No other recent presidential elections have been as divided as this year’s. As the objectivity and credibility regarding poll numbers and media coverage of the candidates are being questioned, the U.S. economy and the capital market are facing an unusual level of political risk. Market participants may seek various tools to hedge the downside risk, such as put options. The question is: to what degree a long put position can help to reduce overall portfolio volatility? To help answer this, we examine a hypothetical portfolio that already has a risk control mechanism in place.

Let’s consider a typical multi-asset portfolio invested in the S&P 500® and five-year U.S. Treasuries (UST) with a fixed volatility budget. When the realized volatility of the equity market exceeds the volatility budget, the portfolio is partially allocated to UST to keep the volatility under control; when the realized volatility of the equity market falls below the volatility budget, the portfolio is fully allocated to the S&P 500 to get 100% equity market participation. When the yield curve is inverted, all fixed income allocation will be shifted to cash. We can further assume that there is no shorting and no borrowing. The portfolio is rebalanced only when its realized volatility deviates more than 0.5% from the pre-specified volatility budget.

Overlaying this portfolio with a self-financed five-year synthetic put option on the portfolio struck at 80%, or in other words, assuming that we are able to pay x amount to buy a five-year put to protect 80% of the remaining portfolio (portfolio value minus x), we can observe the level of volatility reduction derived from this put overlay.

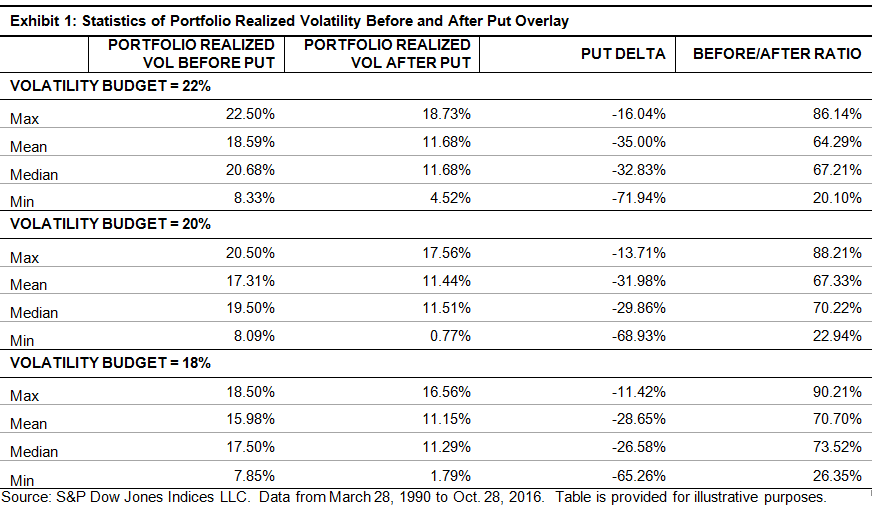

Exhibit 1 shows the statistics of the portfolio’s realized volatility before and after the put overlay. The delta of the synthetic put drives risk reduction. Higher volatility budge usually results in a more volatile portfolio and a higher delta of the put option, which, in turn, reduces more risk in ratio terms (1-Before/After Ratio).

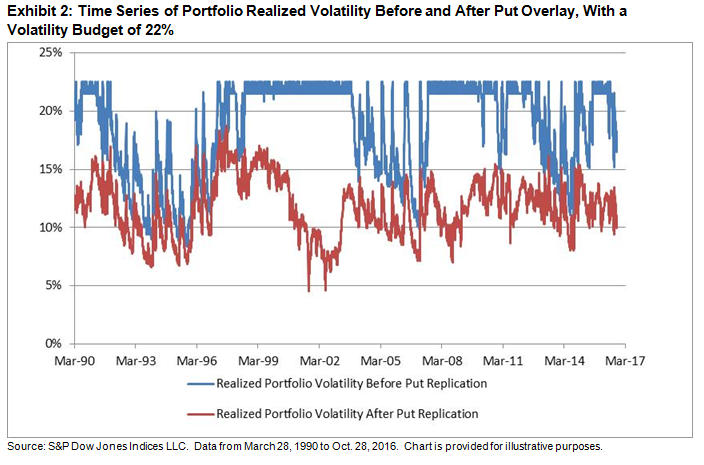

Exhibit 2 shows the time series of the realized volatilities before and after the put overlay for a portfolio with a volatility budget of 22%.

As a rule of thumb, overlaying a put option on a ~20% volatility portfolio reduces about 6%-8% of the realized volatility over a 26-year period. The good old put protection strategy has been working for decades, and it could still be a powerful volatility reduction tool no matter who becomes the next president.

Note: Realized volatility is defined as the maximum of the long-term volatility and short-term volatility in the S&P Risk Control Indices Model. This is because this is usually the volatility that is used to adjust the portfolio allocation to meet the volatility budget. For more information about the calculation, please refer to S&P Risk Control Indices.

The posts on this blog are opinions, not advice. Please read our Disclaimers.