Introduction

As an industry leader in dividend index development, S&P Dow Jones Indices (S&P DJI) is committed to launching new and innovative dividend indices across global markets. The newly launched S&P/TSX Composite High Dividend Growth Index reflects this, representing the first application of the S&P Global Market Intelligence Dividend Forecasting Dataset within the S&P/TSX Composite Index universe. The index employs a distinct methodology, selecting companies that have demonstrated stable or growing dividends over the past five years and are projected to deliver the highest dividend yield growth going forward.

In this blog, we will explore the index’s methodology, historical outperformance, enhanced dividend yield and growth, as well as sector allocations versus the S&P/TSX Composite Index.

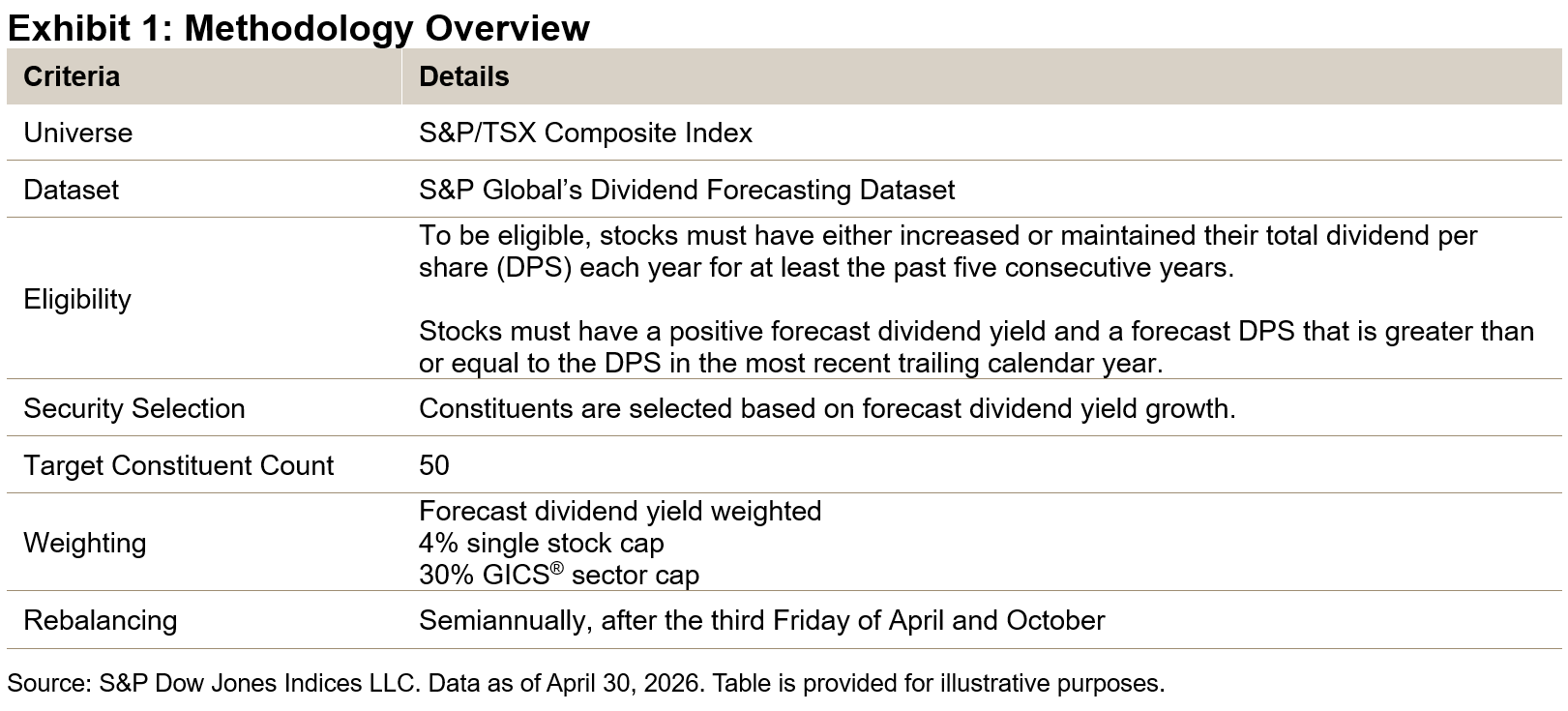

Methodology Overview

To be eligible for selection, constituents must have maintained or grown their dividends for at least five consecutive years, and they must also be projected to continue to do so over the next 12 months.

