Market-cap-weighted indices like the S&P 500® that offer a broad measure of the market have long served as the foundation of passive investing. With valuations at elevated levels and sector concentration—particularly in technology—near historic highs, we examine alternative weighting methods that may provide broader and complementary views.

Revenue weighting offers a complementary approach: by weighting companies proportionally to their top-line sales, the S&P 500 Revenue-Weighted Index, S&P MidCap 400® Revenue-Weighted Index and S&P SmallCap 600® Revenue-Weighted Index1 anchor weights to economic activity rather than market value. These indices may exhibit broader sector diversification and lower valuation multiples, while maintaining the characteristics of passive investing.

In this blog, we review the historical performance, risk-adjusted returns, valuation characteristics and diversification effects of revenue-weighted index construction.

Long-Term Outperformance versus Benchmarks

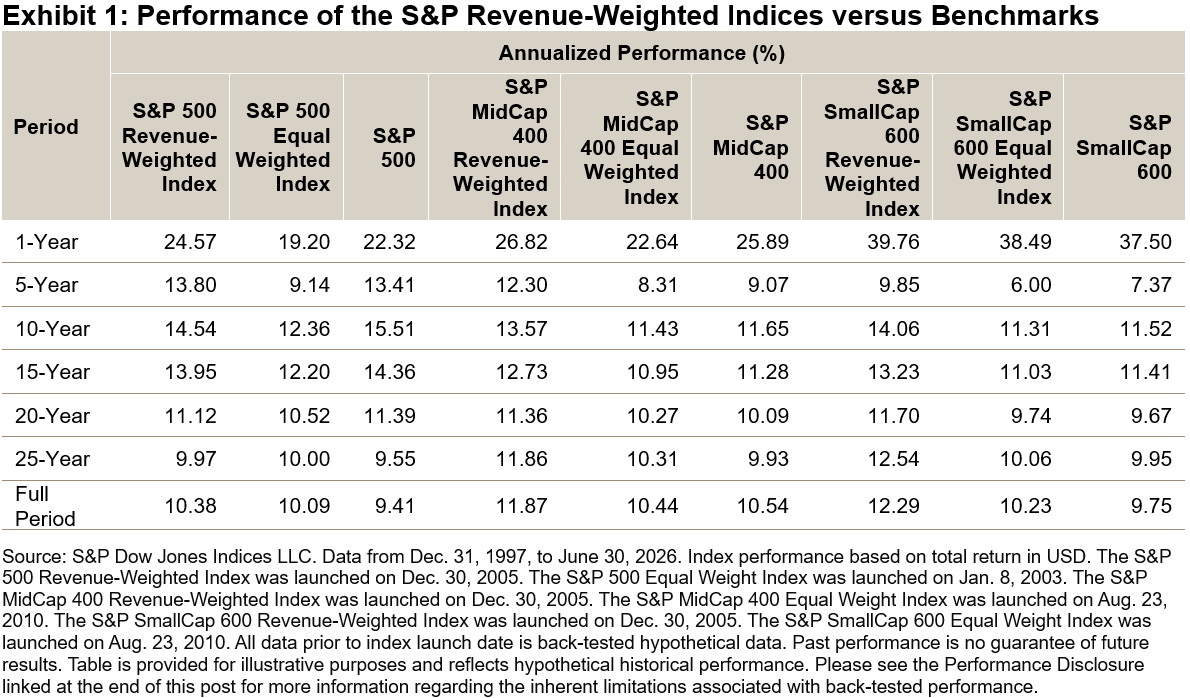

The S&P 500 Revenue-Weighted Index has outperformed the S&P 500 as well as the S&P 500 Equal Weight Index across both short- and long-term periods. This trend extends to mid- and small-cap equities; the S&P MidCap 400 Revenue-Weighted Index and S&P SmallCap 600 Revenue-Weighted Index have also outperformed their respective equal- and market-cap-weighted benchmarks (see Exhibit 1).

