Alternative investments for high net worth investors are like the weather — everyone talks about it, but no one does anything about it. In fairness, alternative investments — hedge funds, private equity, and the like — are often hard to access and complicated to explain. But if they can deliver on their promise of uncorrelated returns — i.e., can serve as an effective hedge to an investor’s equity portfolio — then the game may well be worth the candle.

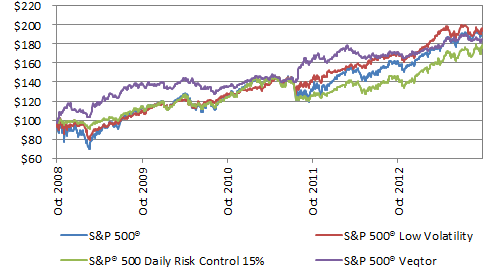

Not all alternative strategies are complicated or inaccessible. The S&P Dynamic VEQTOR Index, e.g., exploits the well-known inverse correlation between the equity market and volatility. When volatility spikes, in other words, the equity market typically plunges, whereas when volatility is declining, equities typically do well. So an index which is long both volatility and equities has the potential to deliver a relatively smooth pattern of returns compared to either asset class in isolation. That, it a nutshell, is what VEQTOR aims to do.

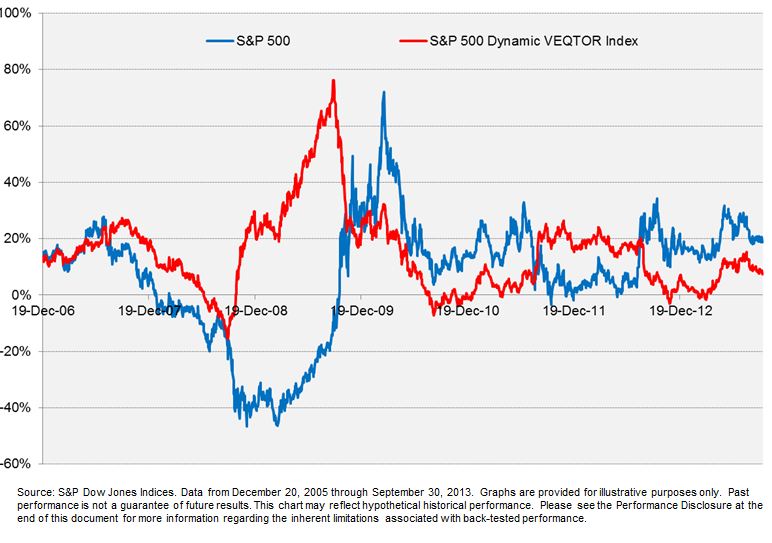

And successfully so, as the graph below demonstrates. We’ve graphed trailing 252-day (i.e. approximately one year) returns for both the S&P 500 and the S&P Dynamic VEQTOR Index. When the equity market was at its worst (e.g. during the 2008 financial crisis), VEQTOR did extremely well, since that’s exactly when its long volatility position was paying off. During more normal equity environments, VEQTOR tends to lag.

One of the remarkable things about VEQTOR is that it’s relatively uncommon for it to show a loss on a trailing 252-day basis. (Notice how the red line in the graph is typically above zero.) We can measure this effect by asking how often VEQTOR lost money:

The chart tells us that, of all the 252-day lookback periods in our data, the S&P 500 lost more than 20% 12.7% of the time. VEQTOR never lost that much. The other rows have an analogous interpretation. Most notably, VEQTOR lost money only 11.2% of the time — substantially less than the S&P 500.

This pattern of returns — limited downside with negative correlation to the equity market — is exactly the pattern of returns that makes alternatives appealing . VEQTOR demonstrates that such patterns can be both attractive and accessible.

The posts on this blog are opinions, not advice. Please read our Disclaimers.