The index selects the top 50 constituents exhibiting the highest forecast dividend yield growth, determined by subtracting the 12-month historical yield from the 12-month forecast yield. Constituents are then weighted according to their forecast dividend yield, subject to stock and sector constraints.1

Performance Comparison

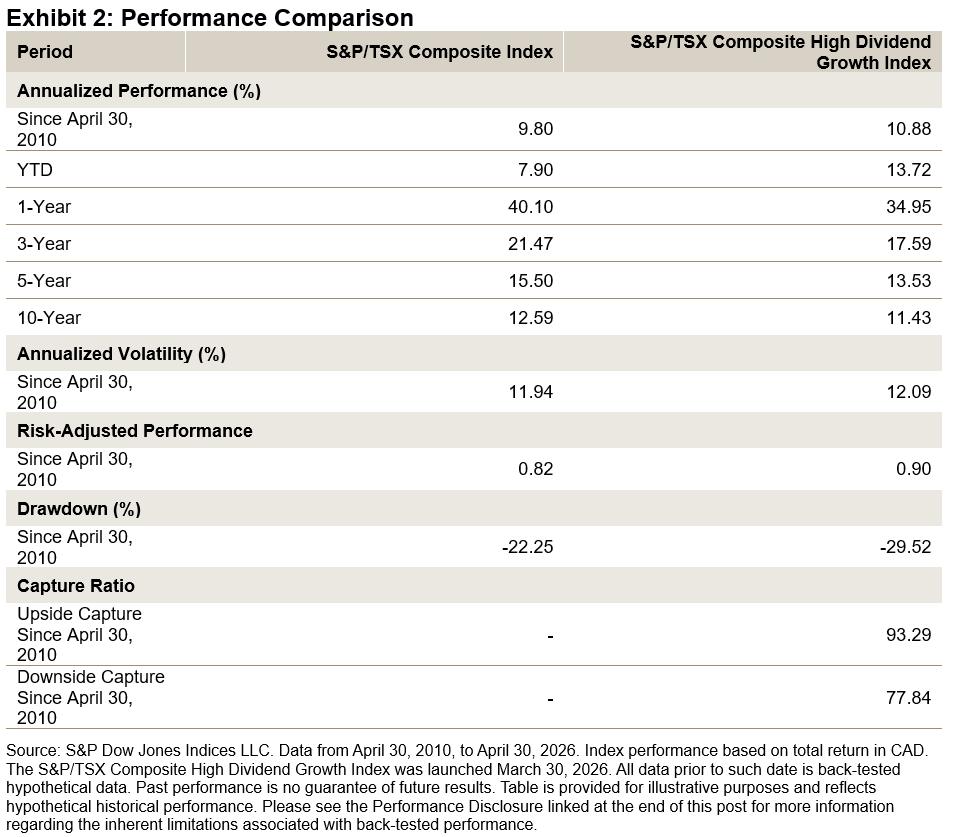

Using back-tested data starting April 2010, the S&P/TSX Composite High Dividend Growth Index outperformed the S&P/TSX Composite Index, both on an absolute and risk-adjusted basis (see Exhibit 2). Additionally, the index has demonstrated asymmetric capture ratios, participating in over 93% of the benchmark’s upside while the downside capture ratio was less than 78%.

