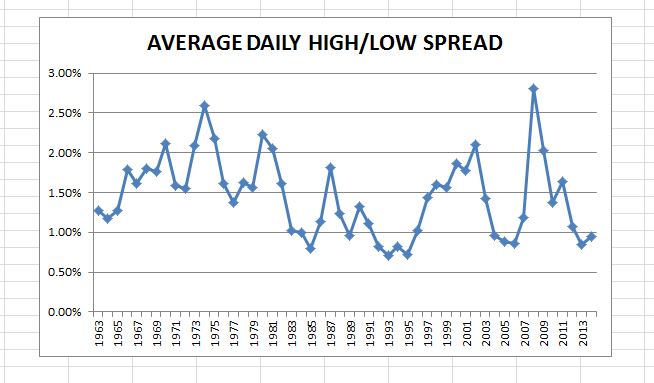

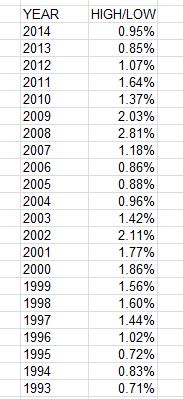

The market was up 0.7% this morning, and down 0.7% in early afternoon trading, and is currently trending up from the red. So I keep hearing that volatility has returned to the market. Maybe, if you just started trading. Daily volatility, as measured by the daily high price divided by the low price, has increased to an average 0.95% from last year’s 0.85%. However, the prior year, 2012, was 1.07%, with the year before that, 2010 being 1.64%, and the 50-year average is 1.47% – 50% more than the current year. Compared to that data today’s market is tame (the VIX, while up today, is still under 15). The increased perception is due to last year’s low volatility, which was the lowest since 1995. If you truly want to see volatility look at 2008-2009, when it averaged over 2.4% a day, and we saw (many) days where the index was up 1% at 3 p.m. and closed down 1%.  Additionally, last year saw significant gains in the market, as 2013 posted a 29.6% gain, with 457 of the S&P 500 issues gaining, as compared to the 2014 year-to-date, which is up 0.81%, with 275 issues up. Also differentiating this year is the number of issues moving well outside the index return of up 0.81% YTD. To date, 103 issues are up at least 10% this year, with 51 declining at least 10%. While the index has been flat, it would appear the battle from within has been ranging, and that has added to the perception of volatility.

Additionally, last year saw significant gains in the market, as 2013 posted a 29.6% gain, with 457 of the S&P 500 issues gaining, as compared to the 2014 year-to-date, which is up 0.81%, with 275 issues up. Also differentiating this year is the number of issues moving well outside the index return of up 0.81% YTD. To date, 103 issues are up at least 10% this year, with 51 declining at least 10%. While the index has been flat, it would appear the battle from within has been ranging, and that has added to the perception of volatility.

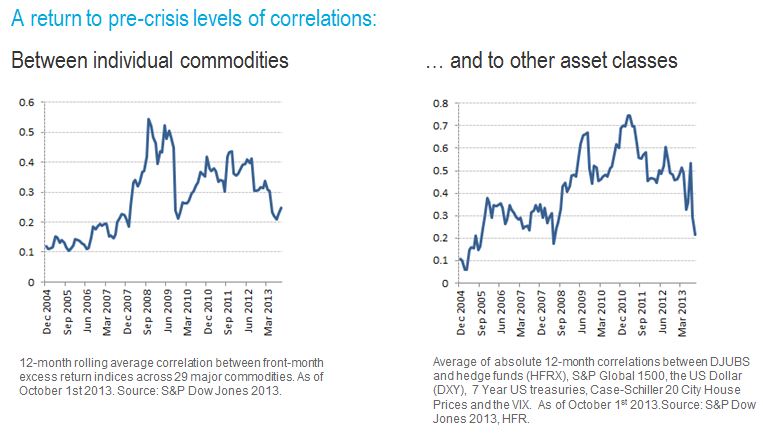

Notice in the charts above that both correlation of commodities to each other and to other asset classes has fallen to precrisis levels of about 0.2, indicating little movement together with stocks and bonds and little movement together with each other. This makes commodities, once again, an asset class to provide diversification, and

Notice in the charts above that both correlation of commodities to each other and to other asset classes has fallen to precrisis levels of about 0.2, indicating little movement together with stocks and bonds and little movement together with each other. This makes commodities, once again, an asset class to provide diversification, and