As institutional capital moves deeper into digital assets, one question is becoming increasingly relevant: what, exactly, should crypto fund managers be measured against?

That was the central issue in a recent webinar, “Benchmarking Digital Asset Funds: Are Managers Measuring Performance Effectively?” hosted by Crypto Insights Group with participation from S&P Dow Jones Indices (S&P DJI), Amitis Group and Syncracy Capital. The discussion brought together the perspectives of S&P DJI, an index provider with a range of S&P Digital Asset Indices, an active manager and a fund allocator—offering a useful snapshot of how institutional standards are beginning to form in a market that still lacks a universally accepted playbook.

The panel featured Andy Martinez, CFA, CEO of Crypto Insights Group; Sherifa Issifu of S&P Dow Jones Indices; Ryan Watkins, CIO of Syncracy Capital; and Chris Solarz, CIO of Amitis Group. Together, they explored three issues that increasingly define institutional crypto investing: what should be benchmarked, how should alpha be defined, and what makes a benchmark credible in a fast-evolving asset class?

The Core Problem: Finding a Benchmark Fit for the Fund Strategy

Our host Andy Martinez opened the session with a practical observation from Crypto Insights Group’s work with both managers and allocators: benchmarking is one of the most persistent friction points in digital asset investing. More than 60% of managers surveyed by the firm said their biggest challenge was simply finding a benchmark that fit their mandate, while the next biggest challenge was getting limited partners (LPs) comfortable with the benchmark they had selected.

That challenge matters because benchmarking is not a cosmetic exercise. It shapes how managers present performance, how allocators judge skill and ultimately how capital gets allocated. In traditional markets, exposure and comparison sets are relatively well understood. In digital assets, by contrast, many strategies are still being compared against benchmarks that do not reflect the exposures they actually contain.

A recurring example is the industry’s anchoring performance back to Bitcoin (a proxy is the S&P Bitcoin Index), even when a strategy has little or no Bitcoin exposure, or in some cases the use of an equity benchmark like the S&P 500®. As Martinez noted, this creates a distorted evaluation framework—particularly now that institutions can access Bitcoin beta cheaply through ETFs. If the benchmark does not reflect the real opportunity set, it becomes difficult to tell whether returns came from market exposure, manager skill or simply the framing of the comparison.

Why Bitcoin Is No Longer a Sufficient Universal Benchmark

Ryan Watkins made perhaps the clearest case for moving beyond a one-size-fits-all Bitcoin benchmark. Syncracy Capital runs a long-biased digital asset hedge fund focused on the top end of the crypto market excluding Bitcoin, with an emphasis on identifying long-term category leaders across different segments of the crypto economy.

Watkins argued that benchmarking such a strategy to Bitcoin is fundamentally misleading. His analogy was straightforward: it is like benchmarking an equities hedge fund against gold. In his view, Bitcoin behaves more like a monetary asset or digital gold, while much of the rest of the digital asset universe increasingly resembles equity-like exposure to application layers, protocols and growth themes.

That distinction matters because relative performance can become deeply distorted. In years when Bitcoin rallies sharply, managers focused on altcoins or broader digital asset themes may appear to underperform even if they are executing well within their mandate. In other periods, the reverse may happen, creating the illusion of skill where none exists.

Watkins also emphasized that the very term “cryptocurrency” obscures the diversity of the market. Most tokens are not designed to function primarily as currencies. Instead, allocators are increasingly underwriting exposure to areas such as stablecoins, prediction markets, tokenization and other application-specific segments of the crypto economy. That broadening opportunity set makes a single-asset benchmark even less defensible as the default reference point.

To better align measurement with mandate, Watkins said Syncracy Capital uses an S&P DJI benchmark—the S&P Cryptocurrency BDA Ex-MegaCap Index—that excludes the mega caps, specifically Bitcoin and Ethereum, as a more representative proxy for the part of the market in which the fund actually invests.

