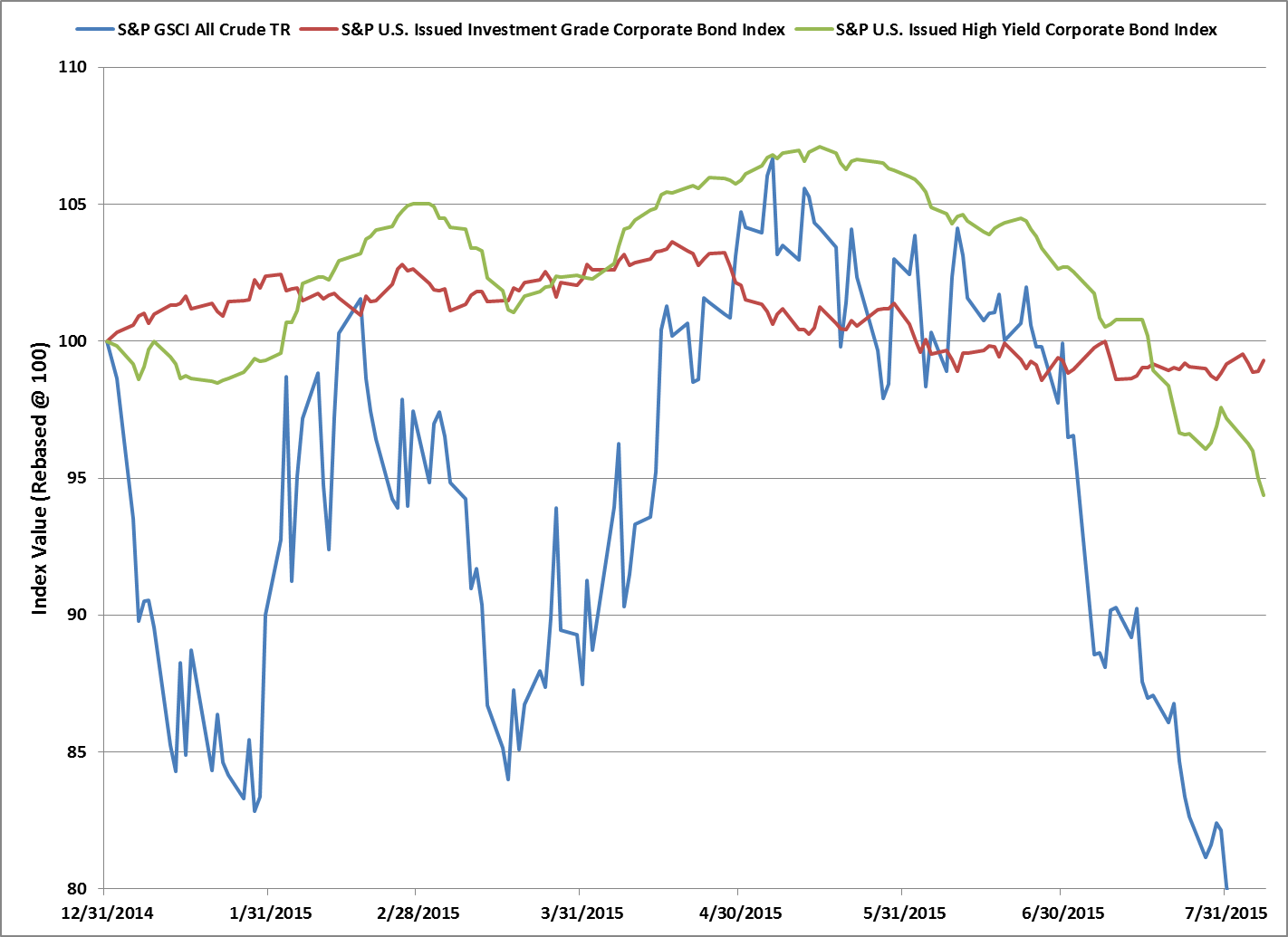

Crude oil, as measured by the S&P GSCI All Crude was down 20% in July 2015 and has continued its sell-off in August 2015 by dropping another 6.86%. As of Aug. 10, 2015, the index has returned -25.4% YTD. Energy-related bonds in the investment-grade or high-yield indices have added a negative hit to the indices’ overall performance.

The energy sector of the S&P U.S. Issued Investment Grade Corporate Bond Index accounts for 8.6% of the index’s market value. So far in August 2015, the sector has remained positive, returning 0.14%, almost offsetting July 2015’s -0.15% return. June 2015 had a more significant negative performance with -2.05%. The S&P U.S. Issued Investment Grade Corporate Bond Index has returned 0.16% MTD and -0.03% YTD. The S&P 500® Energy Corporate Bond Index, a sub-index of the S&P 500 Bond Index that includes both investment-grade and high-yield issuers of the equity index, has returned -0.11% MTD and -0.72% YTD.

In the S&P U.S. Issued High Yield Corporate Bond Index, the energy sector has had more of an impact, as the market value weight of the sector is 14.4% of the index. Already in August 2015, the energy sector is down 2.9%, following a 5.37% loss in July 2015 and a 3.31% loss in June 2015. At the end of May 2015, the S&P U.S. Issued High Yield Corporate Bond Index had a YTD return as high as 4.08%, but it has returned 1.18% YTD.

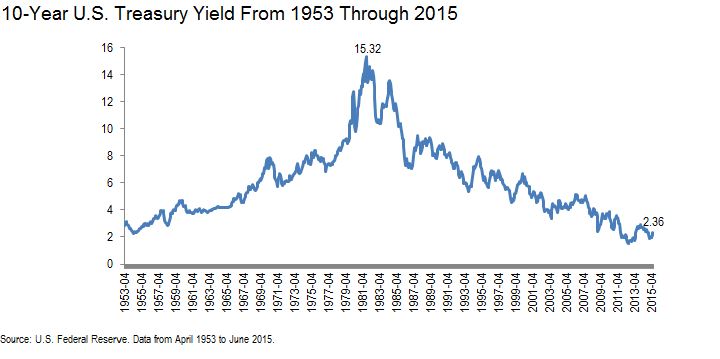

Treasury yields, as measured by the S&P/BGCantor Current 10 Year U.S. Treasury Bond Index, moved 17 bps lower in July 2015. The first week of August 2015 saw the yield-to-worst of the S&P/BGCantor Current 10 Year U.S. Treasury Bond Index close almost flat, after moving 12 bps higher on the release of stronger Factory Orders and ADP Employment numbers. However, the increase in rates did not last long, as the yield-to-worst moved down 10 bps to close at 2.17%. The index has returned 0.18% MTD and 1.57% YTD. Market participants will return from their vacations in August 2015 to focus on September 2015 and the possibility of a Fed rate hike.

Exhibit 1: Index Values

Source: S&P Dow Jones Indices LLC. Data as of Aug. 7, 2015. Past performance is no guarantee of future results. Chart is provided for illustrative purposes.

The posts on this blog are opinions, not advice. Please read our Disclaimers.