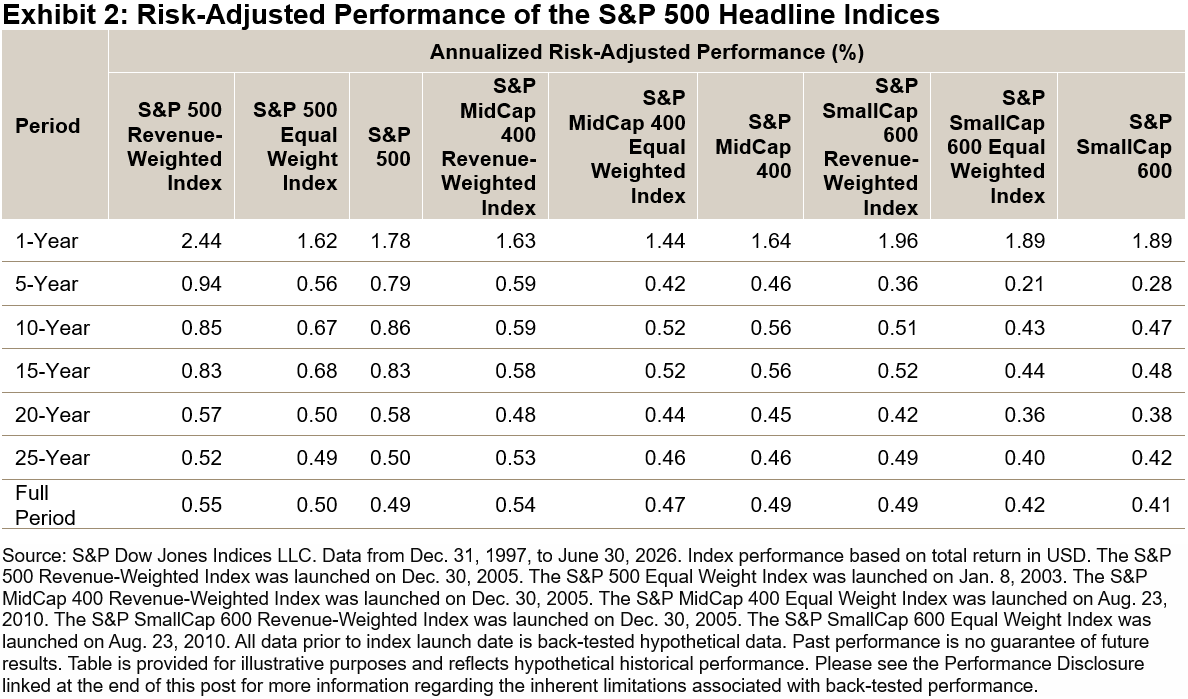

Enhanced Historical Risk-Adjusted Performance

As illustrated in Exhibit 2, the revenue-weighted indices also showed superior risk-adjusted performance compared to their equal- and market-cap-weighted counterparts, across both short- and long-term horizons.

