In the weekend Wall Street Journal (May 3, 2014) there is an informative article entitled “The Risks of Floating Rate Funds”. The article does a great job of delving into the risks of these types of structures and is quite timely as the low rate environment continues. The investor appetite for floating rate assets while facing the prospect of future rising interest rates is a fascinating topic. The goal of this blog is to add some information in to the discussion.

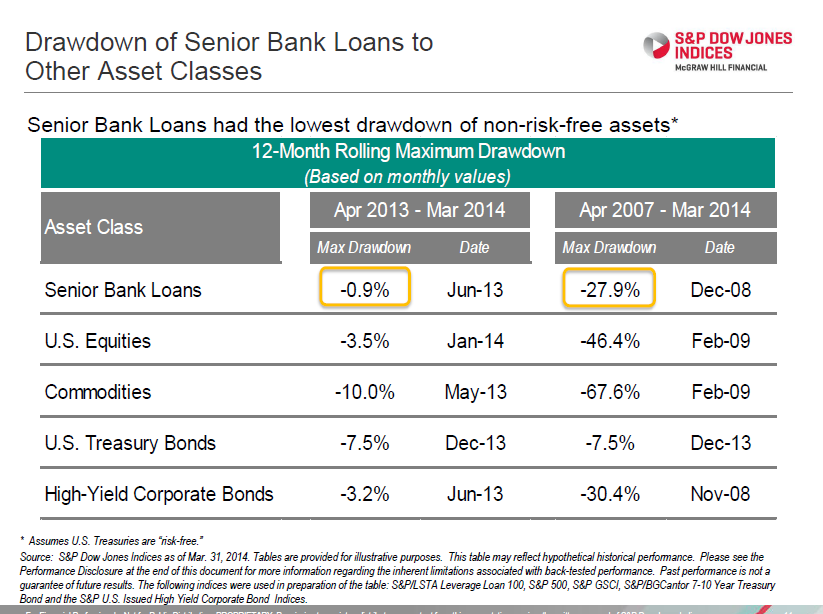

The volatility of the senior loan asset class is an important topic. There certainly was a volatile time period during 2008 and 2009 for the financial markets. The S&P/LSTA U.S. Leveraged Loan 100 Index tracking the senior loan market saw a dramatic decline in value in 2008 of just under 28%. It may be valuable to also consider the environment and compare that drop in value to other asset classes during that time period: the S&P 500 Index was down over 46%, the S&P GSCI was down over 67% and high yield corporate bonds were down over 30%. During the twelve month period of ending April 2014 the senior loan market experienced a maximum decline of 0.9% while the other markets have experienced larger negative swings.

Source: S&P Dow Jones LLC. Data as of March 31, 2014.

Echoing an important point raised in the Wall Street Journal article is the aspect of interest rate ‘floors’. During this low rate environment the interest rate paid out by many senior loans has been held to minimums or ‘floors’. The interest rate of these floating rate loans are tied to benchmark rates, typically LIBOR, that have dropped significantly. As of year end 2013, approximately 80% of the loans in the S&P/LSTA U.S. Leveraged Loan 100 Index have some type of interest rate floor. For the interest rate on those loans to rise the benchmark rate, LIBOR, needs to rise to a point where the rate (LIBOR plus spread) breaks through that minimum rate or the ‘floor’ of these loans. The key aspect of this is when the rate does rise enough to be above the interest rate ‘floor’ the lenders get the benefit of a rising rate. Meanwhile, the loans with floors are earning above market yields due to the ‘floor’.

There are many other aspects of risk and reward related to the senior loan and high yield corporate bond markets that can be discussed in additional posts.

The posts on this blog are opinions, not advice. Please read our Disclaimers.