The coming week will provide Europeans with a chance to vote in the 2014 EU parliament elections. Nationally and internationally, the contest is viewed as somewhat moot; the majority across the EU will most likely not even vote.

But whilst voters in the EU elections are not voting for members of the ECB or its president Mario Draghi, the European central bank IS directly governed by the laws of the EU parliament. With laws defining a financial transaction tax, bank regulation and a potential banking union all on the immediate agenda for the EU, the outcome may be more important than the minimal degree a low turnout and sparse media coverage implies.

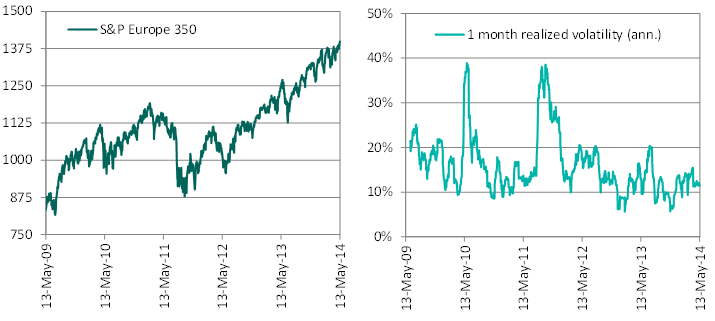

At the time of the last elections (held between 4 and 7 June 2009), the EU exhorted citizens to vote with campaigns with titles such as “How much should we tame financial markets?”. Since then, in price terms, the S&P Europe 350 index of large-cap stocks is up by over two thirds. And, whilst the markets were not “tamed” entirely, volatility has certainly come down:

S&P Europe 350 price return and volatility, May 2009 – May 2014

Source: S&P Dow Jones Indices, May 2014. Charts are provided for illustrative purposes only. Past performance is no guarantee of future results.

Most equity investors would not be disappointed with such returns – including the effects of dividends before tax, the gross total return of the S&P Europe 350 was 100% – but investing is a relative game. If you had decamped to the U.S. markets and the S&P 500 in particular, as many did during the Eurozone crisis, you would have done better.

Source: S&P Dow Jones Indices, May 2014. Tables are provided for illustrative purposes only. Past performance is no guarantee of future results.

More recently, Europe-focused ETFs listed in the U.S. saw large inflows and flows from U.S. investors to European stocks have been tilted in favour of the latter since the new year. Why are those outside Europe now buying in?

Value is part of the answer: after five years of stellar performance, valuations in the U.S. have risen too; and by a greater extent than their underperforming European equivalents. So by now on most measures of “value” Europe certainly looks “cheaper” than the U.S.

But it is not just U.S. value investors who are attracted. The considerable fillip to the U.S. markets provided by tens of billions of monthly bond purchases by the Fed’s stimulus program looks likely to be wound down by the coming October; interest rates are predicted to rise shortly thereafter. The ECB has so far only provided oral guarantees supporting the Euro (“whatever it takes”). And while the ECB does not look set to make a surprise announcement of anything like the U.S. program; the prospect of deflation has brought on more bullish talk. The ECB has also relied less on signalling their intentions than the Fed, a consequence of which is greater uncertainty.

Judging by the experience of Japan and the U.S., expanded fiscal stimulus in Europe will likely boost the equity markets in its wake. Those investors who won’t “fight the Fed” – and those flocked to Japan early last year – will be watching Europe closely. It is impossible for us to predict who will do better out of Europe or the U.S. over the next five years. But we can certainly understand why U.S. investors are looking to Europe at present.

Ultimately, the role and composition of pan-EU institutions impacts the demand from international investors for equity markets in the region.The winners of the 2009 elections, still reeling from a financial crisis, were shortly served a potent cocktail of challenges to the integrity, currency, credit and economic future of the region via the Eurozone crisis. The challenges ahead will hopefully not prove equally testing, but for their impacts on the financial markets alone, these elections may well prove important.

The posts on this blog are opinions, not advice. Please read our Disclaimers.