How has index concentration shifted historically and why might a diversified, cap-weighted benchmark like the S&P 500 already be tracking tomorrow’s market giants? S&P DJI’s Ben Vörös sits down with Tim Edwards to discuss Tim’s latest research, In the Shadows of Giants, and examine whether the dominance of a few large companies may be a signal of risk or opportunity for market participants.

The posts on this blog are opinions, not advice. Please read our Disclaimers.The Market Measure: In the Shadows of Giants

130 Years of The Dow: Why It Still Matters to Asia-Pacific

Latin Markets: Still Dancing to the Same Beat

Forecasting Tomorrow’s Dividends: Introducing the S&P/TSX Composite High Dividend Growth Index

SPIVA Special Report: Heroes in Haystacks

The Market Measure: In the Shadows of Giants

130 Years of The Dow: Why It Still Matters to Asia-Pacific

- Categories S&P 500 & DJIA

- Tags Asia Pacific, DJIA, Dow Jones Industrial Average, The Dow, U.S. equities

How Wall Street’s Oldest Barometer Impacts Markets from Singapore to Seoul

When Charles Dow published his first industrial average on May 26, 1896, Asia’s great stock exchanges had barely been born. Tokyo’s bourse was just 15 years old; Hong Kong’s exchange had yet to open its doors. Today, many Asian markets take cues from the close of the Dow Jones Industrial Average® (DJIA) before trading begins the next morning. That overnight signal—whether positive or negative—often influences sentiment across Asia-Pacific markets at the open.

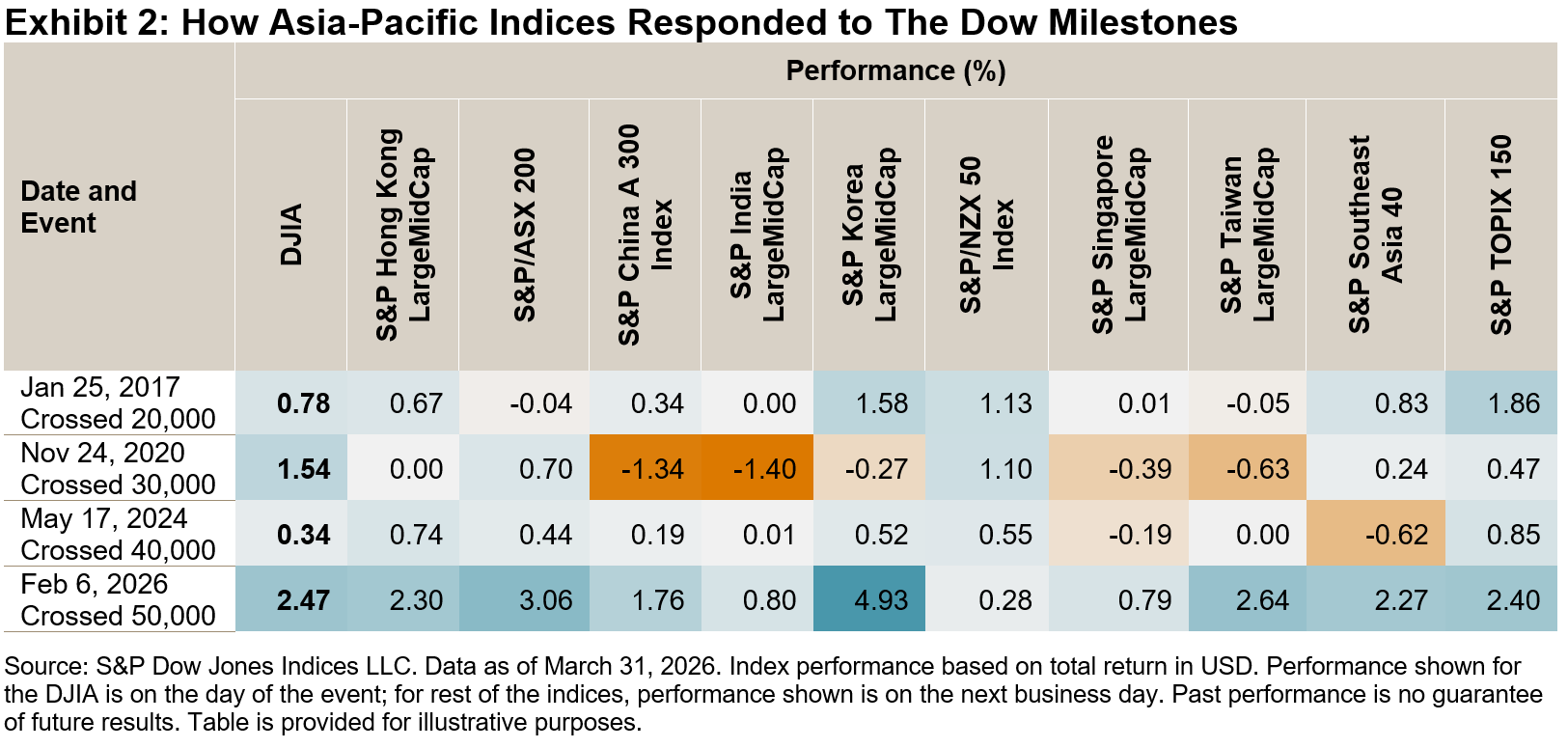

The Dow® crossed 50,000 for the first time on Feb. 6, 2026, a milestone that triggered a surge across Asia-Pacific indices the following session. The relationship between The Dow and the Asia-Pacific region has only deepened over 130 years as supply chains, capital flows and technology have woven the East and West into a single market fabric.

