In prior blogs,[i] we discussed the return contribution of mega-cap securities in 2017, as well as the impact of style classifications that may give small-cap active managers more autonomy to invest in significantly different risk exposures. In this blog, we look at active factor risks taken by active managers across three market-cap ranges against the appropriate S&P DJI style benchmarks.

Using the aggregate holdings of the managers[ii] and the Northfield US Fundamental Equity Risk Model, we observed the managers’ active exposures to systematic risk and whether those factor bets were rewarded.

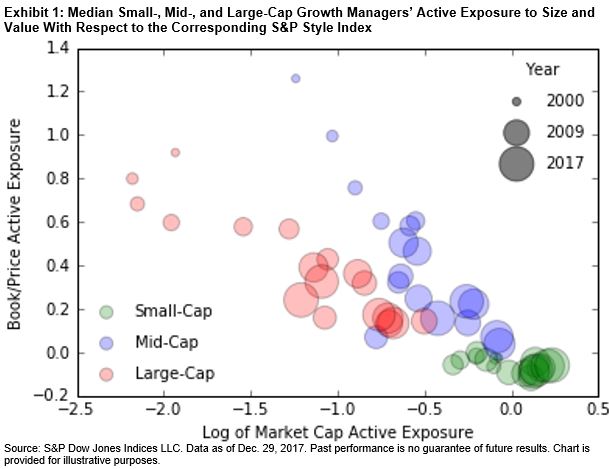

Exhibit 1 shows the median fund’s[iii] active exposure for both book/price and log of market cap, which serve as the proxies for value and size factors, respectively. Funds have noticeably shifted their exposures to those two factors over the past 18 years.

For example, across all three market-cap categories, the median fund started the 2000s with a negative active exposure to size. In other words, the median active fund was invested in companies that, in general, were smaller than that of the respective benchmark. However, over the years, the median active fund’s exposure to size has increased across all market-cap ranges, as shown by the increasing bubbles. By the end of 2017, active exposure to size for mid- and small-cap managers was roughly in line with that of the respective benchmark.

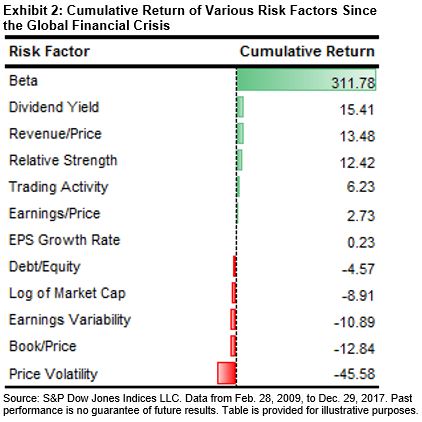

Undoubtedly, the longest-running equity bull market we have been experiencing since the 2008 global financial crisis influenced this gradual shift to neutral weight in the market-cap factor that we observed in actively managed funds. As market-capitalization-weighted benchmarks increased their index values, and with market beta responsible for 312% of average benchmark return (see Exhibit 2), active managers could not afford to have a sizable underweight to the market factor or a significant overweight to the size factor.

Similarly, active exposure to the value factor has also been converging to that of the benchmark. Both mid- and large-cap funds started the evaluation period with high active exposure to book/price. This equated to the median fund investing in companies that were more “value-like” or “cheaper” than their benchmark. By the end of 2017, however, they had a marginal positive active exposure to the value factor.

It is worth noting that the value factor performed rather poorly over the period from Feb. 28, 2009, until Dec. 29, 2017. Based on the Northfield US Fundamental Equity Risk Model, book/price returned -12.84% over this period. Among the five Fama-French factors, the value factor—as represented by high minus low portfolios formed by book/price ranking—returned -12.83% over the same period, compared with 37.95% delivered by the profitability factor.

It remains to be seen whether the size factor or the value factor will continue their performance cycle. One thing we can be certain of, based on the factor exposures of actively managed funds, is that active managers have displayed dynamic exposures to size and value factors, gradually shifting from active underweight to a more neutral position over time. That dynamic shift was in line with the performance of those factors.

[i] The Impact of Size on Active Management Performance in 2017: Part 1 and The Impact of Style Classification on Active Management Performance in 2017: Part 2.

[ii] Fund holdings were sourced from FactSet’s Ownership database on a monthly basis for all available funds within the CRSP dataset. The funds that met the style criteria were then pulled out for this analysis.

[iii] On a monthly basis, the benchmarks’ factor exposures were subtracted from each fund’s factor exposures to arrive at the active exposure. The funds were then averaged across each factor and year to create an average yearly active factor exposure for each fund. The median within each market capitalization, year, and factor was then presented in Exhibit 1.

The posts on this blog are opinions, not advice. Please read our Disclaimers.