Did you know there is now about $620 billion more of student loan debt than total U.S. credit card debt?

Here are some more astounding statistics highlighted in our new paper:

- The average student loan debt for 2017 graduates was $39,400, up 6% from the prior year.

- About 44 million borrowers owe a total of $1.48 trillion in student loan debt.

- In the past 3 decades (adjusted to reflect 2017 U.S. dollars):

- A 1988 graduate of Harvard University would have spent $17,100 on tuition during their senior year. Now, they would have to pay $44,990 in tuition for their child to attend Harvard, a markup of 163%.

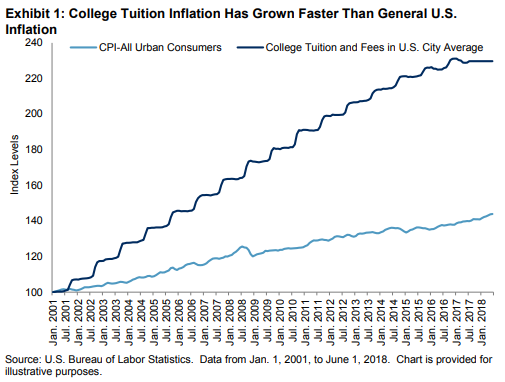

Costs associated with college tuition and fees, as measured by the U.S. Bureau of Labor Statistics, have far outpaced general U.S. inflation as measured by CPI (5.9% versus 2.6%, annualized from January 1987 to June 2018; see Exhibit 1). So for individuals saving for college, growing assets on pace with tuition inflation is possibly challenging without a college inflation protection security.

Unfortunately, most market participants saving for college only have some combination of the available investments today, perhaps in a 529 plan or “qualified tuition plan” that are made up of just traditional stock and bond funds.

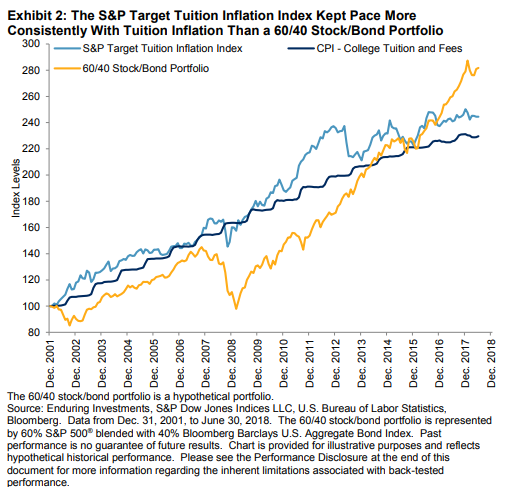

In response to this, S&P Dow Jones Indices partnered with Enduring Investments to develop the S&P Target Tuition Inflation Index, which comprises underlying inflation bond, corporate bond, and equity indices and is designed to reflect changes in college tuition and fees over long term periods.

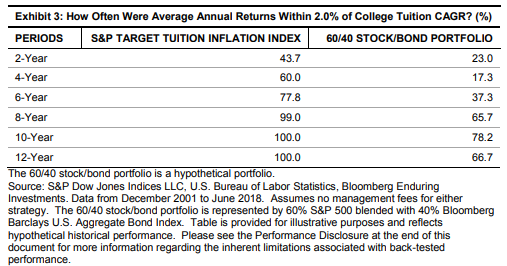

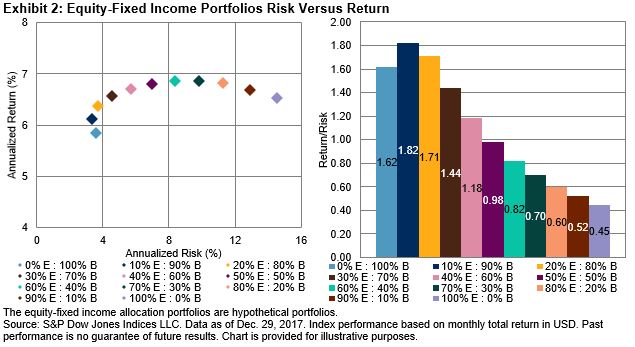

Over longer time periods, the likelihood of tracking tuition inflation with the S&P Target Tuition Inflation Index increased. For example, when two-year periods were measured, the index only tracked the College Tuition and Fees U.S. City Average CPI within 2% during 43.7% of the period studied. When the time periods were lengthened to over eight years, the index tracked within 2% of tuition inflation nearly 100% of the time. This was a significant improvement over a typical 60/40 stock/bond mix that is usually intended to provide better risk-adjusted returns. Since most of the contribution to risk in the traditional 60/40 stock/bond allocation comes from equities, its tuition inflation matching capability was comparatively volatile.

Not only will the traditional mix by definition decline with falling equities, but an acceleration of general inflation may adversely affect the performance of equities and bonds. Also, in a declining equity environment, tuition inflation will likely accelerate, partly driven by rising general inflation plus demand growth for education, as well as endowment and appropriation underperformance.

Please stay tuned for Part 2 of this series that will describe the theory behind how the index keeps pace with tuition inflation. If you can’t wait, it is all posted now in our research here.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

Source: S&P Dow Jones Indices

Source: S&P Dow Jones Indices