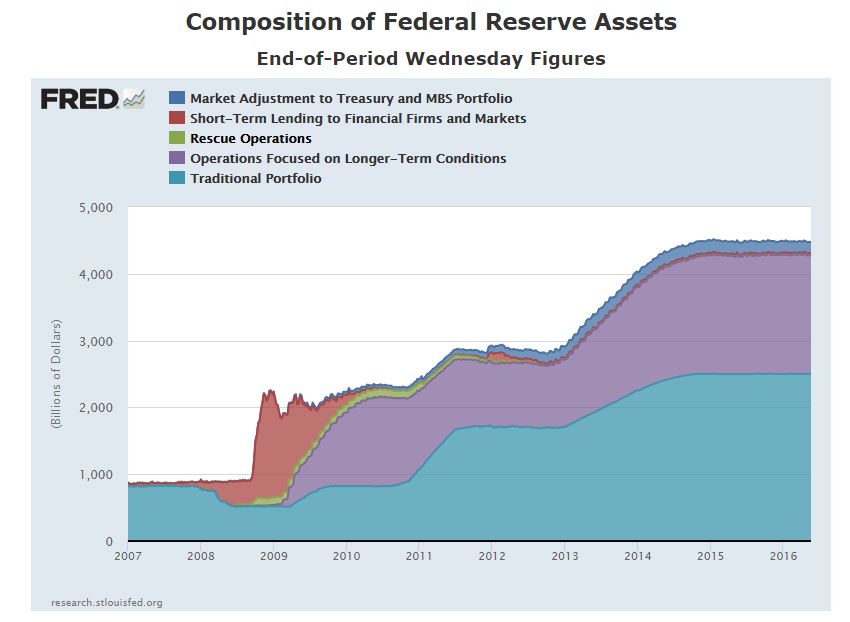

Since the demise of Bear Stearns and Lehman Brothers in 2008, Federal Reserve policy has focused on containing market turmoil and disruption. Current Fed policy built on a massively expanded balance sheet (first chart); the quantitative easing that inflated the balance sheet and the Fed funds rate glued to the zero lower bound (second chart). This all resulted from efforts to limit turmoil and curb disruption. Through the last ten years, financial market stability was as equally important as low inflation and unemployment.

This is about to change. The Minutes of the April 26-27 FOMC meeting include a discussion of the relationship between monetary policy and financial stability:

“Most participants judged that the benefits of using monetary policy to address threats to financial stability would typically be outweighed by the costs associated with deviations from the Committee’s employment and price-stability objectives induced by such actions; some also noted that the benefits are highly uncertain.”

The Fed is not abandoning the markets and ignoring market turmoil. Rather, it is recognizing that policy actions designed to temper any market bump can get in the way of their dual mandate of low inflation and full employment. They note that there may be times when market disruption is so severe that failing to respond would damage the Fed’s policy goals:

“Nonetheless, participants generally agreed that the Committee should not completely rule out the possibility of using monetary policy to address financial stability risks, particularly in circumstances in which such risks significantly threatened the achievement of its dual mandate and when macroprudential tools had been or were likely to be ineffective at mitigating those risks.”

For ten or more years commentators have cited the “Fed Put,” the idea that if markets dived the Fed would step in with low interest rates and liquidity to prop things back up. Many investors believed that the Fed was providing downside protection to help people exit positions in a collapsing market.

Looking back the Fed Put was more myth than reality. The comments in the April 26-27 Minutes suggest that the Put is no more.

Charts from St. Louis Federal Reserve Bank FRED economic data

The posts on this blog are opinions, not advice. Please read our Disclaimers.