Puerto Rico Bonds Removed from Investable Municipal Bond Indices

On January 8, 2014, S&P Dow Jones Indices announced that it is removing bonds issued by Puerto Rico and other territories from the S&P National AMT-Free Municipal Bond Index effective January 31, 2014.

- Why? Puerto Rico bonds no longer meet the objective of the index.

The objective of the S&P National AMT-Free Municipal Bond Index is to be an investable index that measures the performance of the investment-grade tax-exempt U.S. municipal bond market. The Index excludes those sectors of the municipal bond market that have historically represented higher risks when compared to investment grade General Obligation and essential purpose bonds. For example, excluded are corporate backed municipal bonds, multifamily housing and health care bonds. Puerto Rico municipal bonds are now trading at levels more appropriate for high yield taxable corporate bonds. Puerto Rico municipal bonds also are experiencing varying degrees of liquidity in the secondary market. As a result, Puerto Rico municipal bonds no longer meet the objective established by this investable investment grade index.

- Puerto Rico bonds will remain in the broader benchmark indices designed for performance measurement and attribution analysis including the S&P Municipal Bond Index, the S&P Taxable Municipal Bond Index and their sub-indices.

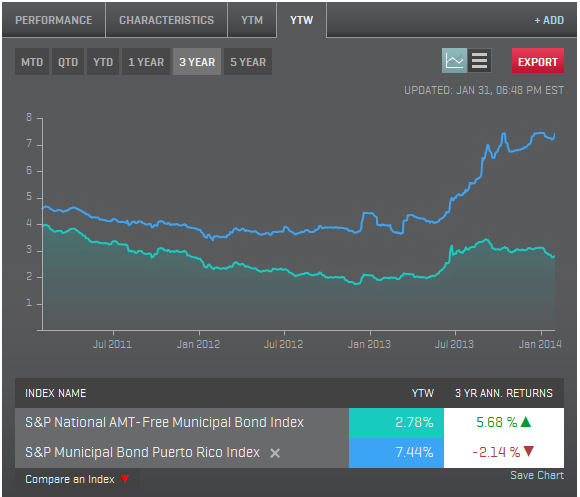

Market data as of January 31, 2014:

Puerto Rico remains a top story in the municipal bond market as it prepares to come to market with more debt. Bonds issued by Puerto Rico are rated at the lowest investment grade rating by Moody’s, S&P and Fitch. Each ratings service has recently announced the possibility of downgrade to below investment grade.

Since the start of 2014, the average yield of bonds in the S&P Municipal Bond Puerto Rico Index have ended unchanged at 7.44%. The yield got as low as a 7.19% on Friday the 24th but has risen by 25bps since then bringing bond prices back down. Throughout the ups and downs, the index has seen a year to date total return of 1.33% helping to offset its 2013 negative return of -20.46%.

Investment grade bonds tracked in the S&P National AMT-Free Municipal Bond Index have seen yield drop by 33bps this year to end at 2.78%. The drop in yields pushes bond prices up resulting in a positive 2.12% total return year to date.

High Yield municipal bonds tracked in the S&P Municipal Bond High Yield index have seen a positive 2.89% return year to date with yields of bonds in this index dropping by 30bps during January to end at 6.46%.

Link to the original announcement http://us.spindices.com/documents/index-news-and-announcements/20140108-muni-national-series-methodology-update.pdf?force_download=true

The posts on this blog are opinions, not advice. Please read our Disclaimers.