This morning brought a report that “retail investors have returned to Wall Street, pouring money into mutual funds focused on US equities for the first time since early 2015, according to data from TrimTabs Investment Research…. ‘Maybe people think, in times of higher volatility, active managers will do a better job,’ Winston Chua, an analyst at TrimTabs, said of the $3.3bn that retail investors put into mutual funds in January.”

They might think that, but they would be wrong.

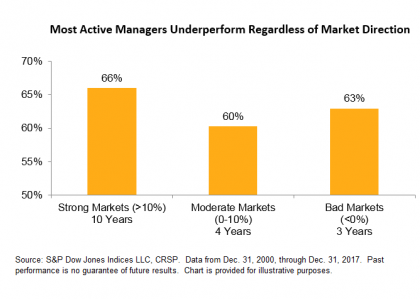

Our SPIVA reports have tracked the relative out- and under-performance of actively-managed mutual funds since 2001. It’s been a rough ride for active managers – in an average year, 64% of large-cap funds underperformed the S&P 500; a majority outperformed in only three years. Seventeen years of data are not a lot, and we should be circumspect about drawing too many conclusions from too few observations. Nonetheless, we can make at least a crude judgment as to whether volatile, weak markets favor active managers.

The graph above divides the SPIVA database into “strong” years (when the market rose by at least 10%), “moderate” years (smaller positive returns), and “bad” years (negative returns). In strong markets, 66% of active funds underperformed the S&P 500; in down years, “only” 63% underperformed. That hardly constitutes persuasive evidence of successful active management in declining markets.

There’s a reason for this finding: most actively-managed funds are more volatile than the benchmark against which they’re evaluated. Moreover, fund volatility tends to persist – a high-volatility fund this year is likely to have above-average volatility next year. The contrast with fund returns – where success this year tells you nothing about the likelihood of success next year – is notable (and, from the active manager’s standpoint, regrettable).

The active-passive debate will continue unabated in 2019, and there may be good reasons why some investors should hire active managers. The expectation of outperformance in a bad market is not one of them.

The posts on this blog are opinions, not advice. Please read our Disclaimers.