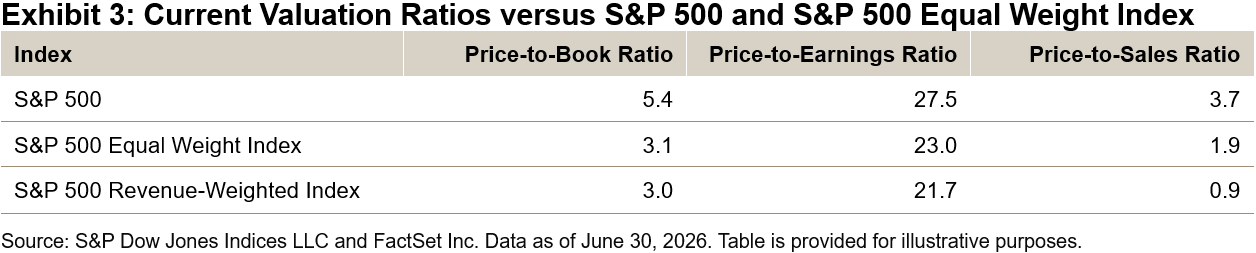

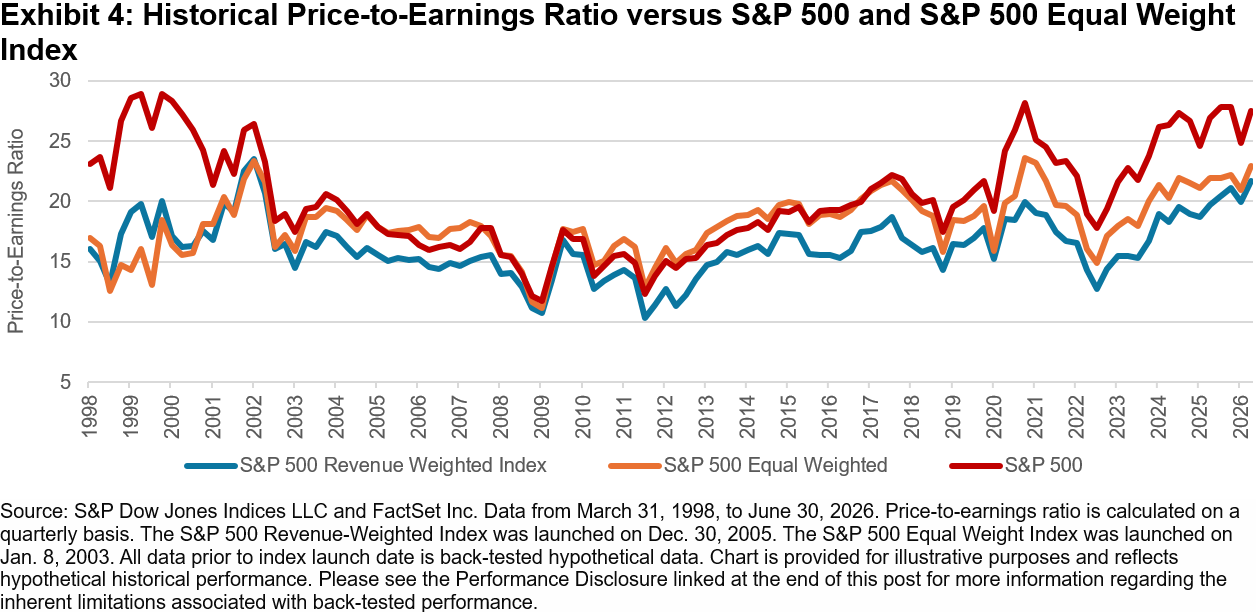

Lower Valuations Relative to Benchmark Universes

Exhibit 3 illustrates that, as of June 30, 2026, the S&P 500 Revenue-Weighted Index was trading at lower valuation ratios compared to both the S&P 500 and the S&P 500 Equal Weight Index. This trend has also been observed historically over the long term, as shown in Exhibit 4. Additionally, the mid-cap and small-cap revenue-weighted versions consistently demonstrated lower price multiples relative to their respective benchmarks.

