A headline from yesterday was very intriguing: “Why investors crave a return to the art of stock-picking.” Copious data demonstrate the peril of placing hope in active management. The article argues that since we seem to be in a trend that favors value, it is a good time for managers to pick stocks based on fundamental value metrics.

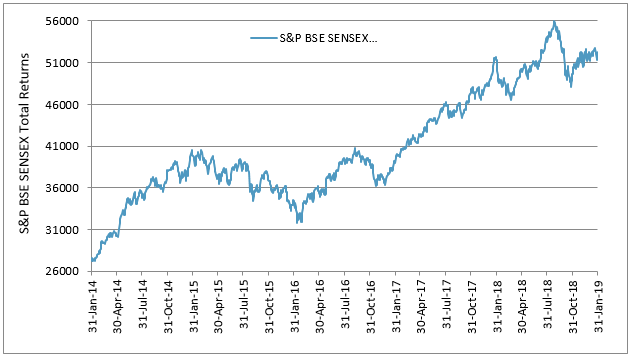

The point that value has recently been beating growth has some merit. The chart below shows the performance cycles for S&P 500 Growth versus S&P 500 Value since 1995. There has been a shift in course since October 2018, with the growth index declining 8% versus just 4% for the value index.

Value, like many other factors, cycles in and out of favor. When it is in vogue, value managers might have an easier time beating the broad market—a value manager might well look good against the S&P 500 when value is beating growth. But that doesn’t necessarily mean that he is adding value as an active value manager.

It is important, in other words, not to conflate the performance advantage of value over growth with the process of stock selection within a value universe. To do otherwise is to confuse style with selection.

The “indicization” of many investment strategies has allowed for cheap access to previously-unavailable factor strategies. The availability of factor indices “…makes the active manager’s life harder. In former days, he could expect to be paid both for providing access to factor exposures as well as for stock selection; today, he’s increasingly limited to stock selection as factor exposure is indicized.”

Value might be back in favor, but that does not imply that beating a value index by stock selection is likely. S&P Dow Jones Indices’ SPIVA report also covers style fund managers— whose results are consistent with those of broad market fund managers. Most style managers underperform their respective benchmarks most of the time.

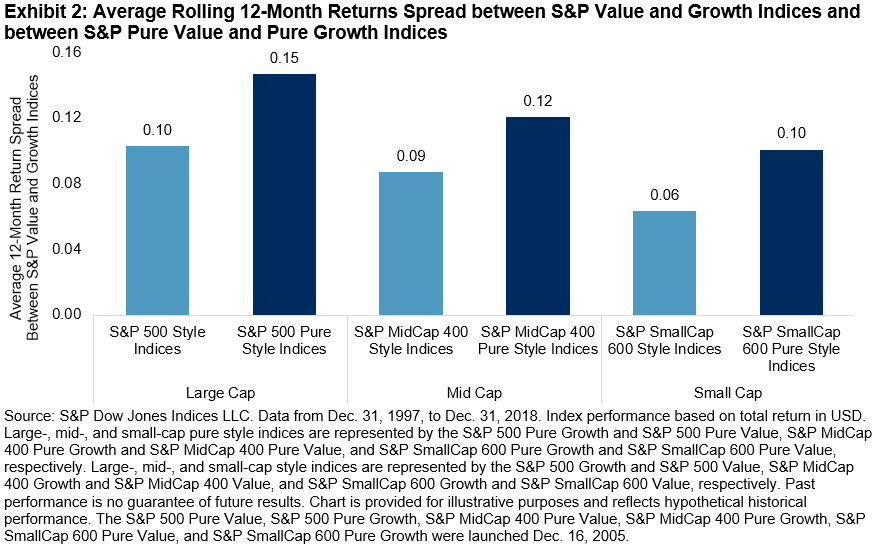

The relative performance of value and growth indices moves in cycles over time, thus market participants could potentially make tactical adjustments to take advantage of short-term deviations in relative value. Exhibit 2 illustrates the style return spread (value minus growth) for the large-cap, mid-cap, and small-cap style and pure style indices.

The relative performance of value and growth indices moves in cycles over time, thus market participants could potentially make tactical adjustments to take advantage of short-term deviations in relative value. Exhibit 2 illustrates the style return spread (value minus growth) for the large-cap, mid-cap, and small-cap style and pure style indices.