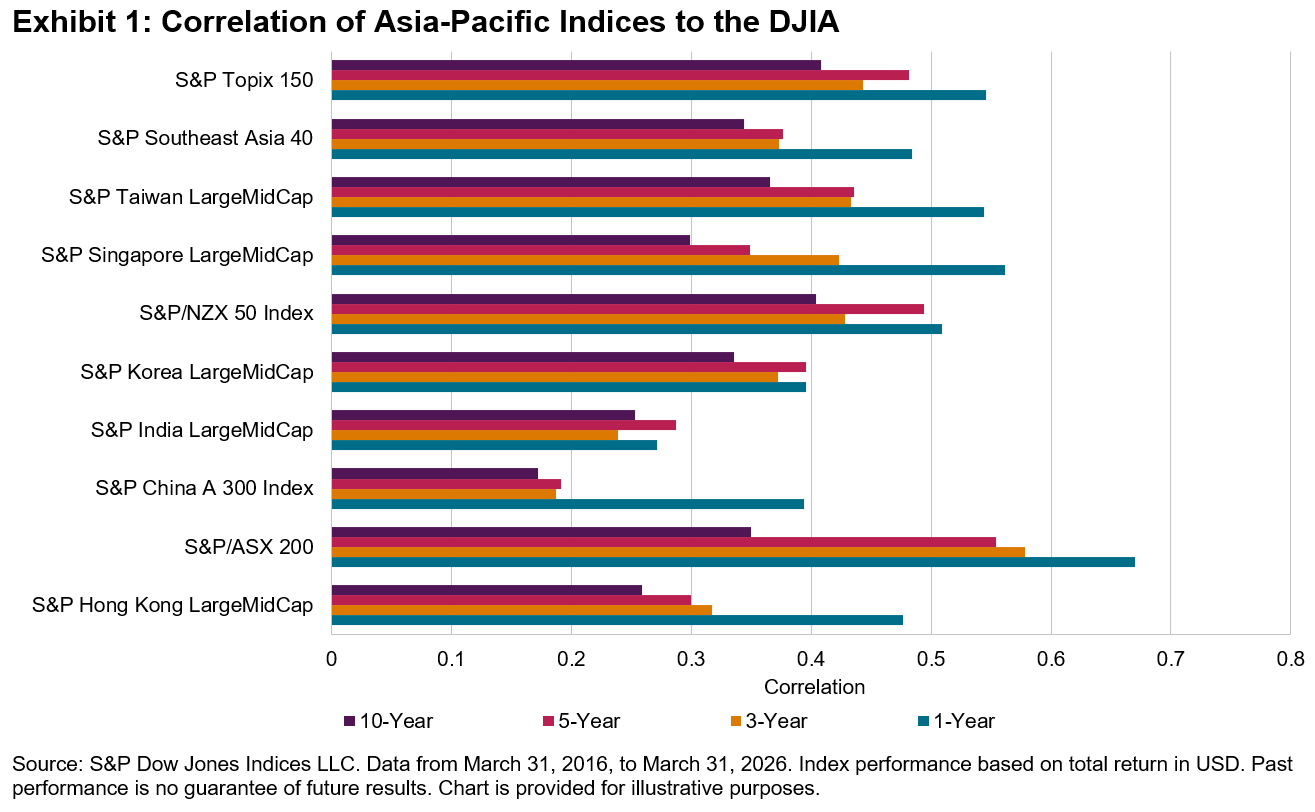

Why the DJIA Matters More than Ever for Asia-Pacific

Asia-Pacific markets open hours before Wall Street closes, making the prior U.S. session a critical input. Markets like Hong Kong, Japan, South Korea, Singapore, Australia, New Zealand and India show statistically significant correlation with The Dow, particularly during periods of global stress such as the 2008 Financial Crisis and the 2020 COVID-19 pandemic shock. Sharp moves in U.S. equities often influence the next trading session in Asia-Pacific.

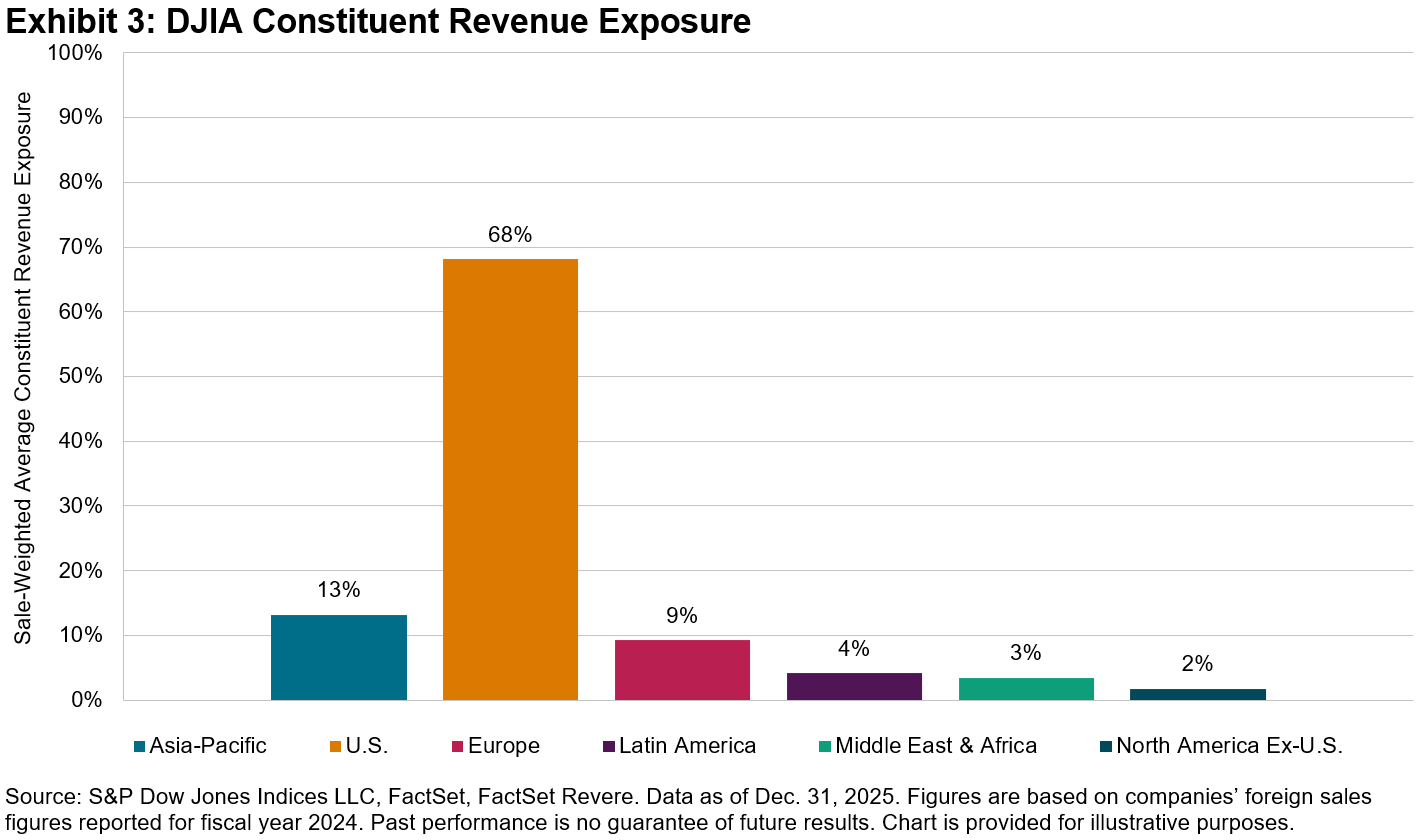

Additionally, the 30 DJIA components derive significant revenues from Asia-Pacific. In fact, outside of the U.S., Asia-Pacific is the region from which DJIA companies derive the largest revenue.