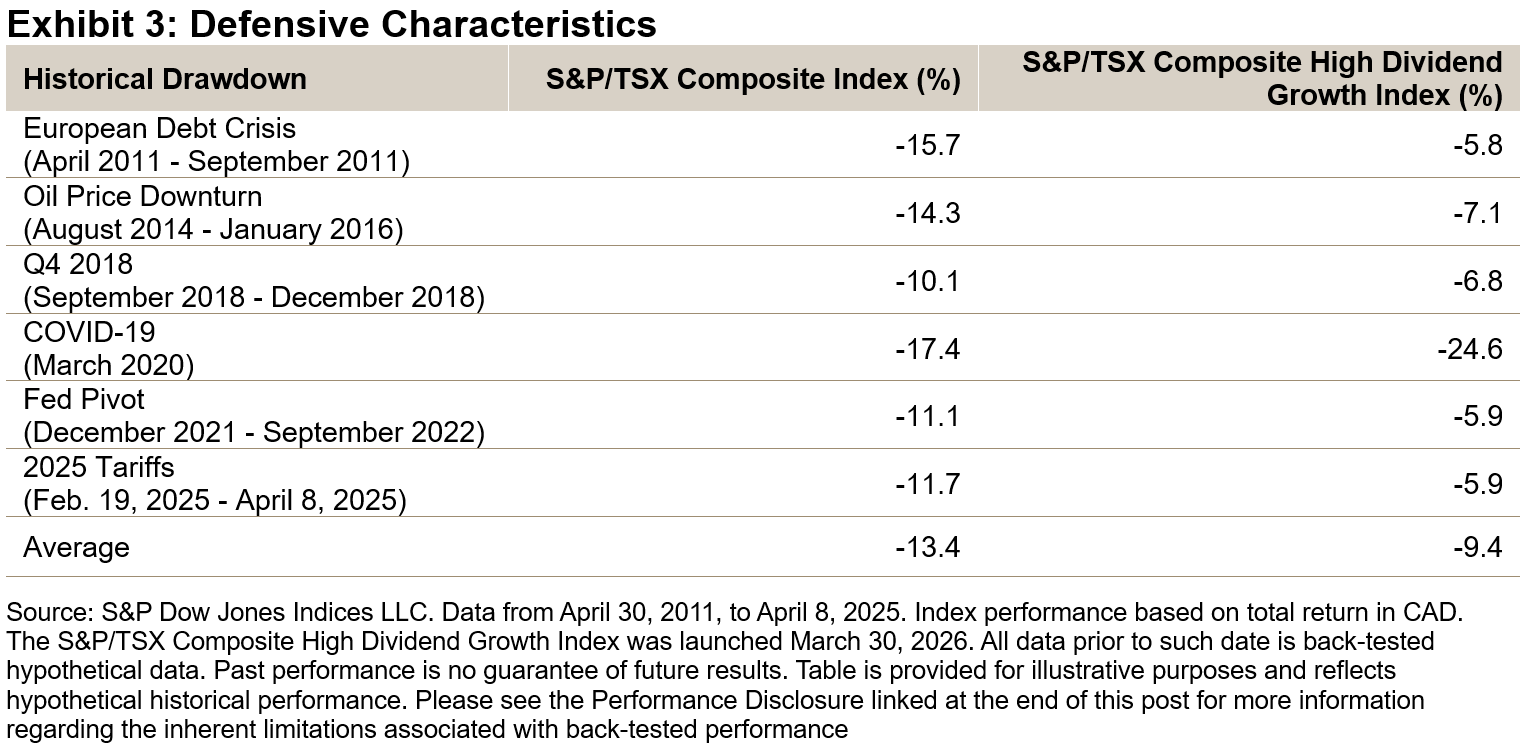

Beyond its strong downside capture, the index has shown notable downside protection during historical drawdown periods over the back-tested period, outperforming the S&P/TSX Composite Index in five out of six major drawdowns, with the exception of the March 2020 COVID-19 downturn. On average, the S&P/TSX Composite High Dividend Growth Index experienced a drawdown of -9.4%, compared to -13.4% for the S&P/TSX Composite Index, equating to less than 70% of the benchmark’s downside.

