For many years, active fund managers and institutional investors have often used a factor-based approach either to strategically construct portfolios or to tilt their portfolios toward well-known risk factors, such as low volatility, value, momentum, dividend, size, and quality, to capture the factor risk premium. Investors seeking to identify skilled active managers look to dissect fund performance into returns generated from factor exposures and alpha that is attributable to fund manager skill, which in turn should affect fund flows.[1]

An analogy[2] used to explain this concept associates factors to nutrients and stock returns to food items. Different food items (such as pulses, milk, vegetables, bread, burgers, pizza, etc.) contain nutrients (such as carbs, vitamins, proteins, fats, minerals, etc.) in varying proportions. Similarly, a stock’s risk/return characteristics can be thought of as being explained by different risk factors. A factor index looks to bucket stocks with similar risk/return characteristics. Extending this analogy, different individuals (e.g., an athlete versus someone with a desk job) have different nutrient requirements, therefore they would consume different combinations of food items. Similarly, investors with different risk appetites would allocate accordingly to different factors to generate returns. For example, an investor who is keen on a low risk or defensive portfolio would potentially look to allocate a higher proportion to low volatility and quality factors, whereas as an aggressive investor might look to add exposure to value and size (small-cap) factors. Factor-based investing provides a route to objectively capture inexpensive companies (via value factors) or companies with robust balance sheets and steady returns on equity (via quality factors).

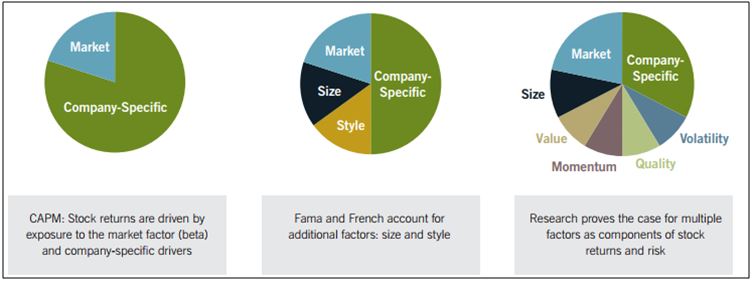

The first model that initiated the conversation on factor investing was the Capital Asset Pricing Model (CAPM) suggesting that a single factor—market exposure—drives the risk and return of a stock. The CAPM suggested that returns that were unexplained by the market factor were idiosyncratic or company-specific drivers. Gradually, the Fama-French Model looked to account for additional factors such as size and value, in addition to broad market returns. Follow-up research by Carhart and Pastor-Stambaugh yielded two new factors, viz momentum and liquidity, respectively. As academic research evolved, newer factors, such as growth, quality, dividends, and volatility, were thought to have attributed to stock returns as well.

Exhibit 1: The Evolution of Factor-Based Investing

Source: Fidelity Investments.[3] Chart is provided for illustrative purposes.

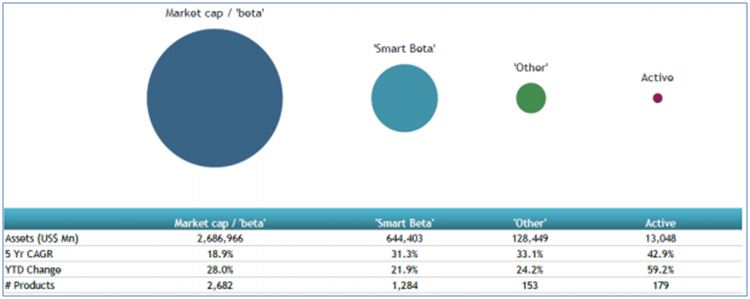

Factor-based investing can be implemented passively with the aid of factor indices aiming to provide exposure to specific factors, following rules-based methodologies, which tend to be more cost effective and transparent than actively managed portfolios. Globally, smart beta products have gained tremendous popularity with smart beta equity ETF/ETP assets, seeing an AUM growth of over 31% CAGR to USD 644.40 billion for the five-year period ending in September 2017. Smart beta ETFs/ETPs account for almost 19% of all equity ETF/ETP AUM as of September 2017.

Exhibit 2: Market Cap Beta Versus Smart Beta

Source: ETFGI.[4] Chart is provided for illustrative purposes.

Factor indices are not designed to replace market-cap-weighted indices. Broad-based or market-cap-weighted indices represent the entire investable opportunity set for market participants. They aim to capture long-term equity risk premium with low portfolio turnover, high trading liquidity, and large investment capacity. Factor indices look to capture targeted risk premia following a rules-based and transparent index methodology. Not only is the stock selection for these indices based on specific factor criterion, but the stock weights are also related to the stocks’ factor scores, which are used to create factor tilts within the index portfolios. In contrast to passive products based on broad-based indices, factor-based strategies can provide an opportunity for market participants to express their active views away from market-cap-based portfolios. Thus, like active funds, factor performance should be evaluated in the long run against a market-capitalization-weighted benchmark.

Please refer to Factor Performance Across Different Macroeconomic Regimes in India for more information on this research paper.

[1] Barber, B., Huang, X. and Odean, T. (2017). What Risk Factors Matter to Investors? Evidence from Mutual Fund Flows. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2408231&rec=1&srcabs=2038108&alg=1&pos=9

[2] https://www.blackrock.com/es/literature/brochure/factor-investing-unlocking-drivers-of-return-en-lai.pdf

[3] https://www.fidelity.com/bin-public/060_www_fidelity_com/documents/brokerage/overview-factor-investing.pdf

[4] https://www.researchpool.com/download/?report_id=1570482&show_pdf_data=true

The posts on this blog are opinions, not advice. Please read our Disclaimers.