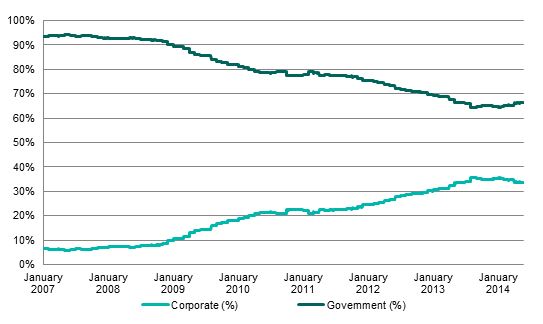

The size of the local-currency-denominated corporate bond market in China, as measured by the S&P China Corporate Bond Index, currently stands at CNY 7.58 trillion, representing an expansion by more than 14 times since December 2009. The strong issuance was driven by the country’s robust economic growth and tighter liquidity conditions. The corporate bond sector has also gained an increasing market share of the overall Chinese bond market; it rose from less than 10% to 33% over the period studied, see the exhibit below.

Exhibit: Corporate vs. Government Bond Markets in China

As of June 18, 2014, the S&P China Corporate Bond Index has risen 5.81% YTD and 33.4% since the index’s first value date on Dec. 29, 2006. Besides the potential currency appreciation, the boom in Chinese debts comes amid an increasing appetite for fixed income assets in addition to the potential yield pick-up offered in the current low-rate environment. Currently, the modified duration of the S&P China Corporate Bond Index is 3.45, with a weighted yield-to-maturity of 5.38%.

Within the corporate bond market, the S&P China Industrials Bond Index is the largest and the fastest growing sector, which represents over 48% of the market. It is followed by the S&P China Financials Bond Index with around 36% of the share.

In fact, over 90% of Chinese corporate bonds are issued by state-owned enterprises (SOE).[1] The SOEs are generally expected by the market to have a low default risk due to their implicit government guarantee and relatively easy access to other funding channels. On the other hand, the non-SOEs that are in industries that face overcapacity issues are perceived to be at higher risk.

As China continues to implement new policies to strengthen the economy, the growth in the corporate bond market is anticipated to remain solid.

Please visit HERE to continue reading.

[1] Bank of America Merrill Lynch, More on China’s on-shore corporate bond market, Asia Credit Strategy, March 28, 2014

The posts on this blog are opinions, not advice. Please read our Disclaimers.