Dividend Comparison

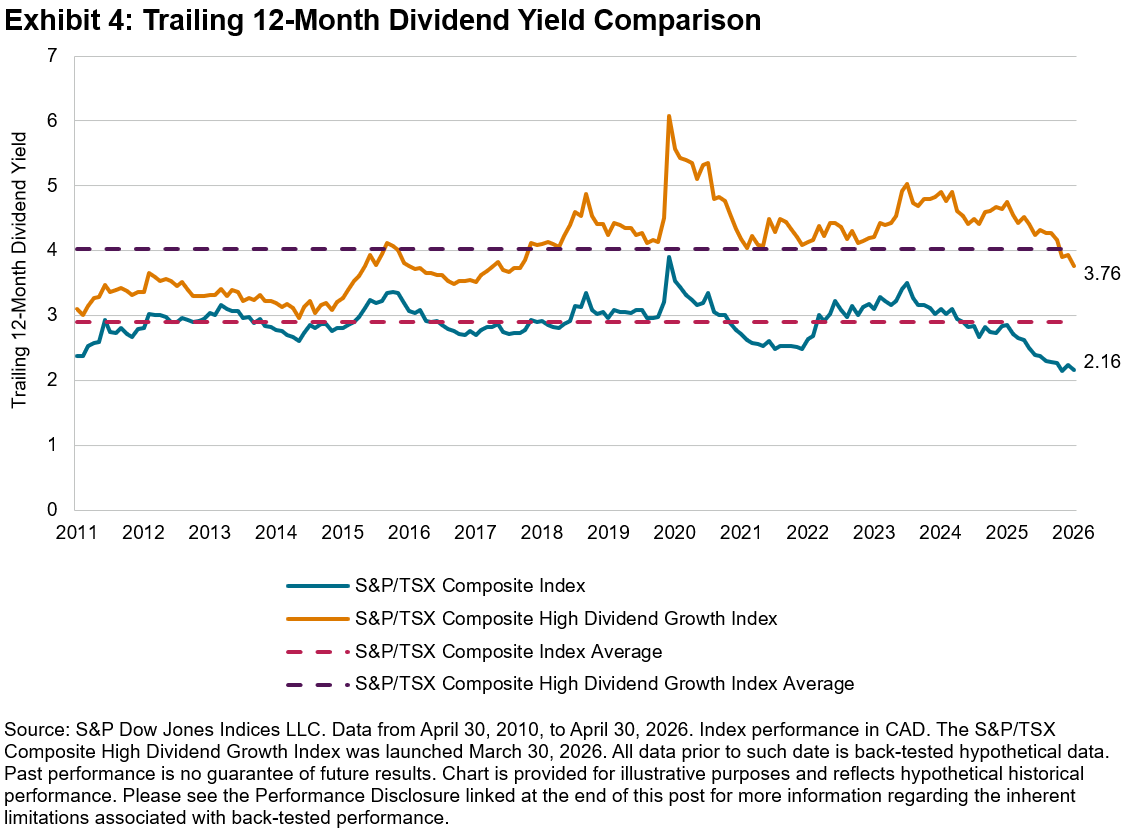

A distinctive feature of the index methodology is its selection of constituents based on forecast dividend yield growth, rather than DPS growth. This important distinction has historically resulted in the index reflecting a combination of both strong current yield and anticipated future dividend growth (see Exhibits 4 and 5).

As of April 30, 2026, the S&P/TSX Composite High Dividend Growth Index had a yield of 3.76%, standing 1.60% above the S&P/TSX Composite Index’s yield of 2.16%. This yield premium exceeds the historical average spread of 1.12% by 38 bps.