Perhaps the most tangible measure of the DJIA’s relevance to Asia-Pacific is the growing shelf of locally listed ETFs and funds that give retail and institutional investors in the region direct access to the index. Over the past two decades, global and regional asset managers have steadily expanded access to products that track The Dow for Asian market participants.1

What began with the first listed product in Singapore in 2002 has since evolved into a broader regional presence, with DJIA-related products now listed in markets including Taiwan, Japan and South Korea. This expansion not only offers market participants greater choice, but also reflects the enduring popularity and influence of The Dow across Asia-Pacific markets.

Conclusion

After 130 years, the Dow Jones Industrial Average remains a reference point for Asia-Pacific markets. Its daily movements serve as vital signals, influencing trading sentiment from Singapore to Seoul before the local exchanges even open. The Dow’s milestones—like crossing 50,000—have at times been reflected in regional market performance, underscoring the ties between Wall Street and the East. With DJIA companies generating a meaningful share of revenue from Asia-Pacific and the proliferation of The Dow-linked investment products in the region, the index’s relevance has only grown. As global markets become ever more interconnected, The Dow’s legacy endures—not just as a historic barometer, but as a living bridge between economies, helping to guide Asia-Pacific through both calm and crisis.

1 For a complete list of products linked to S&P DJI indices, please visit our Index-Linked Products page.

The posts on this blog are opinions, not advice. Please read our Disclaimers.Latin Markets: Still Dancing to the Same Beat

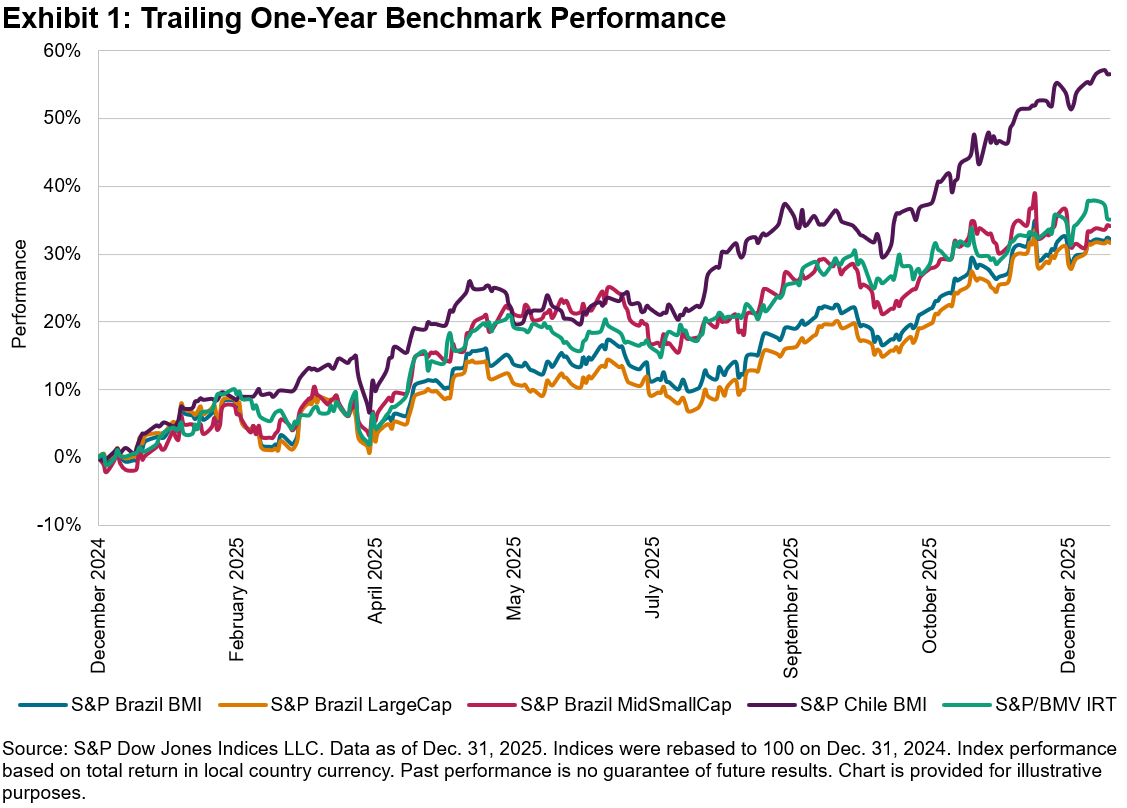

Just as Latin American musicians dominated global charts in 2025, the region’s equities delivered quite the performance last year. While markets navigated shifting interest rates and economic transitions, Latin America stood out as a top-performing region worldwide. The S&P Latin America BMI hit a high note, surging by 53.8% for the year, outperforming the S&P Global BMI by 31.8% in U.S. dollar terms.

As Exhibit 1 illustrates, this growth was widespread. Chile was the clear standout, with the S&P Chile BMI rising 56.6%, followed by Mexico’s S&P/BMV IRT at 35.2%. Brazil also experienced a robust recovery from its 2024 slump, with the S&P Brazil BMI up 32.2%.

