The S&P 500® is widely considered one of the best single gauges of the U.S. equity market. Composed of 500 companies that are domiciled in the U.S., the index captures approximately 82%[1] of the total U.S. equity market value. An index of U.S. companies may lead one to assume that the index is only reliant on the health and growth of the U.S. economy. In reality, the index is much more global than that. Many U.S. corporations have a global presence, with assets and revenues in foreign markets. Therefore, global market events and economic shocks can have a material effect on S&P 500 companies, thus overall index performance.

To better understand where S&P 500 companies’ revenues are coming from, we used the FactSet Geographic Revenue Exposure (GeoRevTM) dataset,[2] which gives a geographic breakdown of revenues for all companies with available data, down to the country level. Since there are no standardization rules for the reporting of geographic revenue segments, the dataset uses a normalization/estimation process to assign revenues to specific countries. The ability to have detail of revenues at the country level is an important tool in understanding potential country exposures or risks for a company or index.

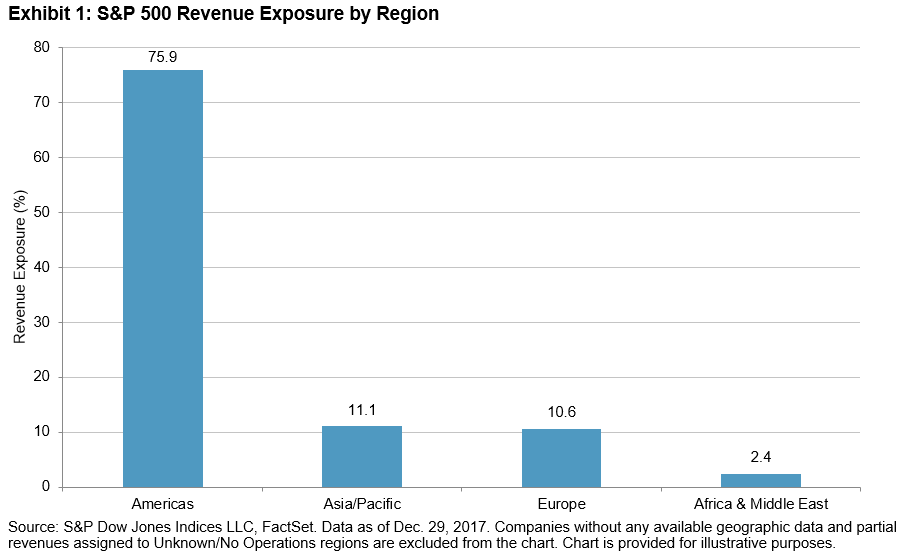

We first look at total revenues at the regional level (see Exhibit 1). The Americas region, which combines the North and South American continents, is unsurprisingly the largest regional exposure, at 76% of total revenues. The Asia Pacific region (11.1%) and Europe (10.6%) follow in terms of total revenue, with Africa & Middle East having the lowest total revenues, at 2.4%.

At the country level, nearly 71% of S&P 500 revenues comes from the U.S., with the remaining coming from foreign markets. Internationally, the largest individual countries by total revenue include China (4.3%), Japan (2.6%), and the UK (2.5%).

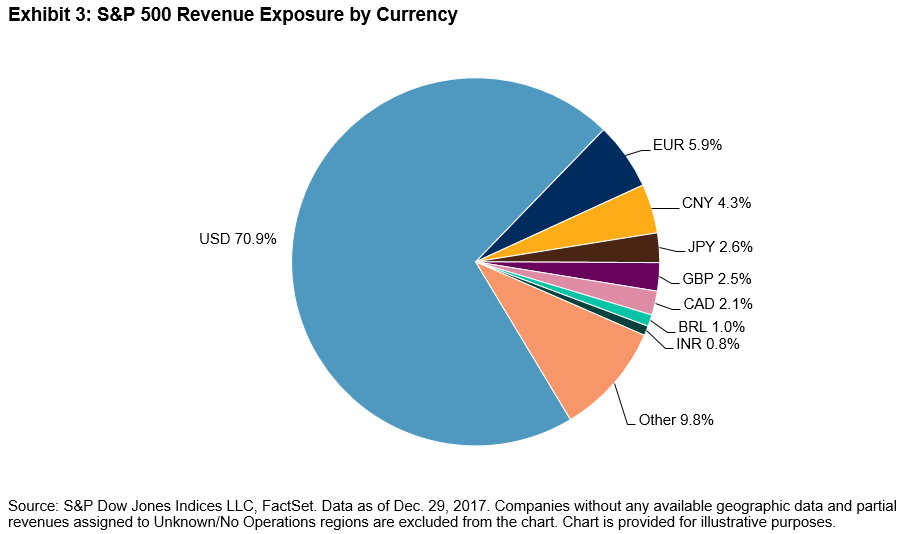

Given the diverse mix of countries, it is important to examine the potential foreign currency exposure of the S&P 500, which we determined by mapping the currency used in each country (see Exhibit 3). Several additional observations can be made from the currency-based revenue chart. First, it shows that the euro is the foreign currency the S&P 500 has the most exposure to, coming in at 6%. Second, the chart shows the number and the mix of currencies the S&P 500 has exposure to—six foreign currencies with a total exposure of 1% or more and 19 currencies coming in at a minimum of 0.25%.

Given the results, we can see that the S&P 500 has meaningful exposure to foreign markets. As such, events both domestic and globally, as well as policies that change the dynamic between the U.S. and other foreign markets, can potentially have an effect on the S&P 500. In future posts, we will look at how the global market exposure of companies in the S&P 500 affect the performance of the index.

[1] Source: S&P Dow Jones Indices LLC. Calculation as of Dec. 29, 2017.

[2] More information on the dataset can be found here: https://www.factset.com/data/company_data/geo_revenue

The posts on this blog are opinions, not advice. Please read our Disclaimers.