In major cities at this time of year, an army of street vendors bristling with umbrellas await their chance to emerge in entrepreneurial fervour, providing tourists and commuters alike with immediate respite from unanticipated rain. It’s a viable business strategy: the chaotic nature of weather means that occasional rainfall remains practically impossible to predict*, hence our common tendency to rely on an adaptive strategy. Demand and cost rises with tempestuous environments, while the inconvenience of preparing for the worst is a frustrating drag in sunnier times.

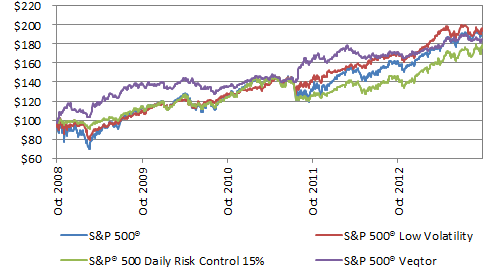

So does the same strategy of purchasing protection “as needed” work in the stock market? And does it cost more to do so? Stretching the analogy somewhat, we’ll look at three simple strategies to mitigate equity risk, and explain a little more behind the three indices shown below, each of which incorporates a different way to hedge an investment in the S&P 500® Index dynamically:

Source: S&P Dow Jones Indices. Total returns shown for the five year period to October 18th, 2013. Charts and graphs are provided for illustrative purposes. Past performance is no guarantee of future results.

1) Move to sunnier climates: permanently avoid more risky stocks

The “low volatility effect,” sometimes called the low volatility “anomaly,” refers to the tendency – manifest across a wide range of markets – for stocks with low volatility to outperform their peers, especially in terms of risk-adjusted returns. While academics continue debate the underlying dynamics – a behavioural explanation supposes that speculatively minded investors will gladly overpay for a potentially oversized return** – investors can capture this effect through indices that underweight or remove stocks with higher volatility. The S&P 500 Low Volatility Index removes 80% of the most volatile stocks from the index and weights to the remainder inversely proportional to their historical volatility.

2) Go back inside when it’s wet: exploit regimes in volatility

Volatility tends to persist: the level of the volatility today can be a guide to volatility tomorrow. If markets are currently choppy, it therefore may make sense to de-risk going forward. Systematic “risk control” indices realize this approach by explicitly targeting a prespecified risk level, dynamically allocating between equity and cash (in more volatile periods) in order to maintain the target. As well as potentially providing better performance, indices with such controls have gained widespread traction because of the reduced costs of protection – significantly cheaper put options in particular.

3) If everyone else is preparing for a storm, maybe you should too

The so-called “fear index”, VIX, reflects market expectations of future volatility. Surprisingly (perhaps), a high level of actual volatility shows a mild historical bias towards a subsequent positive return for VIX futures. Additionally, the VIX has also historically shown trending behaviour (if people are getting more worried, maybe you should too). Taken together, this suggests that a high and increasing VIX is a potentially useful signal.

Strategies that aim to capture trends or regimes typically show performance somewhat idiosyncratic to the specifics of their individual signal construction, but with nearly four years of live history the S&P VEQTOR Index provides a concrete example of the latter concept, using levels and trends in volatility to allocate between the 500® and short-term VIX futures.

Over the past five years, each of the three risk management strategies above resulted in an improved risk/return profile in comparison to the S&P 500®. And while we are duly assured that history is no guide to future performance, such results certainly support the view that dynamic risk management may be sensibly obtained without the costs of appointing an external active manager. Not dragging your golfing umbrella round in the sunshine, on the other hand, is likely to remain beyond the aegis of science. At least the street vendors will be glad of that.

* Even the much-admired UK Met Office only targets 70% accuracy for predictions over the next three hours.

** Anyone unconvinced might consider the (financially irrational) demand for lottery tickets.