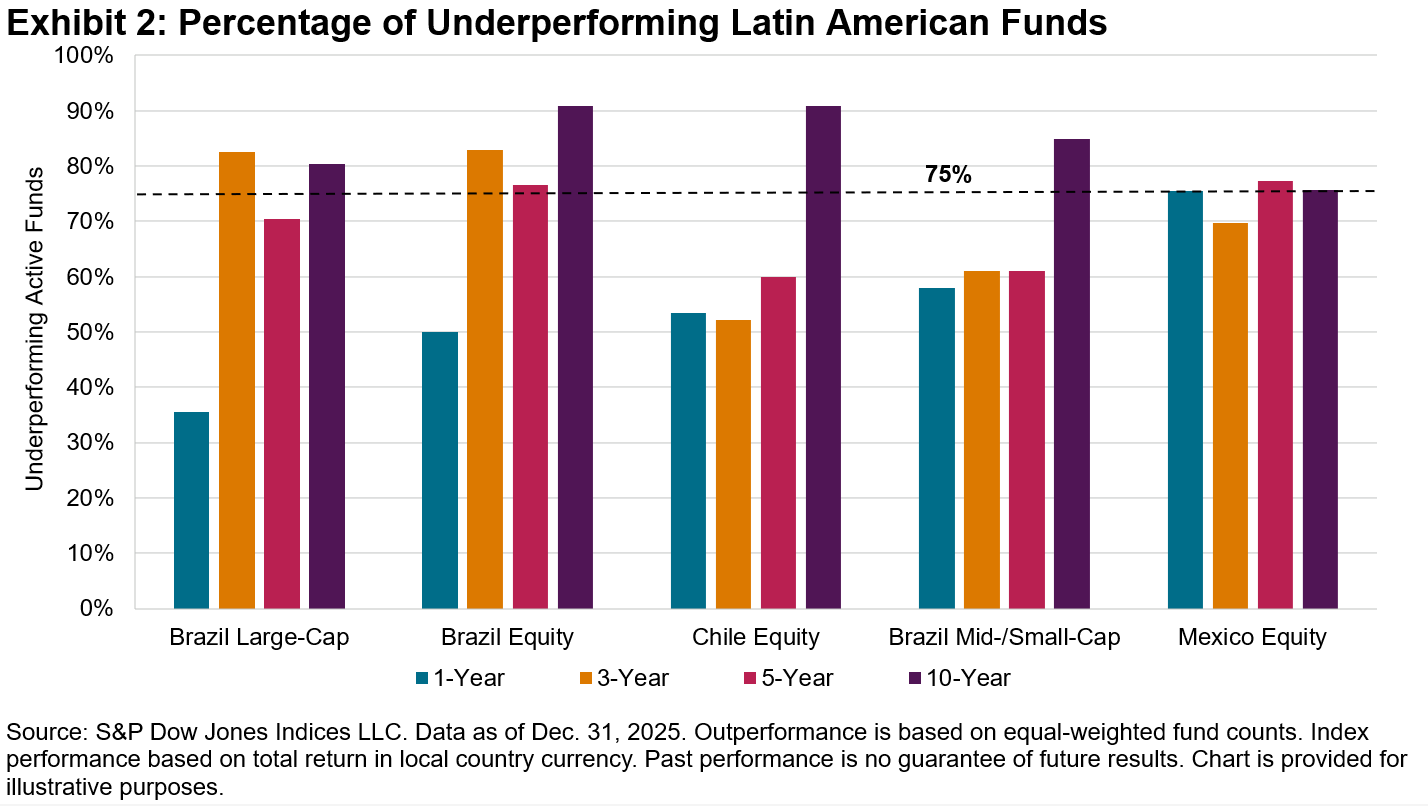

Did active funds sing in tune with the broad rally or end up off-key? The results, detailed in the SPIVA Latin America Year-End 2025 Scorecard, were mixed. While active large-cap equity funds in Brazil fared relatively well, the majority of active funds in all other regional categories failed to capture the full extent of the 2025 surge. As Exhibit 2 shows, over a 10-year horizon, high underperformance (over 75%) remained the undeniable norm across all categories.

To understand why active managers struggled in some countries but succeeded in others in the short term, we can start by looking at market skew and leadership concentration.

In 2025, Latin American markets experienced notable disparities in performance distributions. In Mexico, for example, the S&P/BMV IRT exhibited moderately positive skew. Only 10 stocks (27.0%) outperformed the benchmark, meaning active managers faced a high probability of selecting underperformers. Chile showed a similar, albeit slightly less skewed outcome, with the strongest performers heavily concentrated among the highest-weighted stocks.

Brazil offered a fascinating case study in active management dynamics. While the broader Brazilian equity market saw a relative absence of positive skewness, with over half of its components (51.6%) outperforming the S&P Brazil BMI, the S&P Brazil LargeCap told a different story.

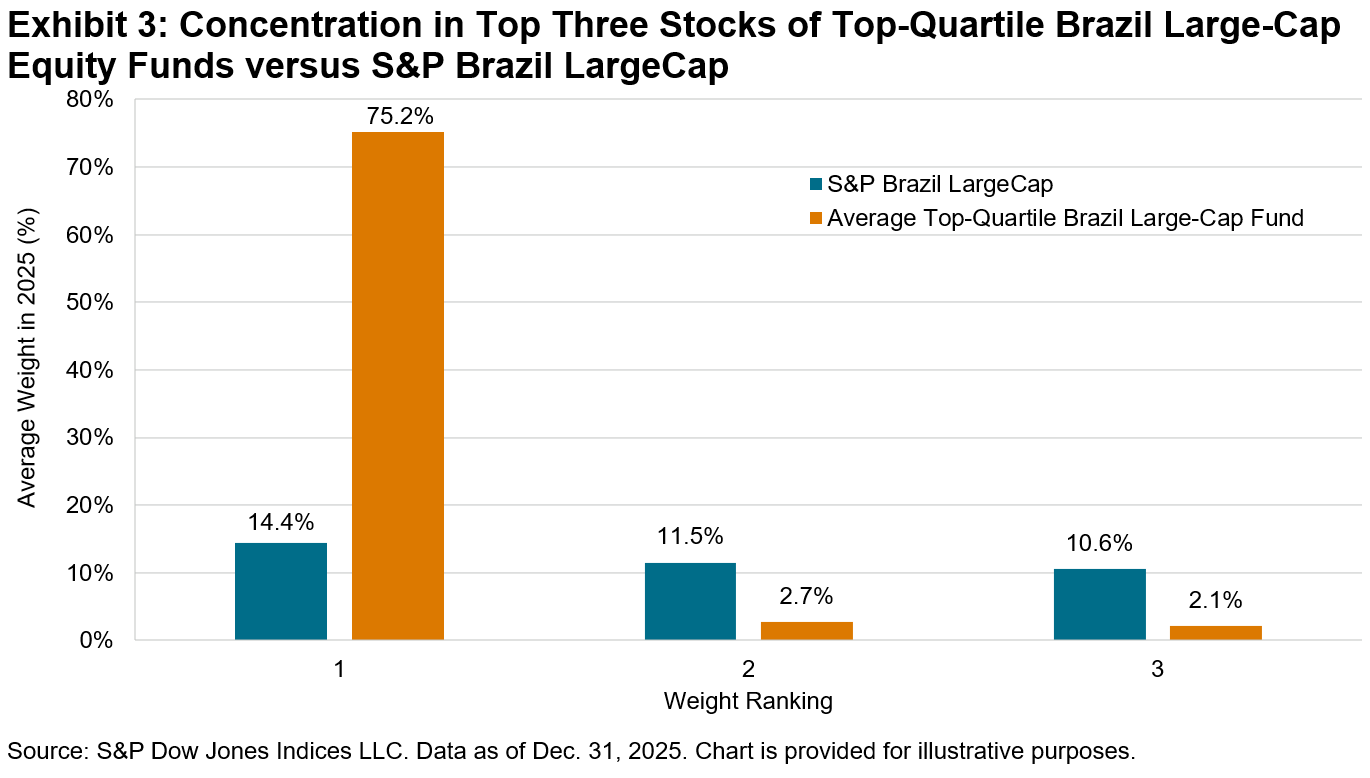

Typically, when a few mega-cap stocks drive a market’s index performance, active funds struggle to keep pace due to portfolio diversification tendencies that shift them away from significant concentration. In 2025, however, Brazil proved to be an exception. Active Brazil Large-Cap funds posted their best results since 2021, aided by highly concentrated positions. While the S&P Brazil LargeCap’s top three constituents accounted for 36.5% of its weight, the average total weight of the top three holdings among top-quartile Brazil Large-Cap equity funds was 80.0%, as shown in Exhibit 3. Perhaps even more remarkably, the average weight of the largest holding in top-quartile Brazil Large-Cap equity funds was 75.2%, illustrating a tilt toward massive single-stock concentration in the pursuit of outperformance.

