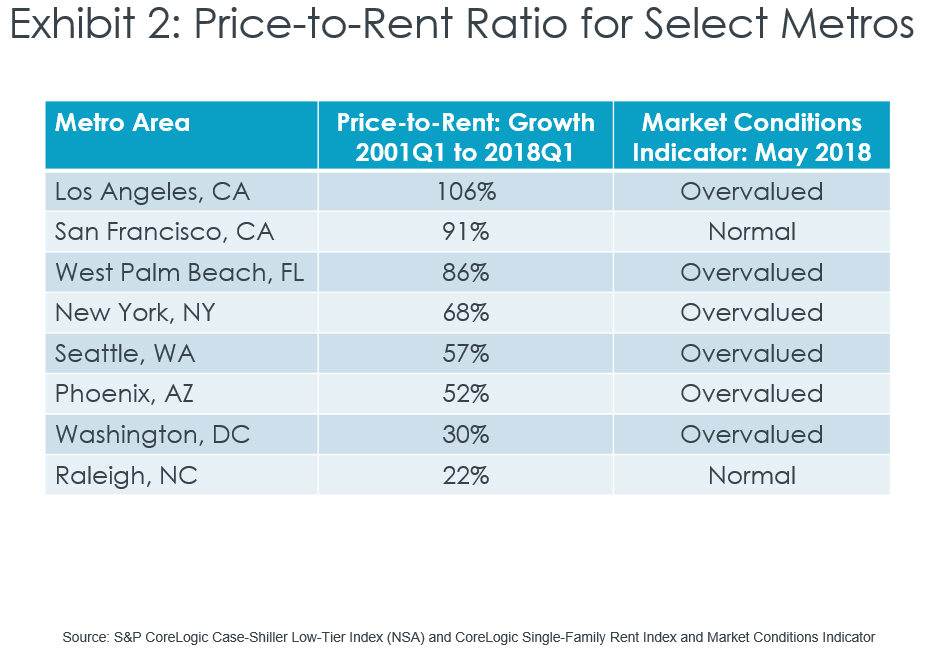

When we examined select metros that the CoreLogic Market Conditions Indicator found to be ‘normal’ in 2001, we found that price-to-rent ratios were up by more than 60 percent in the Los Angeles, San Francisco, West Palm Beach and New York metros; of these, all but San Francisco were places that the Indicator had flagged as overheated today (Exhibit 2). Metro areas that the Market Conditions Indicator has tagged as ‘overvalued’ and have a high price-to-rent ratio are at heightened risk of a value correction, especially as long-term interest rates rise.

[1] The Bureau of Labor Statistics’ Consumer Price Index all items less shelter was used to adjust for inflation. Of the places included in the 20-City Composite, Dallas, Denver, Portland, San Francisco and Seattle have real prices above their pre-recession peak, as measured by the S&P CoreLogic Case-Shiller Index.

[2] Because single-family rental homes have a median value that is less than the median value of all single-family homes, the calculations used the S&P CoreLogic Case-Shiller Low-Tier Index (not seasonally adjusted) for homes with a purchase price within the lowest one-third of the CBSA price distribution.

[3] Market value of a rental home = (Net operating income)/(Capitalization rate)

The posts on this blog are opinions, not advice. Please read our Disclaimers.