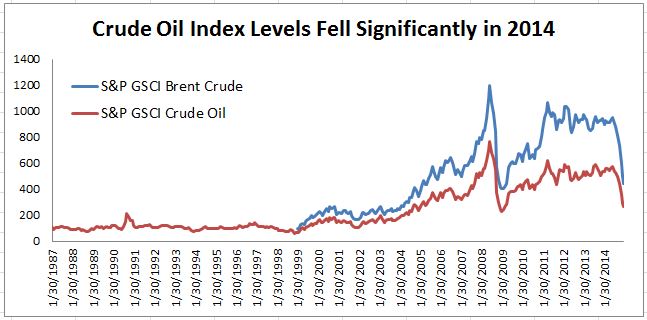

The current quote of NYMEX crude is lower by $2 today as the price action of crude oil has been on a downhill slide since the end of June 2014. The news is loaded with stories of oil and its effects on consumers and the economy. Min Zeng of the Wall Street Journal published “Closely Watched Inflation Gauge Falls to Lowest Level in 14 Years,” while his colleague Jason Zweig approached the issue from a differing angle. In his article, “Here’s a Tip: Buy More TIPS,” Mr. Zweig makes a case for investors to keep an eye on the performance of TIPS (Treasury Inflation-Protected Securities) and to be opportunistic with investing. The article states, “in recent months, as oil has fallen, TIPS ‘have taken a huge adjustment,’ says Gemma Wright-Casparius, portfolio manager of the Vanguard Inflation-Protected Securities Fund, with $24.8 billion in assets. ‘They look fairly priced to me now.’” This asset class may be down, but don’t count it out, if I was to paraphrase the message.

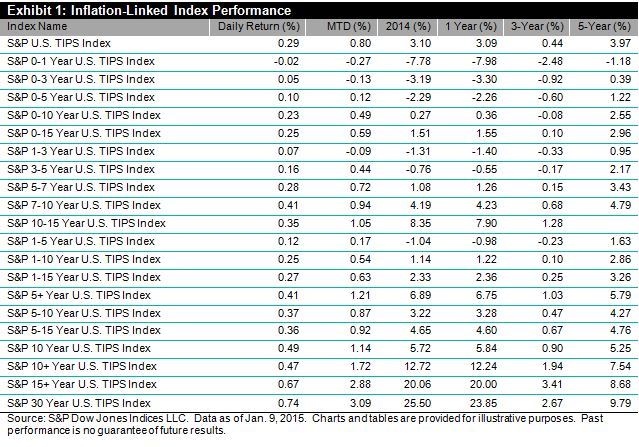

The return of the S&P U.S. TIPS Index for 2014 was 3.10%, though the index did have a tough December, returning -1.1%, and an even tougher September, losing 2.38%. As of Jan. 9, 2015, the index was returning 0.80% MTD.

The U.S. Fed seems determined to get inflation up to its target level of 2%, though the current, all-items CPI of 1.3% YOY is nowhere near the target. Extreme as it may seem, the Fed does have the tools to print money in order to push the inflation level upward. Current expectations are that inflation will stay low, but as we know, the idea of insurance is to protect against the unexpected. As the saying goes, “the best time to buy insurance is when the sun is shining.”

Source: S&P Dow Jones Indices. Data from Jan 30, 1987 to Jan 8, 2015. Past performance is not an indication of future results.

Source: S&P Dow Jones Indices. Data from Jan 30, 1987 to Jan 8, 2015. Past performance is not an indication of future results.