While riding the momentum of a few large stocks provided a winning ticket for Brazilian large-cap managers in 2025, history serves as a cautionary tale. Relying heavily on a concentrated handful of stocks has carried significant risk when market leadership rotates.

The newly released Latin America Persistence Scorecard Year-End 2025 highlights this exact challenge, answering a critical question: Can these pockets of outperformance be attributed to genuine skill, or are they the result of fleeting luck?

If outperformance were driven by repeatable skill, we would expect it to persist. Instead, the data shows that active management success is overwhelmingly short-lived. Among the 405 funds across Brazil, Chile and Mexico that placed in the top quartile in 2021, a mere 1.2% managed to remain in the top tier over the following four years.

Looking closely at the equity markets, the drop-off was stark. For broad Brazil Equity funds, only 1 out of 81 top-quartile funds from 2021 (1.2%) maintained its status through 2025. In Chile and Mexico, the persistence rate completely vanished; not a single top-quartile equity fund from 2021 maintained its ranking over the subsequent four years.

Furthermore, the data highlighted the possible severe long-term consequences of getting caught on the wrong side of market concentration. Over two consecutive five-year periods, for example, 57.1% of top-quartile Chile Equity funds did not just lose their top-tier status; they fell to the bottom quartile or were liquidated entirely.

Ultimately, 2025 was a record-breaking year for Latin American equities in an absolute sense. Yet, from a relative perspective, the underlying mechanics of skew and concentration proved difficult for most active managers to navigate. The past year may have offered brief pockets of active success in markets like Brazil, but the long-standing results from the SPIVA and Persistence Scorecards continue to remind us that the song remains the same; over the long term, luck has proven fleeting, and consistent outperformance has remained rare.

The posts on this blog are opinions, not advice. Please read our Disclaimers.Forecasting Tomorrow’s Dividends: Introducing the S&P/TSX Composite High Dividend Growth Index

Introduction

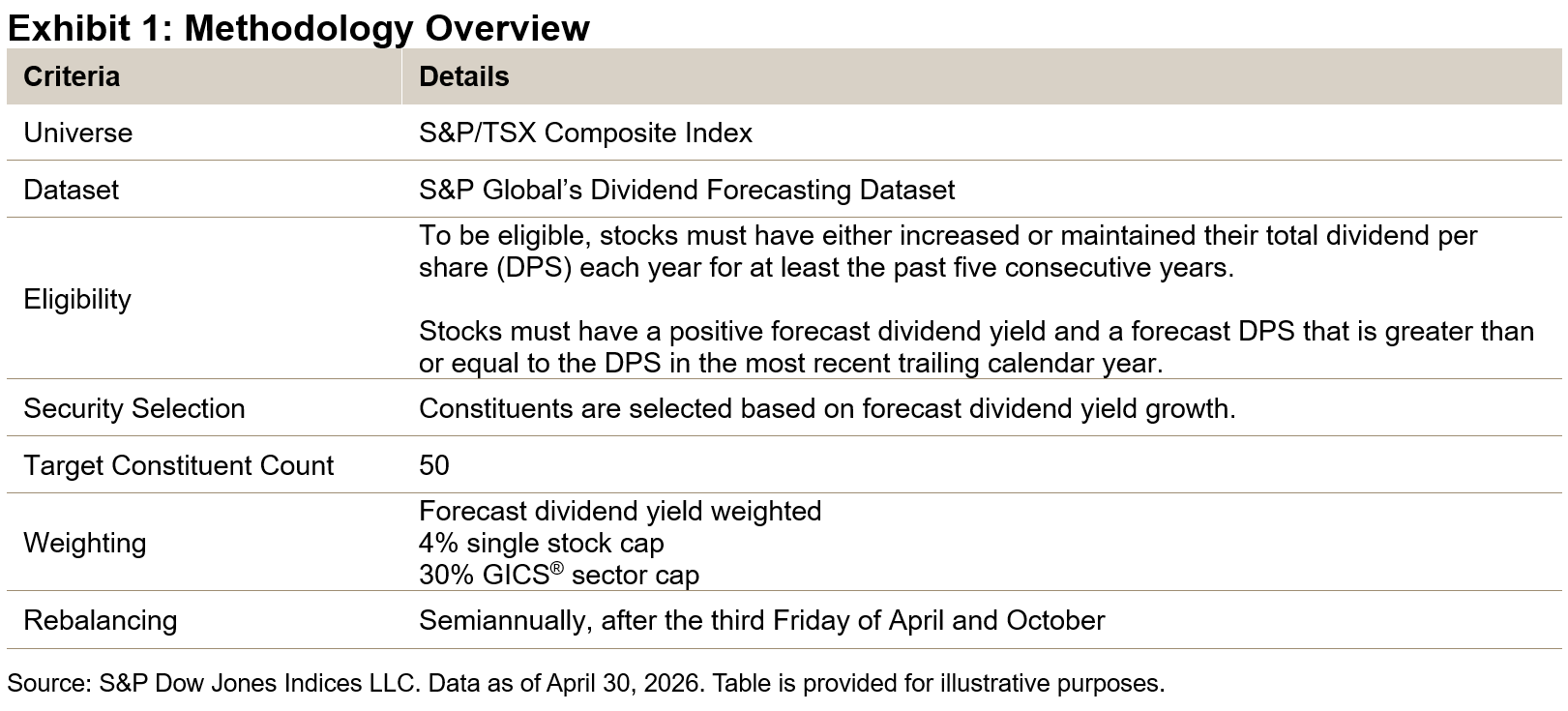

As an industry leader in dividend index development, S&P Dow Jones Indices (S&P DJI) is committed to launching new and innovative dividend indices across global markets. The newly launched S&P/TSX Composite High Dividend Growth Index reflects this, representing the first application of the S&P Global Market Intelligence Dividend Forecasting Dataset within the S&P/TSX Composite Index universe. The index employs a distinct methodology, selecting companies that have demonstrated stable or growing dividends over the past five years and are projected to deliver the highest dividend yield growth going forward.

