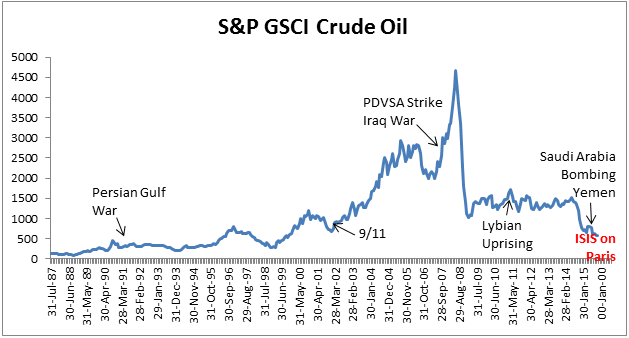

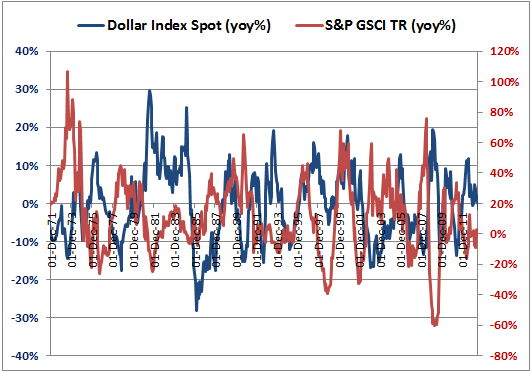

It makes sense that a strong US dollar is generally bad for commodities since as the U.S dollar strengthens, goods priced in dollars become more expensive for other currencies. However, historically the U.S. dollar has a negative correlation of only about -0.30 with the S&P GSCI as shown in the chart below using data since 1970:

This may be surprising since -0.30 correlation does not show a very strong negative relationship. It may be explained partially by the late additions of (WTI) crude oil that did not occur until 1987 and brent crude in 1999. Their combined weights have been up to roughly 50% of the S&P GSCI at times, so their impact on the overall composite relationship to the dollar is significant. In the past 10 years, crude oil and brent crude are two of the most sensitive and negatively correlated commodities in the index to the dollar. Brent crude and (WTI) crude oil are negatively correlated -0.67 and -0.66 with beta of -2.9 and -2.8, respectively. This has driven the S&P GSCI to have a negative correlation of -0.63 to the U.S. dollar. Simply put, brent and WTI have doubled the negative correlation of the index to the U.S. dollar.

However, there are other commodities that just aren’t so badly impacted. Feeder cattle and sugar have up market capture ratios of 130 and 125, using the dollar as the market, that says those commodities outperformed the dollar by 30% and 25%, respectively, in the past 10 years. Further, gold, live cattle, zinc, lean hogs and coffee have all posted positive returns on average when the dollar was up.

While the strong U.S. dollar is bad for commodities overall, it hurts far less than how much a weak dollar helps commodities. In the past 10 years on average, the U.S. dollar was pretty symmetrical with 58 periods of a rising dollar and 62 periods of a falling dollar, and in terms of the magnitude of gains and losses on average of -6.14% and +6.18%. When the dollar was up, brent crude lost 3.67% and (WTI) crude oil lost 4.00% with the worst average loss in nickel of -12.02%, far more than the single commodity average loss of -1.97%. However, when the dollar lost, not one single commodity fell on average and the single commodity gained 24.64% on average. Below is the table that shows the performance:

The posts on this blog are opinions, not advice. Please read our Disclaimers.