Amidst continuing anxiety over financial markets, the U.S. economy turned in some good numbers last week. Fourth quarter GDP was revised upward to 1% real growth from 0.7% with consumer spending up 2.0% at seasonally adjusted real annual rates. Surveys of forecasters had expected growth to be scaled down to 0.4%. Final sales — GDP excluding inventories – was up at a 1.2% real annual rate. Residential investment was the stand-out performer, rising at an 8% real annual rate. Personal income and consumption in January — both up at a 0.5% month pace before adjusting for inflation — beat forecasters’ expectations. Orders for durable goods rebounded strongly from a weak December with strong 5% month on month growth as the non-defense capital goods component was up 3.9% on the month.

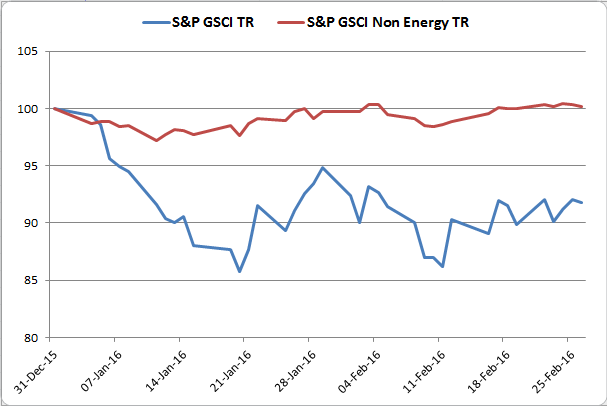

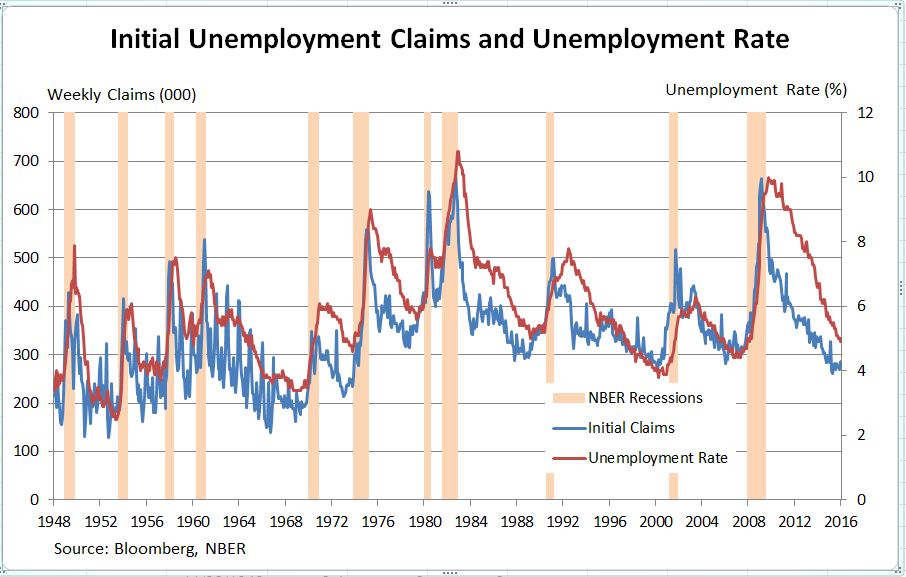

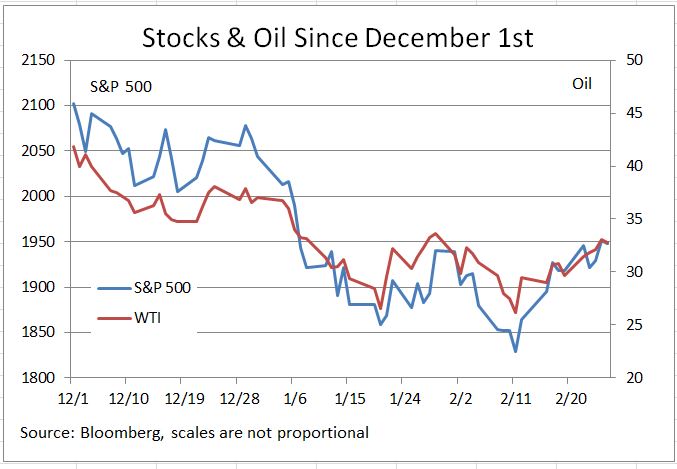

Attention will turn to what’s next – the employment report scheduled for March 4th. One consistent aspect of this economic expansion has been the low number of weekly initial unemployment claims. They continue to run well below 300,000 — the level usually seen as the border between solid growth and possible slowness. Initial claims – the number of people newly out of work filing for unemployment insurance are often cited as a predictor of the unemployment rate. The first chart shows this pattern. Early published forecasts* look for payrolls to rise by about 200,000; much better than the disappointing 151,000 in January but not quite at the recent average of 230,000 per month. Forecasts suggest the unemployment rate will remain at 4.9%. Anxiety about the markets will remain, even though both the S&P 500 and oil have so far held above their recent low set on February 11th.

*forecast by Marketwatch

The posts on this blog are opinions, not advice. Please read our Disclaimers.