It is interesting and amazing to see how people react to natural disasters. Whether it be a hurricane, flood, tsunami, earthquake, and no matter where the disaster is located, the whole world takes notice and helps with anything they can. This was certainly the case for Mexico after the 7.1 magnitude earthquake that shook the capital on Sept. 19, 2017 (12 days after an 8.2 earthquake in the country, and exactly 32 years later after the most significant and deadliest earthquake to hit Mexico City), where thousands of Mexicans took to the streets to help in some way. Troops from around the world (Chile, China, Colombia, Costa Rica, Ecuador, El Salvador, Spain, Guatemala, Honduras, Israel, Japan, Panama, and the U.S., among others) collaborated in search and rescue efforts in the aftermath. We, and I believe all Mexicans, are very grateful to the people that helped and are still helping—thanks so much to all of you.

But the most amazing part is that the generosity was not only that of the people, but companies from sectors like telecommunciations and transportation also helped for eight days by not charging fees for internet, telephone services, public transportation, and many toll roads, and this contributed to a 0.31% drop in year-over-year inflation for September 2017 after 14 consecutive months of increases. Exhibit 1 shows the history of annual CPI over the past 10 years.

Exhibit 2 shows the performance of Mexican inflation-linked bond indices in different periods, and we can see how in the one-month window, the short-term end of the curve saw gains, while losses were observed in the middle and long term.

If you were wondering how inflation behaved after the 1985 earthquake, Exhibit 3 shows inflation from 1980-1990, where we can see that inflation rose for 15 consecutive months after the earthquake—but it’s difficult to make a conclusion based on that data, since during that time Mexico had severe hyperinflation problems.

Now that we have talked about natural disasters, there is an imminent “natural disaster” with the NAFTA negotiations. Over the past 22 days (from the Sept.19, 2017, earthquake through Oct. 11, 2017, as the fourth round of negotiations begins) the Mexican peso depreciated 5.37% (almost MXN 1) against the U.S. dollar. Exhibit 4 shows the performance of the UMS index series, and we can see how over the past month, the currency’s depreciation has helped in the performance of these indices, and in some cases it has evened out YTD losses.

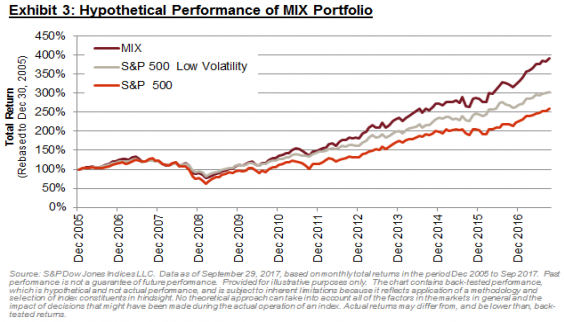

On a hypothetical basis, the MIX portfolio achieved roughly 100% upside capture (i.e. it did not lag in bull markets), while retaining a considerable degree of protection (77% downside capture). The MIX portfolio also demonstrated favourable performance statistics over longer periods. Over all possible rolling 12-month periods during our study, Low Volatility outperformed around 59% of the time; this increases to 72% for the MIX portfolio (Exhibit 5).

On a hypothetical basis, the MIX portfolio achieved roughly 100% upside capture (i.e. it did not lag in bull markets), while retaining a considerable degree of protection (77% downside capture). The MIX portfolio also demonstrated favourable performance statistics over longer periods. Over all possible rolling 12-month periods during our study, Low Volatility outperformed around 59% of the time; this increases to 72% for the MIX portfolio (Exhibit 5). The

The