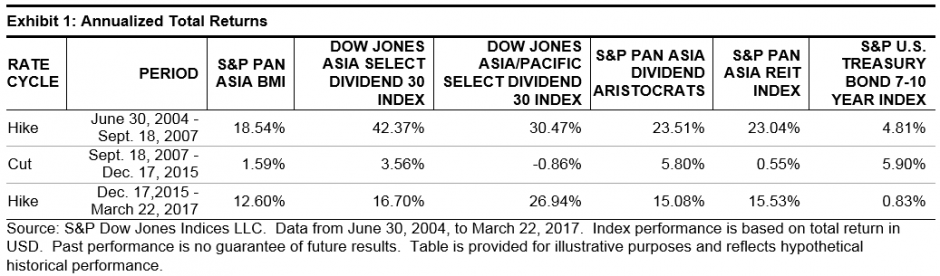

In December 2016, the U.S. Fed raised the interest rate for the second time in the current rate hike cycle. Three more rate hikes were expected for this year, one of which took place in March. In a low interest rate environment, companies that have increasing dividends or offer high dividend yields look attractive to income-seeking market participants. But the yield offered by these companies may be considered less competitive in a rising interest rate environment. Exhibit 1 shows how various S&P DJI Asian dividend and REIT indices have performed in U.S. interest rate cycles since 2004.

During the U.S. rate hike cycle that began June 30, 2004, and lasted until the first rate cut on Sept. 18, 2007, the three S&P Dow Jones Asian Dividend Indices examined, as well as the S&P Pan Asia REIT Index, significantly outperformed the Pan Asia equity benchmark, the S&P Pan Asia BMI, and the S&P U.S. Treasury Bond 7-10 Year Index (see Exhibit 1). However, in the next rate cut cycle lasting from Sept. 18, 2007, to Dec. 17, 2015, the performance trend of these indices reversed, most likely due to the impact of the global financial crisis. The returns of all three Asian dividend indices and the S&P Pan Asia REIT Index lagged the equity benchmark and the S&P U.S. Treasury Bond 7-10 Year Index. The Dow Jones Asia/Pacific Select Dividend 30 Index even recorded negative returns in this rate cut cycle.

In the most recent rate hike cycle starting Dec. 17, 2015, the three Asian dividend indices and the S&P Pan Asia REIT index again delivered significant excess returns compared to the S&P Pan Asia BMI and the S&P U.S. Treasury Bond 7-10 Year Index.

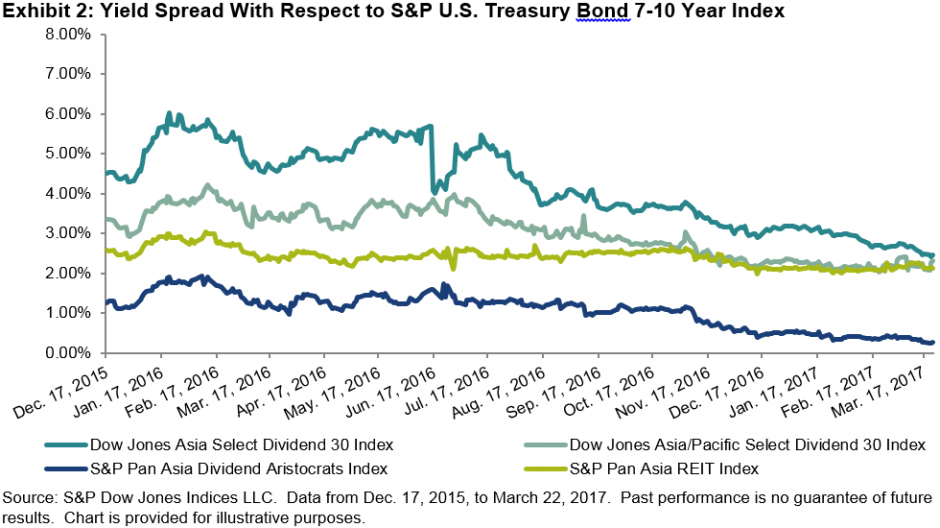

Exhibit 2 shows the yield spread of various dividend indices versus the yield-to-maturity of the S&P U.S. Treasury Bond 7-10 Year Index since Dec. 17, 2015. Apart from the S&P Pan Asia Dividend Aristocrats, both the Dow Jones Dividend Indices and the S&P Pan Asia REIT Index maintained yield spreads of more than 2% after three rate hikes. The S&P Pan Asia REIT Index maintained the most stable yield spread throughout the period studied.

While market participants may expect interest rate hikes to negatively affect Asian high-yield stock performance, it is notable that their performance has been much more sensitive to economic cycles than to U.S. interest rate cycles over the past decade. For the Dow Jones Asian Dividend Indices and the S&P Pan Asia REIT Index, it appears there is still a lot of room for rate hikes before their yield spread will vanish.

The posts on this blog are opinions, not advice. Please read our Disclaimers.