In this blog, we will explore the index’s methodology, historical outperformance, enhanced dividend yield and growth, as well as sector allocations versus the S&P/TSX Composite Index.

Methodology Overview

To be eligible for selection, constituents must have maintained or grown their dividends for at least five consecutive years, and they must also be projected to continue to do so over the next 12 months.

The index selects the top 50 constituents exhibiting the highest forecast dividend yield growth, determined by subtracting the 12-month historical yield from the 12-month forecast yield. Constituents are then weighted according to their forecast dividend yield, subject to stock and sector constraints.1

Performance Comparison

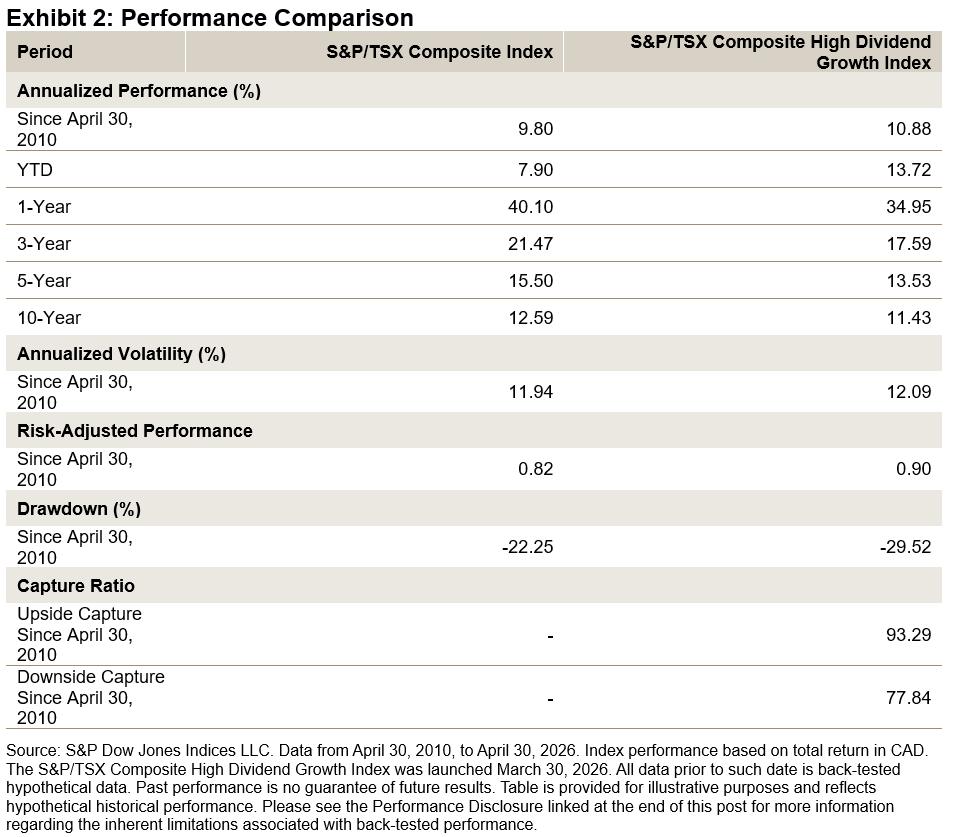

Using back-tested data starting April 2010, the S&P/TSX Composite High Dividend Growth Index outperformed the S&P/TSX Composite Index, both on an absolute and risk-adjusted basis (see Exhibit 2). Additionally, the index has demonstrated asymmetric capture ratios, participating in over 93% of the benchmark’s upside while the downside capture ratio was less than 78%.