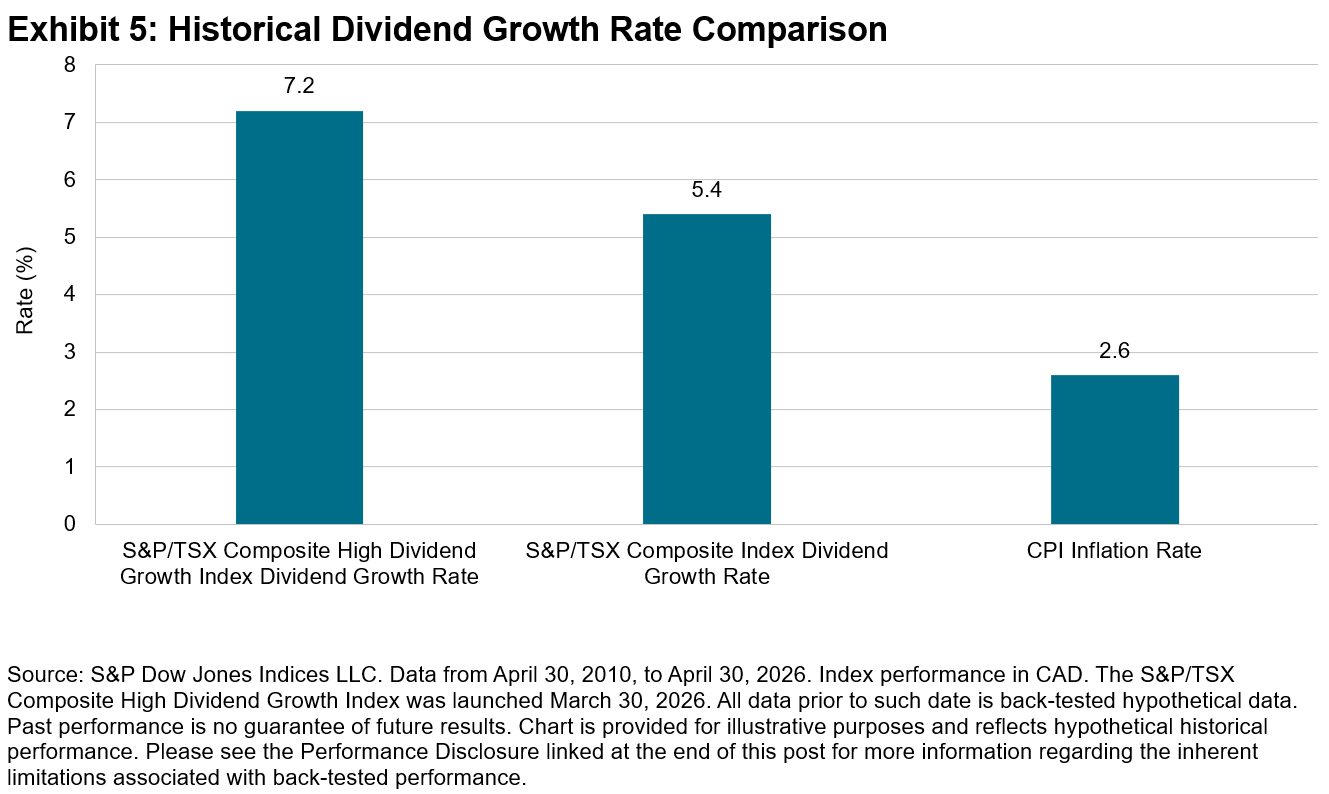

Over the full back-tested period, the S&P/TSX Composite High Dividend Growth Index posted a 7.2% annualized dividend growth rate, outpacing the S&P/TSX Composite Index’s 5.4% and the 2.6% CPI inflation rate. The index showed robust dividend growth well above inflation, which may lead to an increase in purchasing power over time.

