Equity markets are notoriously volatile, at least when compared to fixed income. Dividend payments, by contrast, while not fixed like many bond coupons, offer market participants a much less volatile and more fixed income-like risk and return profile. For the 25 years from 1990 to 2015, the annual variation in S&P 500® dividend points has been 7.65%, compared to 17.4% for the S&P 500® itself. Similarly, since the inauguration of the S&P 500® Dividend future, the realized volatility of the December 2020 contract has been 6.5%, annualized, compared to 15.8% for the E-Mini S&P 500® Index future.

Dividends and GDP Correlation

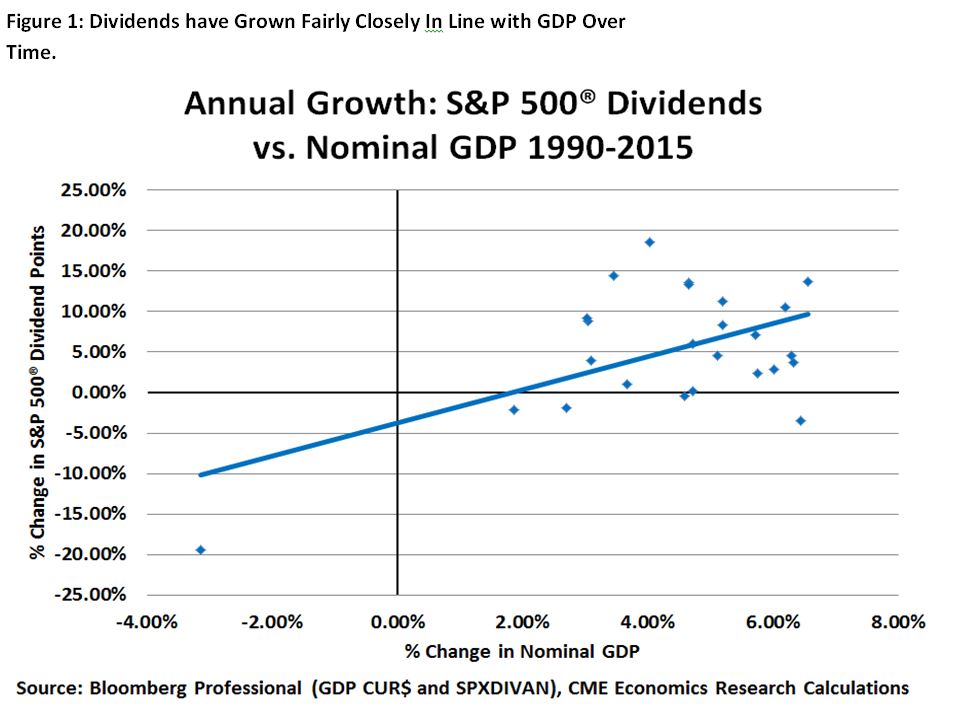

Although payout ratios and corporate earnings as a percentage of GDP change over time, S&P 500® dividend payments have correlated with changes in nominal GDP at around 50% since 1990 (Figure 1). This contrasts sharply with the S&P 500® itself, whose correlation with annual changes in GDP is only 0.1% over the same period. This is largely because equities anticipate future changes in GDP whereas dividends are more apt to reflect present conditions.

Bottom Line

- The main drivers of dividends are corporate profit growth and payout ratios.

- Corporate profits vary as a percentage of GDP, and payout ratios can be influenced by the economic cycle and tax policy.

- While corporate earnings are challenged by the low inflation and sluggish global growth environment, which may lead to more stock price volatility, dividends are far less volatile than equity indices, displaying slightly less than half of the annualized variation.