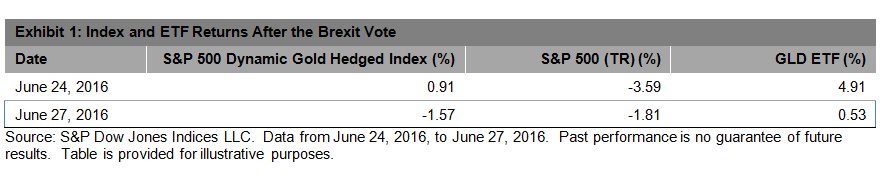

Gold often rallies in times of intense market turmoil, as the safe-haven asset is perceived as a hedge against economic and financial risk. This was one of the rationales for constructing the S&P 500 Dynamic Gold Hedged Index. What happened on Friday, June 24, 2016, clearly demonstrated the effectiveness of the strategy in terms of providing diversification when it is most needed. On that single day, the S&P 500 (TR) returned -3.59% (the 50th largest single-day drop in the past 30-year period), while the S&P 500 Dynamic Gold Hedged Index returned 0.91%. Would this happen again if Trump were elected president of the U.S. in November? That would be interesting to see.

In addition to the potential diversification benefit, the S&P 500 Dynamic Gold Hedged Index could possibly protect portfolio returns from the effects of currency devaluation. This is especially relevant with the current market conditions, as some market participants might conclude that central banks could respond to the Brexit vote by adding more monetary stimulus. In the immediate aftermath of Brexit, the Bank of England said it was well prepared and ready to provide an additional GBP 250 billion in liquidity.

Another thing to note is that the S&P 500 Dynamic Gold Hedged Index is designed to reflect the strategic overlay approach that may provide a more efficient way to gain exposure to gold. The approach pairs a core investment (the S&P 500) with a portfolio hedge applied through a derivative instrument (gold futures). With this approach, market participants do not need to cut their equity exposure in order to increase their holdings in gold. As a simple illustration, if a market participant sold 50% of their S&P 500 holdings and bought into GLD ETF, this 50/50 portfolio ETF would have generated a return of 0.66% Friday, June 24, 2016, 25 bps lower than that of the S&P 500 Dynamic Gold Hedged Index, and this does not include transaction costs.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

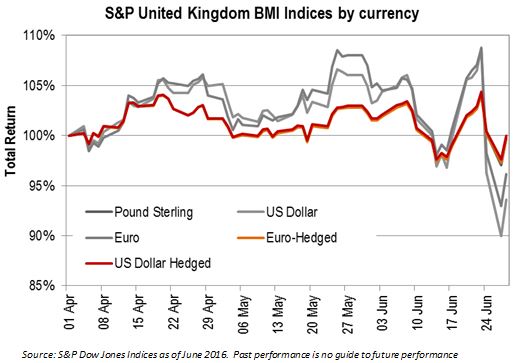

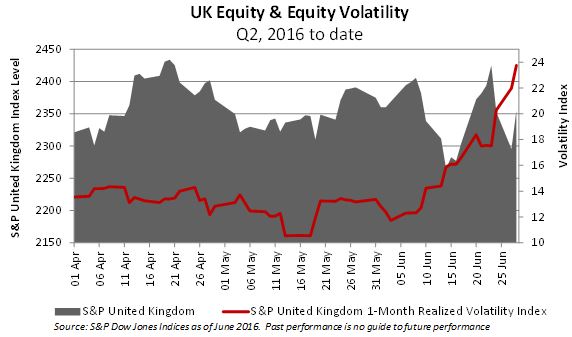

Given the general sentiment, it is notable that the UK’s equity market is not far at all from where it was only three months ago, at least, in pound sterling terms. One reason that the market has held up so well is due to the fall in the value of the British pound: for the large multinationals that make up a significant proportion of the local exchange, a cheaper pound inflates the relative value of their considerable foreign revenues. The chart above shows a very different picture for investors calculating their returns in a different home currency.

Given the general sentiment, it is notable that the UK’s equity market is not far at all from where it was only three months ago, at least, in pound sterling terms. One reason that the market has held up so well is due to the fall in the value of the British pound: for the large multinationals that make up a significant proportion of the local exchange, a cheaper pound inflates the relative value of their considerable foreign revenues. The chart above shows a very different picture for investors calculating their returns in a different home currency.