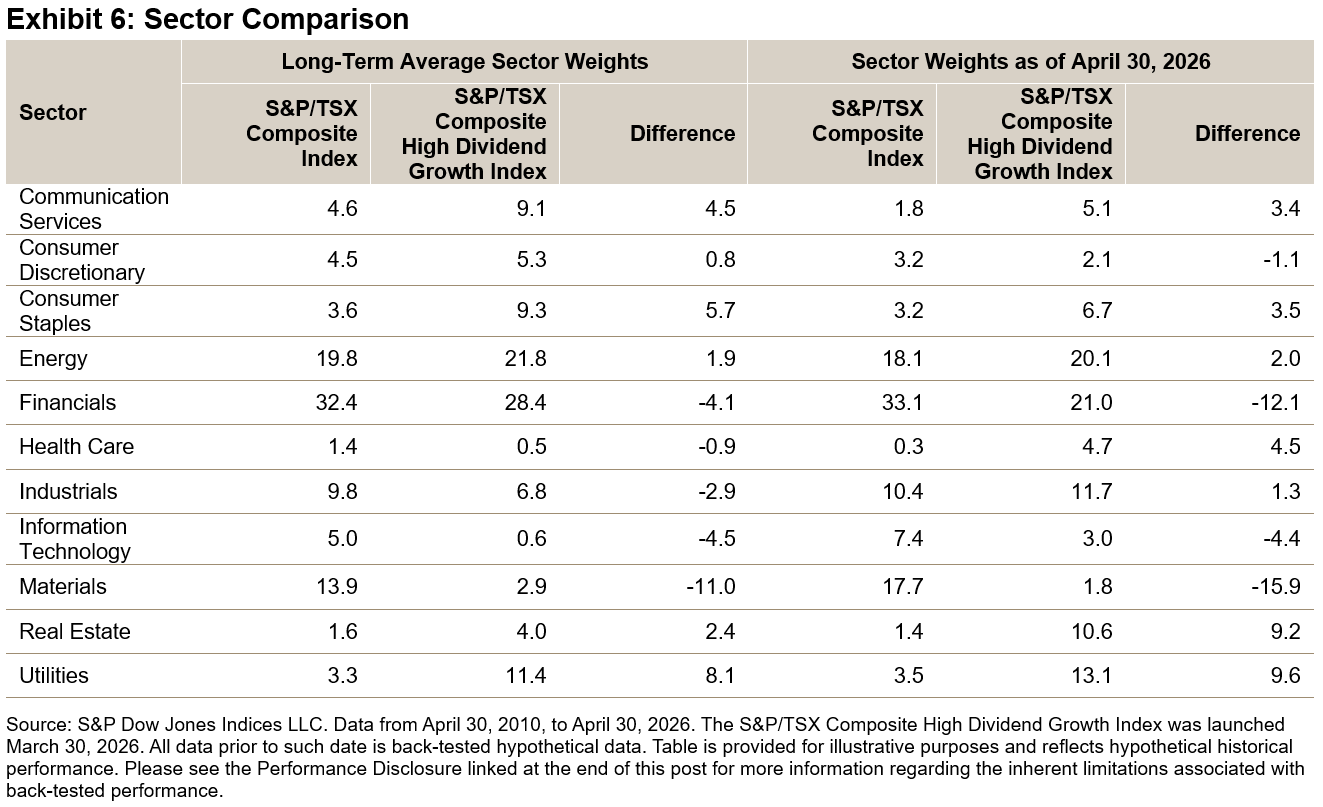

As of April 30, 2026, the S&P/TSX Composite High Dividend Growth Index is significantly overweight the Real Estate and Utilities sectors, while notably underweight in Financials and Materials. This weighting pattern is consistent with the long-term average, although current sector overweights and underweights are more pronounced than those seen over the long term.

Conclusion

S&P DJI is pleased to introduce this innovative methodology to the S&P/TSX Composite Index. With its distinctive approach, the index has shown outperformance and defensive characteristics, as well as higher dividend yield and growth relative to the S&P/TSX Composite Index over the back-tested period. The index serves as a new tool to track companies with a proven record of dividend growth, strong current dividend yields and projected future dividend growth.

1 See the S&P/TSX Canadian Indices Methodology for more information.

The posts on this blog are opinions, not advice. Please read our Disclaimers.