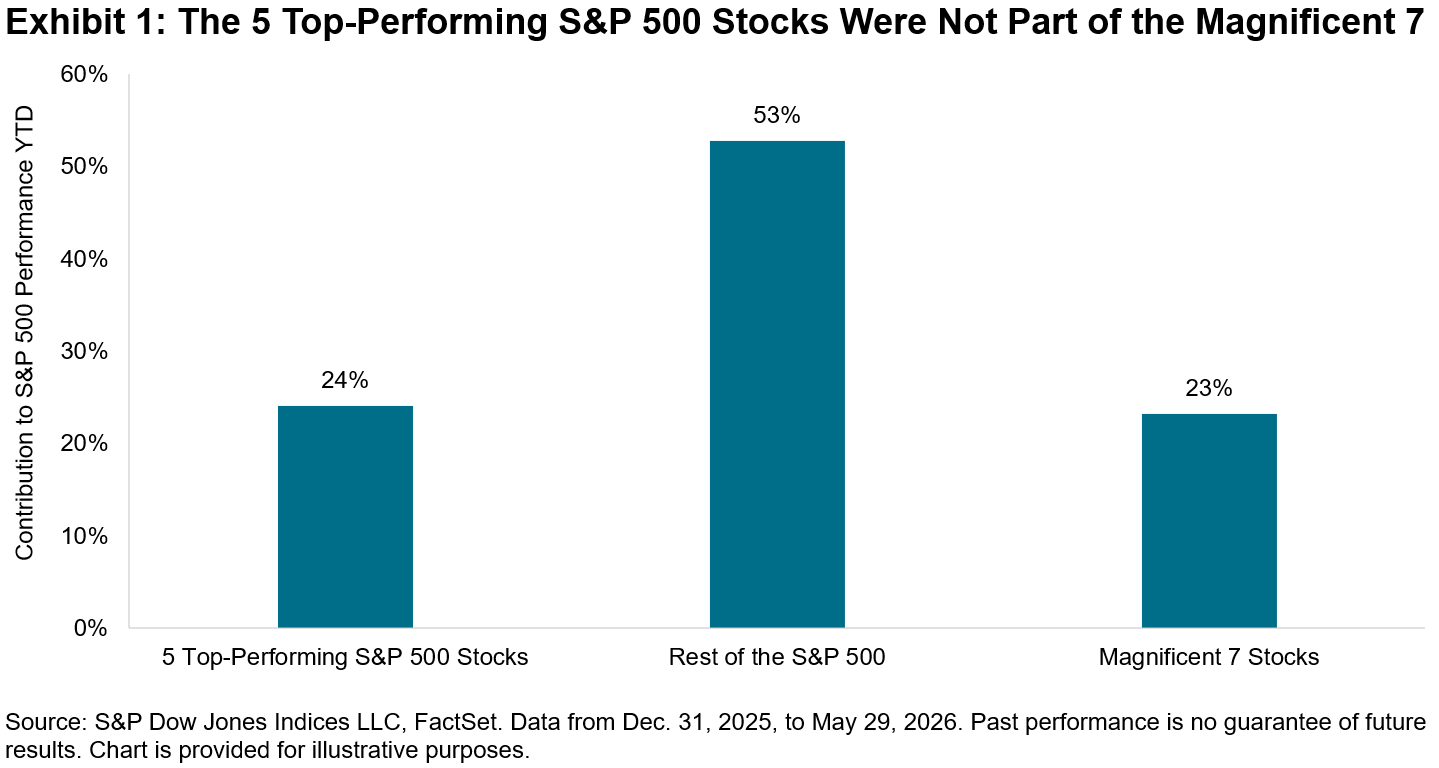

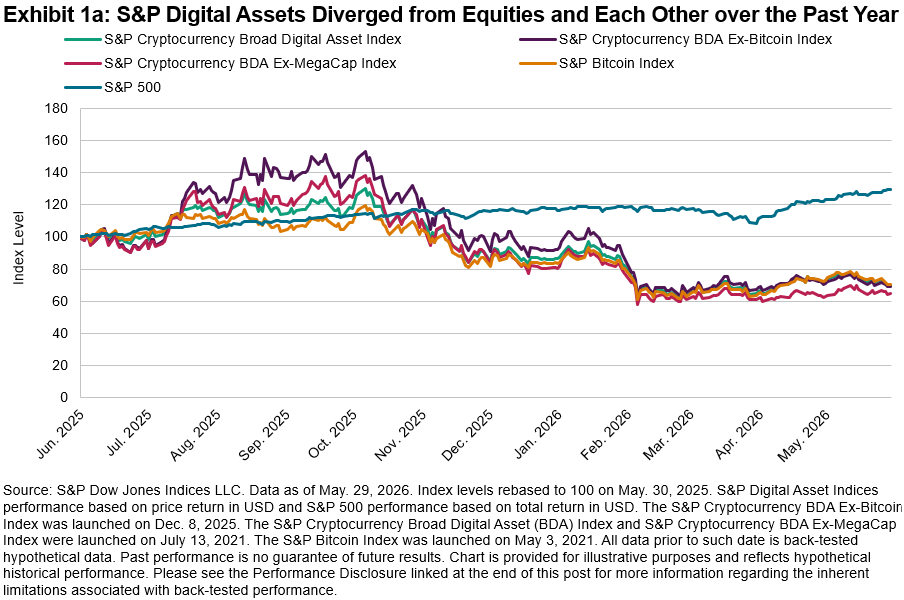

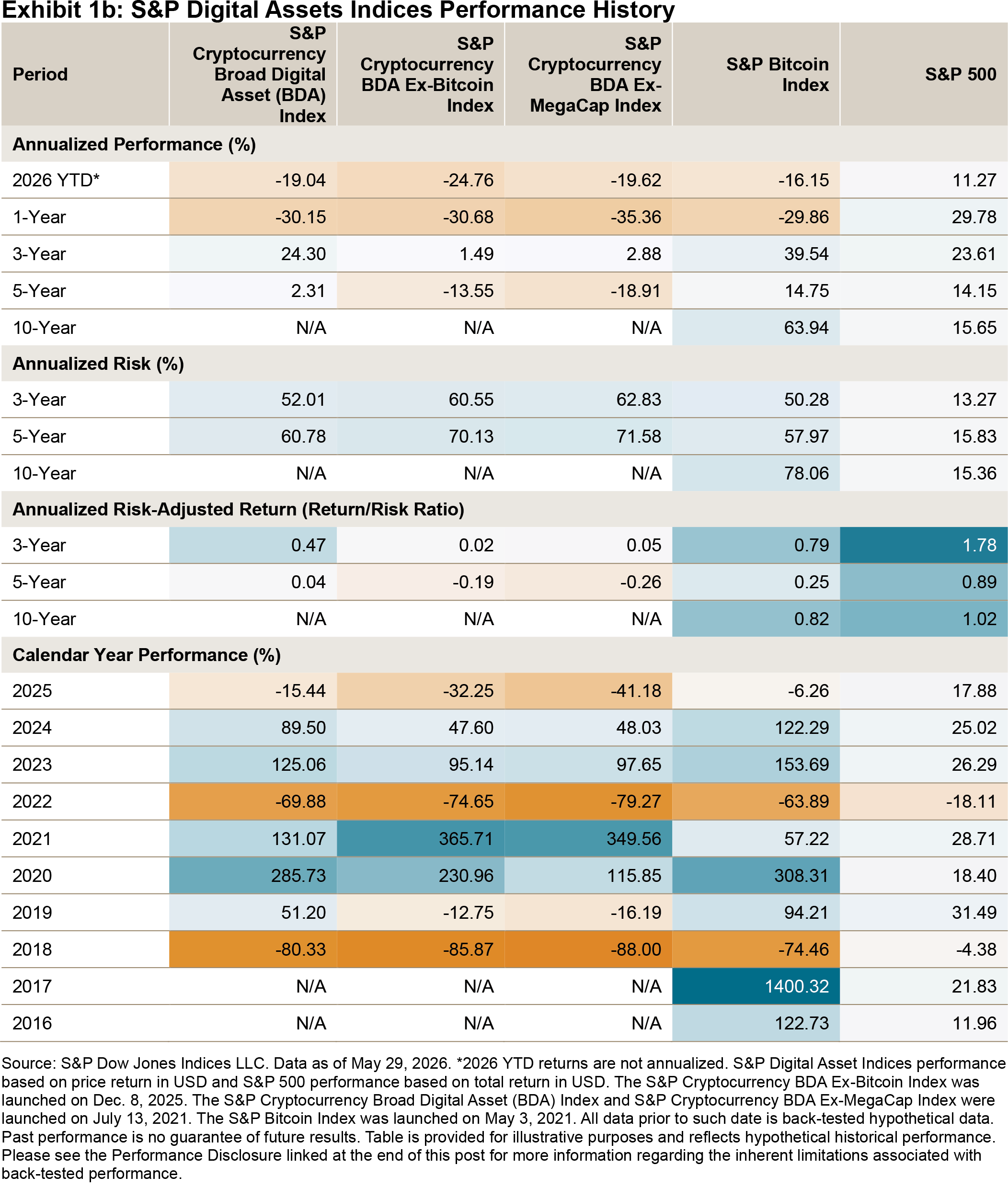

In Exhibit 1, we show the performance of the S&P Cryptocurrency Broad Digital Asset (BDA) Index versus the S&P Cryptocurrency BDA Ex-MegaCap Index. The past year has highlighted the stark difference in behavior and performance characteristics between the S&P 500 and cryptocurrency indices, across indices that both include and exclude Bitcoin. 2025 and 2026 have highlighted the importance of looking under the hood of digital asset indices.

Learn more about our capabilities and view the full webinar replay.

The posts on this blog are opinions, not advice. Please read our Disclaimers.