Despite some warnings from volatility gauges, the market had “priced in” a vote for remain from the UK’s population. This has made for some dramatic headlines, and large movements since the vote to leave the EU was announced. As the market scrambled to make sense of the political chaos, three key themes have emerged from the market’s reaction.

- Higher Volatility

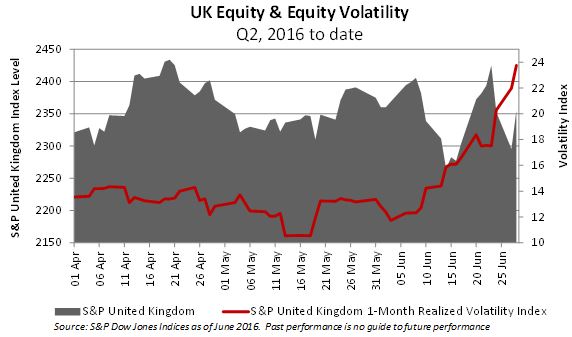

The past few days have seen a rapid repricing in European markets, causing volatility to increase. While volatility tends to rise precipitously, it tends to fall much more gradually. Moreover, the political crisis triggered in the UK by the Brexit vote, and the general record of the EU in solving difficult negotiations, provides grounds to suppose this time will prove no exception. Given the general sentiment, it is notable that the UK’s equity market is not far at all from where it was only three months ago, at least, in pound sterling terms. One reason that the market has held up so well is due to the fall in the value of the British pound: for the large multinationals that make up a significant proportion of the local exchange, a cheaper pound inflates the relative value of their considerable foreign revenues. The chart above shows a very different picture for investors calculating their returns in a different home currency.

Given the general sentiment, it is notable that the UK’s equity market is not far at all from where it was only three months ago, at least, in pound sterling terms. One reason that the market has held up so well is due to the fall in the value of the British pound: for the large multinationals that make up a significant proportion of the local exchange, a cheaper pound inflates the relative value of their considerable foreign revenues. The chart above shows a very different picture for investors calculating their returns in a different home currency.

- The Pound and the Euro are the battlegrounds

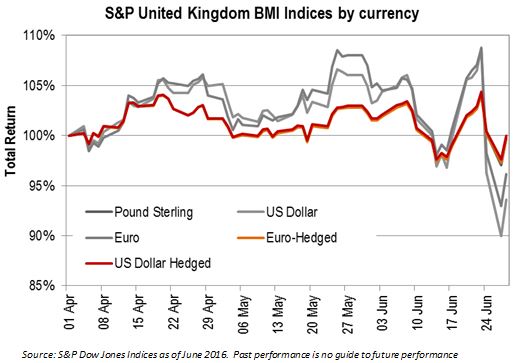

Much of the trading activity around the UK’s referendum and its putative consequence has focused on the pound sterling. This is both a European and UK crisis; both currencies have come under pressure. For international investors, the use of currency hedged equity indices can mitigate the volatility of investments that arise from such fluctuations. As the chart shows, European or U.S. investors in the UK markets could have more or less mimicked the returns of local investors during the period. However, those who did not hedge the currency faced material losses:

And in a broader environment where central banks globally continue to face the temptations of a race to debase, currency hedging offers a way to limit the impact of macro-economic policy missteps, too.

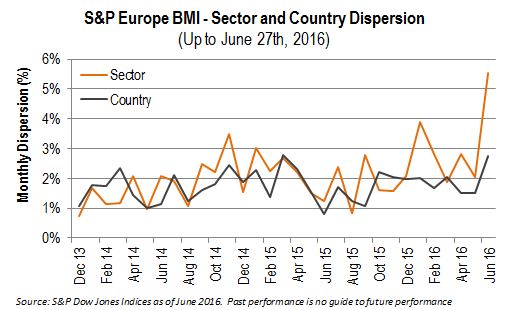

- Higher Dispersion among Sectors than Countries

Along with volatility, dispersion is also rising. However, at least for the moment, the changing economic outlook and opportunity set has driven a wider spread of dispersion among sectors than countries. Wherever they are based, European Financials face the potential for material disruption from a Brexit, while Energy companies and Consumer Staples have so far been largely untroubled. If this trend were to continue, then the opportunistic investor should calibrate their views to which sectors might benefit, rather than which countries.

Should I stay or should I go?

Of late, Europe’s political class has maintained a far-from spectacular record in the speedy resolution of crisis. Faced by a market whipped by political uncertainty and facing an interminable period of months and perhaps years before a definite outcome, investors may be tempted to avoid Europe and the UK altogether. Indeed, as the recent steep falls demonstrate, many already have.

Those who remain might well prepare for higher volatility, and might consider currency hedged versions of investments where appropriate. Finally, and despite the seeming importance of national distinctions to current events, so far it has mattered less whether stocks are based in the core, periphery or edge of Europe. Investors may be wise to keep a closer eye on sectors, than countries.

The posts on this blog are opinions, not advice. Please read our Disclaimers.