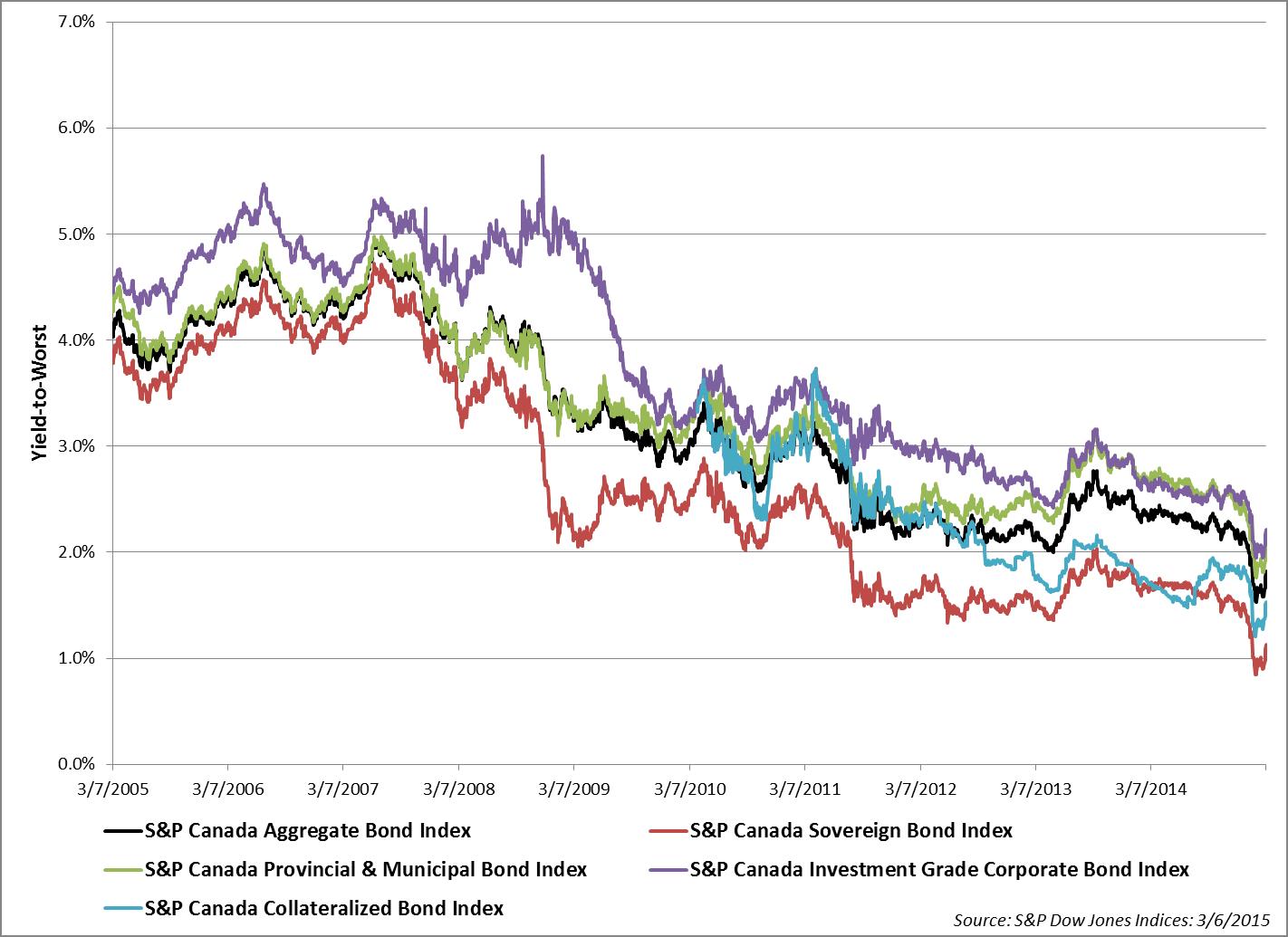

The yield-to-worst of the S&P Canada Aggregate Bond Index touched a low of 1.53% on February 2, 2015 after 10 years of history in which the index’s yield had been as high as 4.96% back in June 2007. After a solid total return of 4.35% in January, the index gave up a little ground and returned -0.11% for February. March has come in like a lion, as it has wiped out 2% of returns as of March 6, 2015. As of the same date, the index is returning 2.15% YTD.

The components of the S&P Canada Aggregate Bond Index are all wider by an average of 29 bps as of March 6, 2015; S&P Canada Sovereign Bond Index (28 bps), S&P Canada Provincial & Municipal Bond Index (32bps), S&P Canada Investment Grade Corporate Bond Index

(26 bps), and S&P Canada Collateralized Bond Index (32 bps).

Last week, Canadian bonds sold off for the entire week. The Bank of Canada held its policy interest rate unchanged at 0.75%, and backed up the no action with statements that the level is the appropriate rate. This is in contrast to the Jan. 21, 2015 cut of 25 bps from the 1% level in response to lower oil prices. The rate cut was a complete reversal of policy and tone for the BOC.

After a stellar 2014 in which the S&P Canada Provincial & Municipal Bond Index returned 10.48%, this index is still out in front as of March 6, 2015, returning 2.76% YTD. Provincials & Municipals Index had a strong January (+5.58%), although they are getting hit the hardest in March, at -2.57% as of March 6, 2015.

The best performer in the recent downtrend has been the S&P Canada Collateralized Bond Index losing only -0.39% of return MTD.

Source: S&P Dow Jones Indices LLC. Data as of March 6, 2015. Past performance is no guarantee of future results. Charts and graphs are provided for illustrative purposes.

The posts on this blog are opinions, not advice. Please read our Disclaimers.