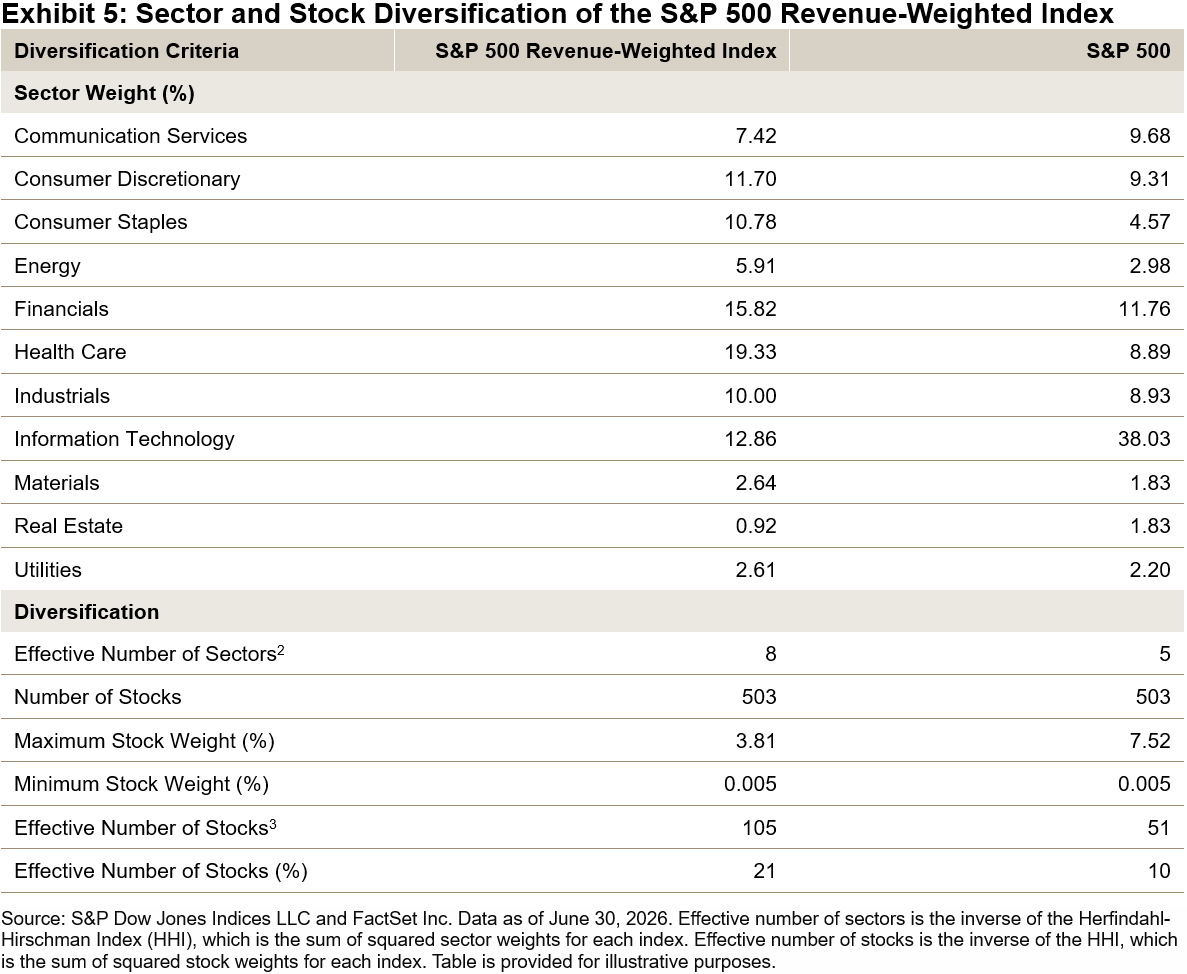

Sector Diversification

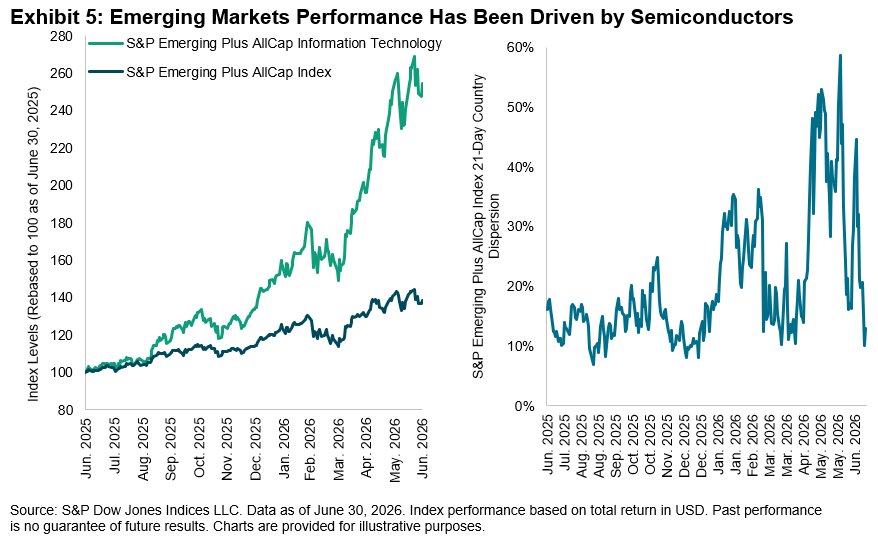

As illustrated in Exhibit 5, the Information Technology sector comprised 38.03% of the S&P 500 as of May 31, 2026—representing an all-time high. In comparison, the S&P 500 Revenue-Weighted Index demonstrated greater sector diversification, with less dispersion across sector and individual stock weights, and a higher effective number of sectors and stocks. While sector weights tend to be more balanced in mid- and small-cap indices, revenue weighting still provides a differentiated view relative to traditional benchmarks.

Conclusion

Revenue-weighted indices can be complementary to traditional market-cap-weighted indices. By anchoring company weights to revenue, these indices have historically preserved a broad equity view while reducing concentration and valuation risk. Over the back-tested history, the S&P 500 Revenue-Weighted Index, S&P MidCap 400 Revenue-Weighted Index and S&P SmallCap 600 Revenue-Weighted Index have exhibited strong total returns and risk-adjusted outperformance, along with a more pronounced value tilt and higher diversification.

1 Please refer to the S&P Revenue-Weighted Index Series Methodology for more details.

2 Effective number of sectors is the inverse of the Herfindahl-Hirschman Index (HHI), which is the sum of squared sector weights for each index.

3 Effective number of stocks is the inverse of the Herfindahl-Hirschman Index (HHI), which is the sum of squared stock weights for each index.

The posts on this blog are opinions, not advice. Please read our Disclaimers.