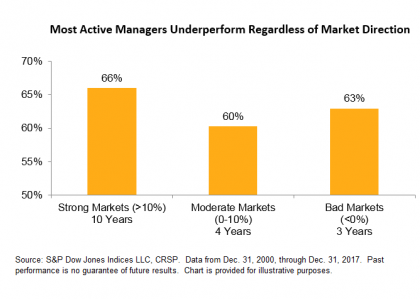

Active managers were welcomed by a disheartening headline this morning. “The 2018 Comeback That Wasn’t for Stock Pickers” highlights that “just 38% of actively managed U.S. stock funds tracked by Morningstar outperformed their counterparts at passively managed funds last year.” This should hardly have been considered shocking. Both long-term and more recent data (notably including our SPIVA reports) document the consistent underperformance of active managers. However, active managers’ relative performance does fluctuate, as evident from the chart below, and some years are clearly tougher than others.

Based on SPIVA data from 2001 to 2017, we’re able to identify some environments in which active managers seemed to deliver relatively better results. Among them are years in which dispersion is high, when low volatility stocks underperform, and when megacaps underperform.

Significantly, none of these conditions occurred in 2018. Dispersion (despite rising in the latter part of the year) was below long term average, the S&P 500 Low Volatility Index was the best performing strategy index, and megacaps narrowly outperformed smaller stocks.

Most active managers underperform most of the time. Nothing in 2018’s data suggests that the year should have been an exception to that general rule.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

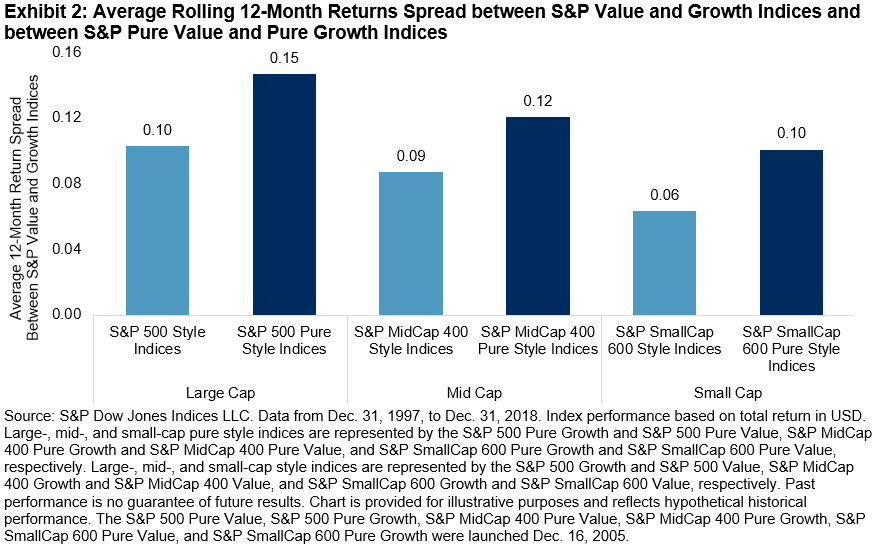

The relative performance of value and growth indices moves in cycles over time, thus market participants could potentially make tactical adjustments to take advantage of short-term deviations in relative value. Exhibit 2 illustrates the style return spread (value minus growth) for the large-cap, mid-cap, and small-cap style and pure style indices.

The relative performance of value and growth indices moves in cycles over time, thus market participants could potentially make tactical adjustments to take advantage of short-term deviations in relative value. Exhibit 2 illustrates the style return spread (value minus growth) for the large-cap, mid-cap, and small-cap style and pure style indices.