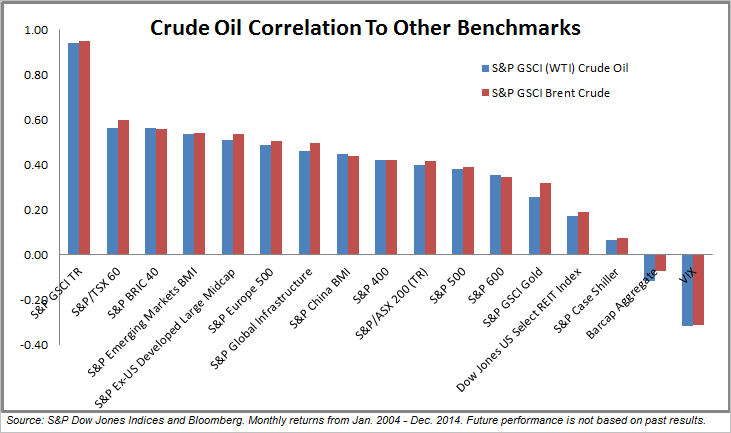

While many assets have some relationship with oil, there are varying degrees of correlation and even a few surprises. For example, Canadian equities are more correlated with oil than are the emerging markets and the US equities; Australian equities are barely correlated with oil, and China who is not nearly as big a producer as a consumer is moderately correlated with oil.

Gold and (Brent) oil are not as oppositely related as many think but have a weak-moderately positive correlation of 0.32. (Correlation of +1.0 is perfectly positive, indicating assets move in lockstep, correlation of 0 indicates no relationship, and correlation of -1.0 is perfectly negative, indicating opposite movement. Generally the more negatively correlated the assets, the more diversification.) While gold straddles the line between a low and moderately positively correlated relationship, a few other asset show more diversification historically.

Real estate and bonds show little relationship with oil with correlations of 0.18 (REITs), 0.07 (S&P Case Shiller) but VIX is the one asset with even moderately negative correlation with oil of -0.32.

The posts on this blog are opinions, not advice. Please read our Disclaimers.