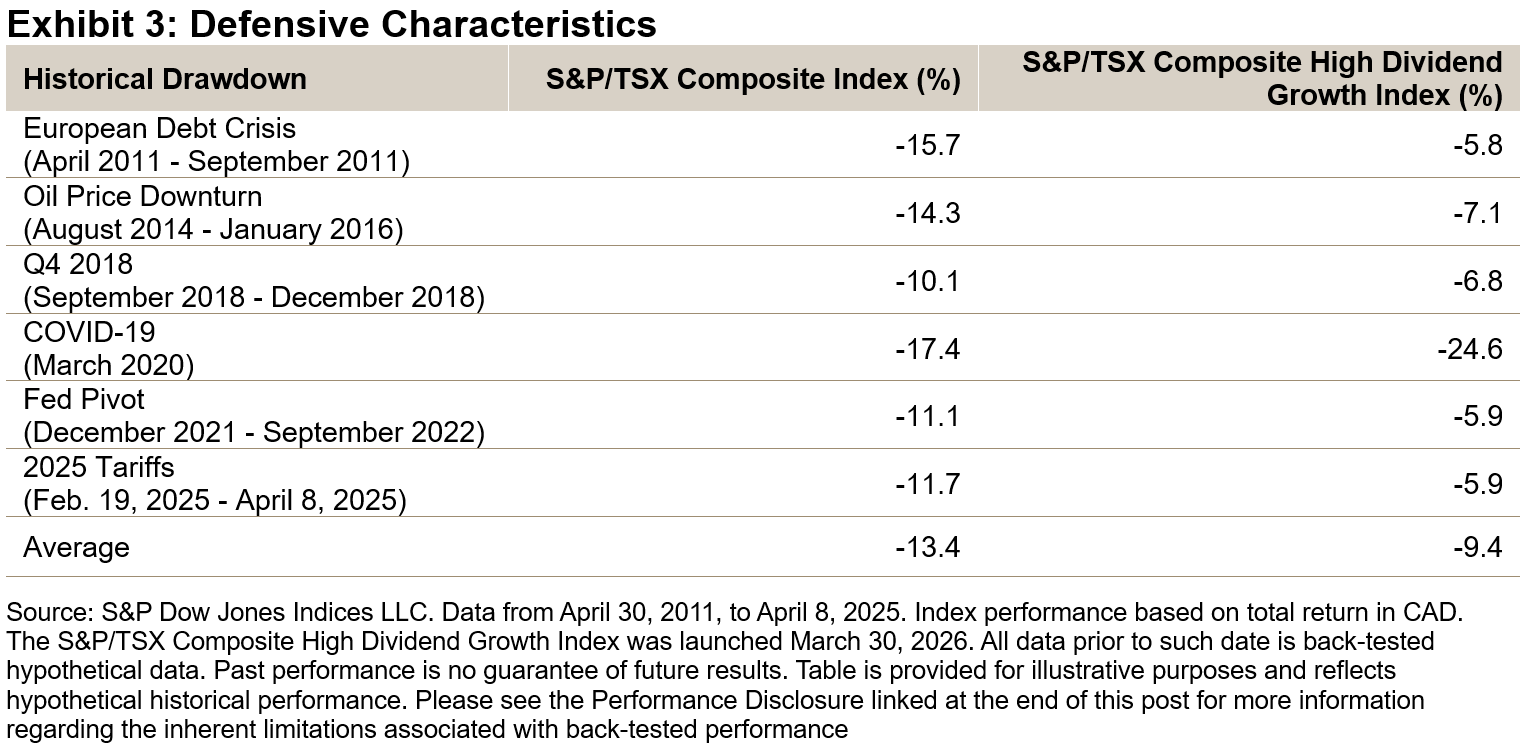

Beyond its strong downside capture, the index has shown notable downside protection during historical drawdown periods over the back-tested period, outperforming the S&P/TSX Composite Index in five out of six major drawdowns, with the exception of the March 2020 COVID-19 downturn. On average, the S&P/TSX Composite High Dividend Growth Index experienced a drawdown of -9.4%, compared to -13.4% for the S&P/TSX Composite Index, equating to less than 70% of the benchmark’s downside.

Dividend Comparison

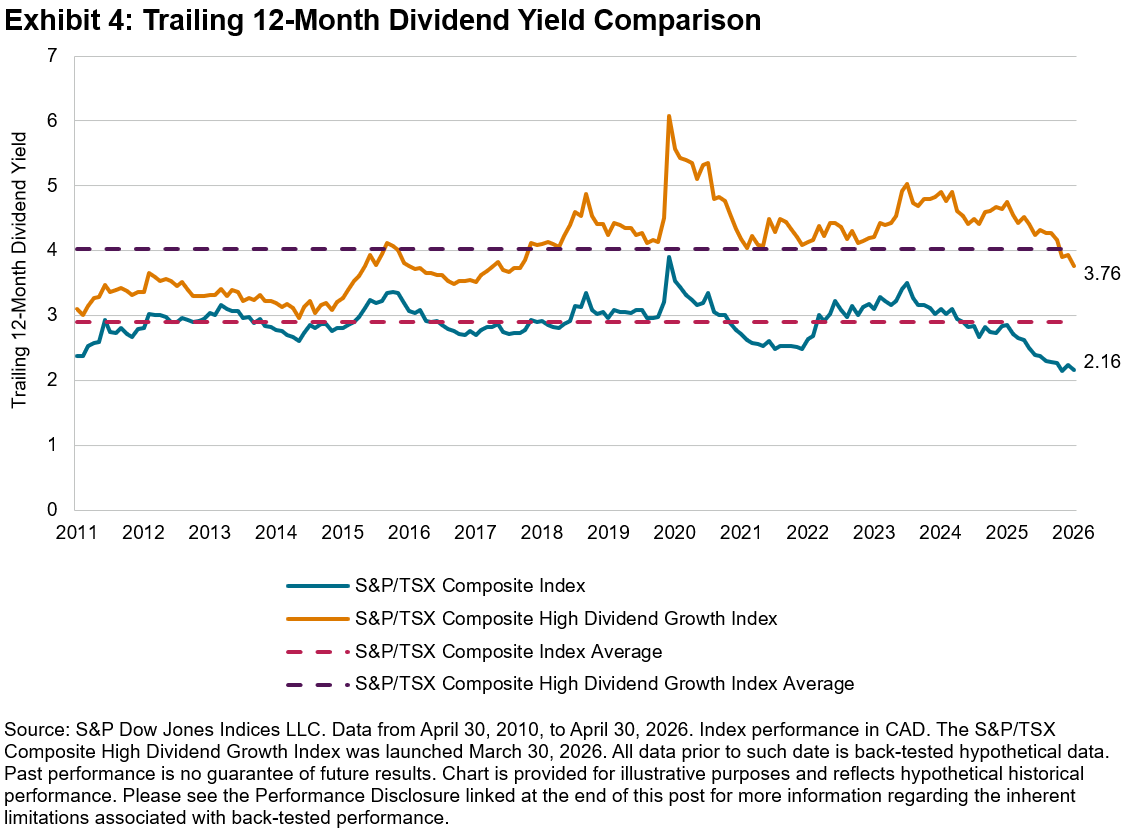

A distinctive feature of the index methodology is its selection of constituents based on forecast dividend yield growth, rather than DPS growth. This important distinction has historically resulted in the index reflecting a combination of both strong current yield and anticipated future dividend growth (see Exhibits 4 and 5).

As of April 30, 2026, the S&P/TSX Composite High Dividend Growth Index had a yield of 3.76%, standing 1.60% above the S&P/TSX Composite Index’s yield of 2.16%. This yield premium exceeds the historical average spread of 1.12% by 38 bps.

