A laddered preferred portfolio uses the same concept as bond laddering, where a portfolio is constructed with instruments of staggering maturities so that a fixed portion of the portfolio matures each year. Rate-reset preferreds are used in a portfolio laddering strategy since they incorporate a reset date every five years. On the reset date, which can also be thought of as a maturity date, either the dividend is adjusted based on a spread above the current five-year government bond yield or the security is called for redemption.

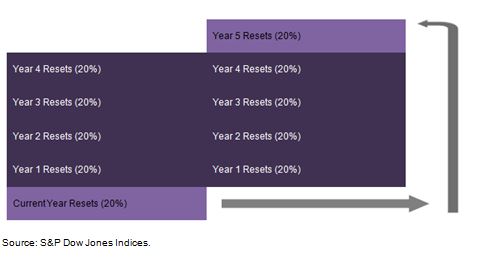

The S&P/TSX Preferred Share Laddered Index is an example of a laddered preferred strategy. The portfolio is broken out into five term buckets based on the reset date calendar year, with each bucket given an equal weighting at rebalancing. This implies that a portion of the portfolio resets each year based on the current interest rate levels. At the beginning of each year, the buckets are changed so that the previously current year term bucket becomes the last term bucket, the year 1 term bucket becomes the current year term bucket, year 2 becomes year 1, and so on.

Benefits and Risks of a Laddered Preferred Portfolio

The potential benefits of a laddered preferred portfolio largely relate to addressing interest rate risk. Perpetual preferreds have high sensitivity to interest rate changes since they have a fixed dividend payment and no set maturity date. Rate-reset preferreds typically exhibit less interest rate risk as the maximum time to the next reset date, or maturity, is five years. In fact, when looking at duration, it is estimated that rate-reset preferreds have durations between 2 and 3 years whereas perpetual preferreds have durations between 11 and 15 years[1]. In a portfolio context, the laddering strategy helps dampen negative effects of interest rate changes, while still offering the opportunity to participate in increased yields. If interest rates are low in a given year, only a portion of the portfolio will be reset to the lower yields. Conversely, the portfolio can benefit from increased interest rates, as part of the portfolio would reset to higher yields.

Two risks related to rate-reset preferreds involve call risk and changes in the regulatory landscape. Call risk may increase in low interest rate environments; when interest rates are low, credit spreads generally decrease between risk-free assets such as government bonds and risky assets such as preferreds. A company may be able to reduce interest expense by calling an outstanding preferred share class and issuing a new share class at a lower spread above the benchmark yield. Changes to the regulatory landscape also pose a threat to rate-reset preferreds. Under Basel III regulations, most preferreds including rate-resets will no longer be considered part of Tier 1 Capital from 2013 onward. This particularly affects financial institutions, as they are required to hold a certain percentage of total capital in Tier 1 assets. To comply with the new regulations, financial institutions may shift from issuing preferreds to other assets still considered to be Tier 1 Capital.

For more on preferreds in Canada, read our recent paper, “Looking Under the Hood of Canadian Preferred Indices.”

[1] Source: National Bank Financial Product Review: BMO Laddered Preferred Share, Jan. 16, 2013.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

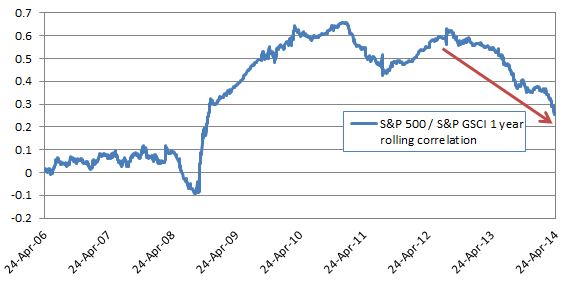

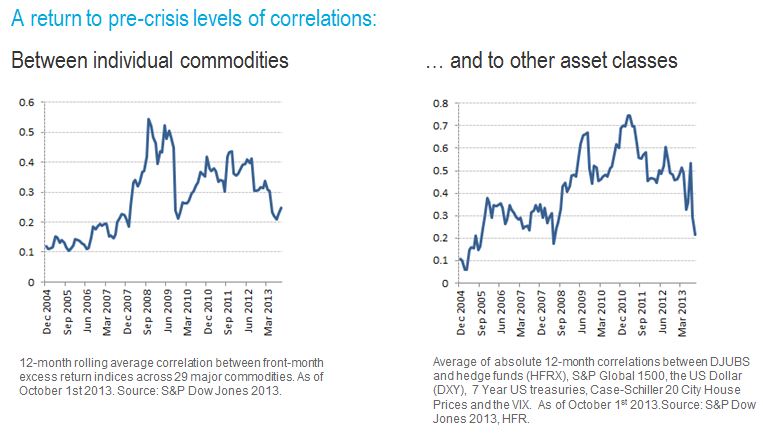

Notice in the charts above that both correlation of commodities to each other and to other asset classes has fallen to precrisis levels of about 0.2, indicating little movement together with stocks and bonds and little movement together with each other. This makes commodities, once again, an asset class to provide diversification, and

Notice in the charts above that both correlation of commodities to each other and to other asset classes has fallen to precrisis levels of about 0.2, indicating little movement together with stocks and bonds and little movement together with each other. This makes commodities, once again, an asset class to provide diversification, and