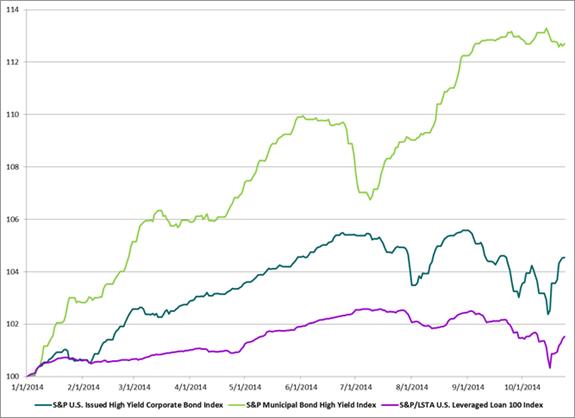

The senior bank loan or leverage loan market as measured by the S&P/LSTA U.S. Leveraged Loan 100 Index ticked up last week as the index has returned +0.10% month-to-date and 1.56% year-to-date. Last week’s price action of the secondary loan market assisted the index in clawing back against a month-to-date loss from the beginning of the week of -0.51%. Much of last week’s leveraged loan positive return accompanied a 3.2% rally in equities (S&P 500) and a 0.8% high-yield bond rally as measured by the S&P U.S. Issued High Yield Corporate Bond Index. Also aiding in last week’s increase in demand for loans was the fact that new-issue launches have slowed to a trickle.

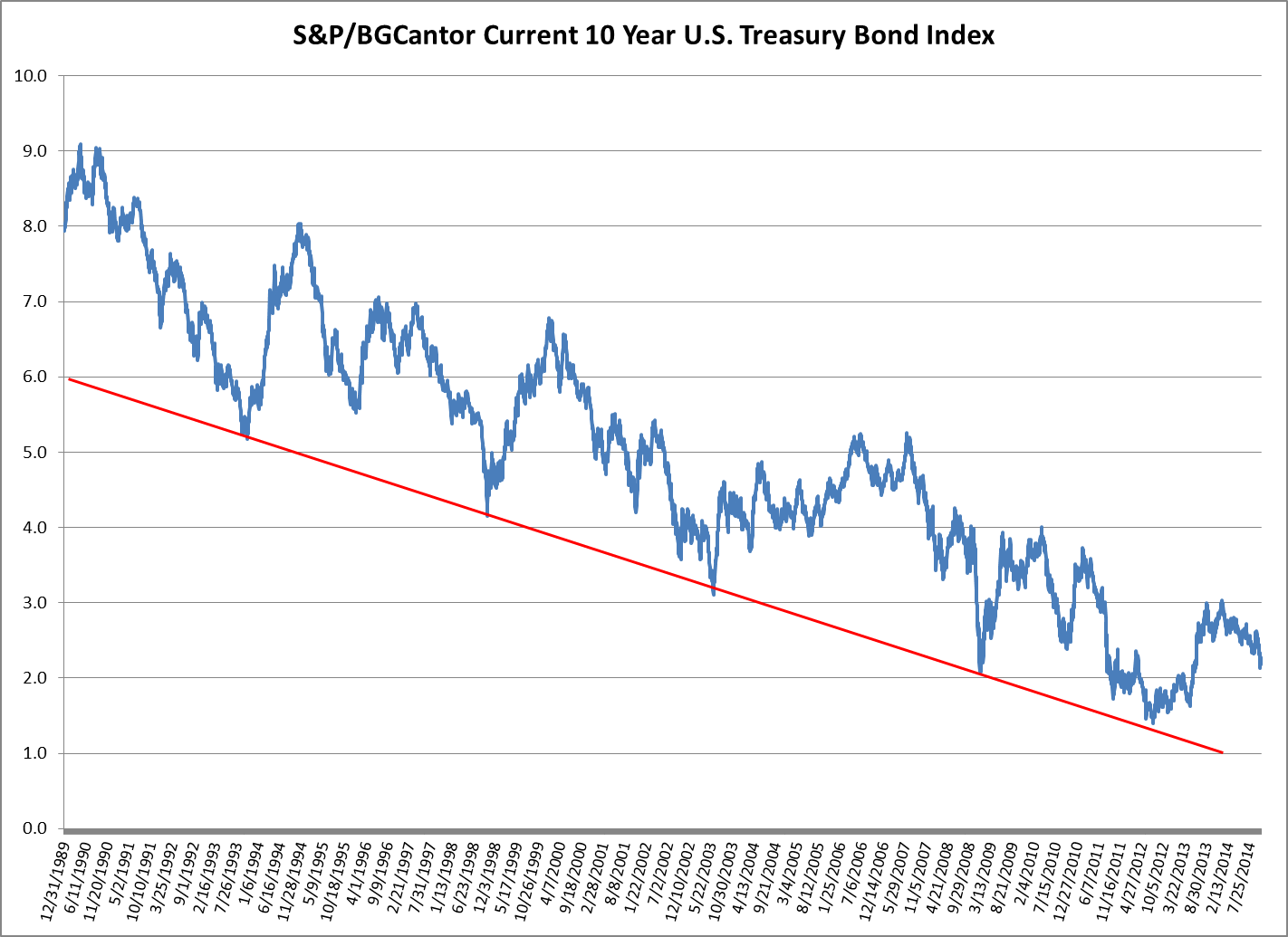

Currently the 10-year Treasury is yielding 2.25%, 2 basis points lower than Friday’s close of 2.27% for the S&P/BGCantor Current 10 Year U.S. Treasury Index. If the markets are concerned of news from this week’s FOMC Meeting announcements, they haven’t shown it. To date the more speculative indices S&P/LSTA U.S. Leveraged Loan 100 Index, S&P U.S. Issued High Yield Corporate Bond Index and S&P Municipal Bond High Yield Index are returning 0.10%, 1.11% and a just slightly negative number of -0.16%, respectively.

Market sentiment can change quickly though and if news from the FOMC does undermine the current risk-on environment; leveraged loans could be the least volatile in price. Compared to the municipal high yield’s 7.35 year duration and the U.S. Issued High Yield’s duration of 4.86%, the weekly reviewed leverage loan index will be least effected to the change in rates.