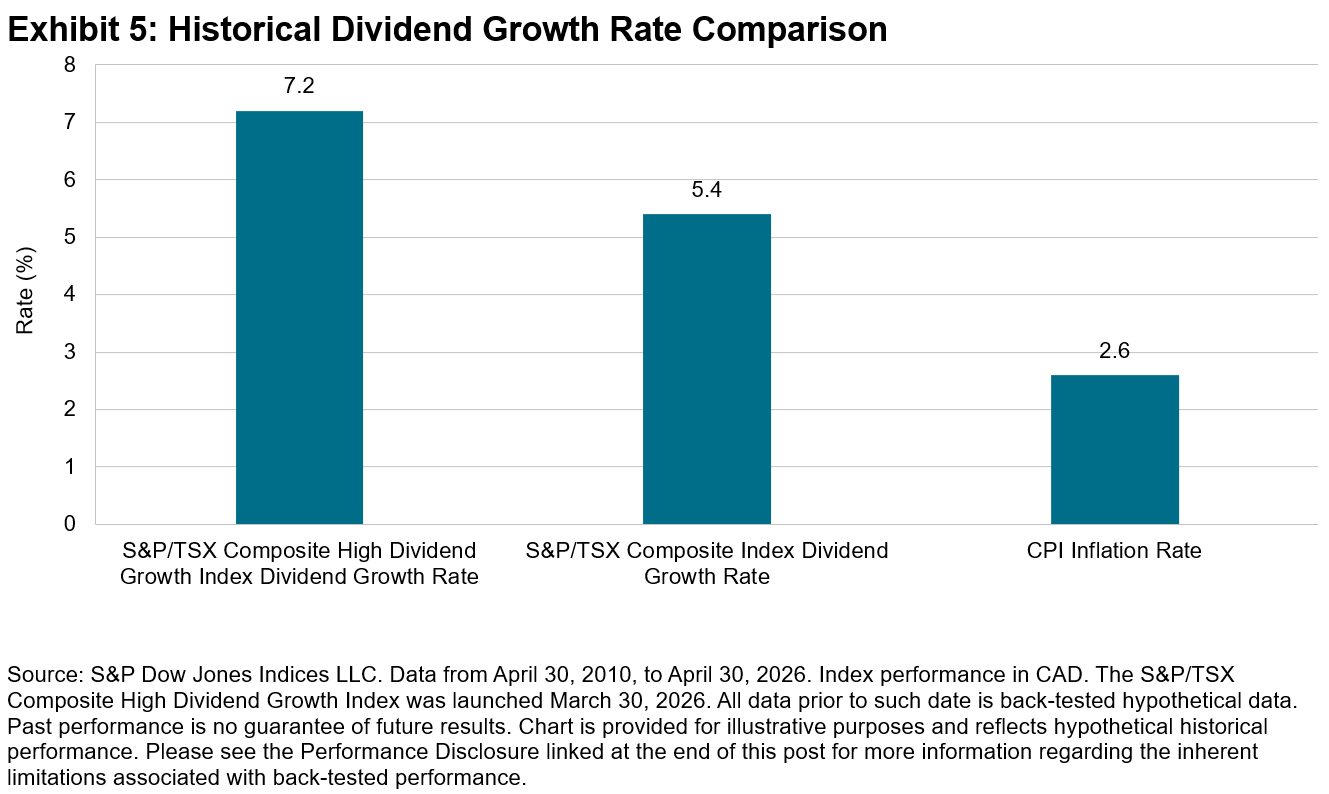

Over the full back-tested period, the S&P/TSX Composite High Dividend Growth Index posted a 7.2% annualized dividend growth rate, outpacing the S&P/TSX Composite Index’s 5.4% and the 2.6% CPI inflation rate. The index showed robust dividend growth well above inflation, which may lead to an increase in purchasing power over time.

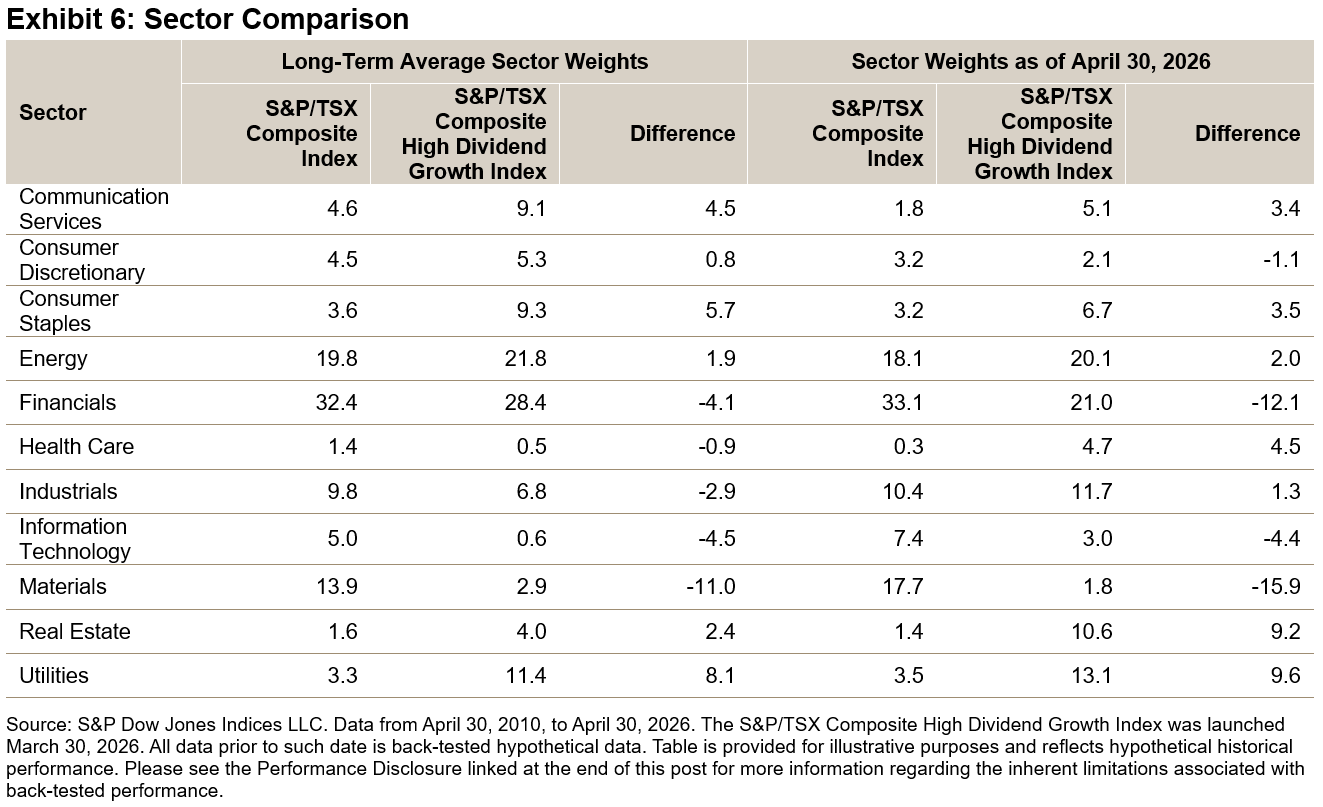

As of April 30, 2026, the S&P/TSX Composite High Dividend Growth Index is significantly overweight the Real Estate and Utilities sectors, while notably underweight in Financials and Materials. This weighting pattern is consistent with the long-term average, although current sector overweights and underweights are more pronounced than those seen over the long term.

Conclusion

S&P DJI is pleased to introduce this innovative methodology to the S&P/TSX Composite Index. With its distinctive approach, the index has shown outperformance and defensive characteristics, as well as higher dividend yield and growth relative to the S&P/TSX Composite Index over the back-tested period. The index serves as a new tool to track companies with a proven record of dividend growth, strong current dividend yields and projected future dividend growth.

1 See the S&P/TSX Canadian Indices Methodology for more information.

The posts on this blog are opinions, not advice. Please read our Disclaimers.SPIVA Special Report: Heroes in Haystacks

Can Hero Funds save portfolios? S&P DJI’s Joe Nelesen takes a closer look at our special SPIVA report examining the performance of multi-asset portfolios of funds versus weighted blends of indices.

The posts on this blog are opinions, not advice. Please read our Disclaimers.