As financial advisors increasingly use index-based strategies to help scale their practices, many are turning to index providers not only for benchmarks—but also for insights. A recent whitepaper1 from Cerulli Associates analyzes why and how a segment of advisors, known as “index provider content users,” are actively using these insights to inform their decision-making and client interactions.

Why and How Advisors Use Index Provider Content

According to Cerulli, 37% of financial advisors report using index providers’ information, with independent registered investment advisors (RIAs) being the type of advisor most likely (44%) to use these inputs.2

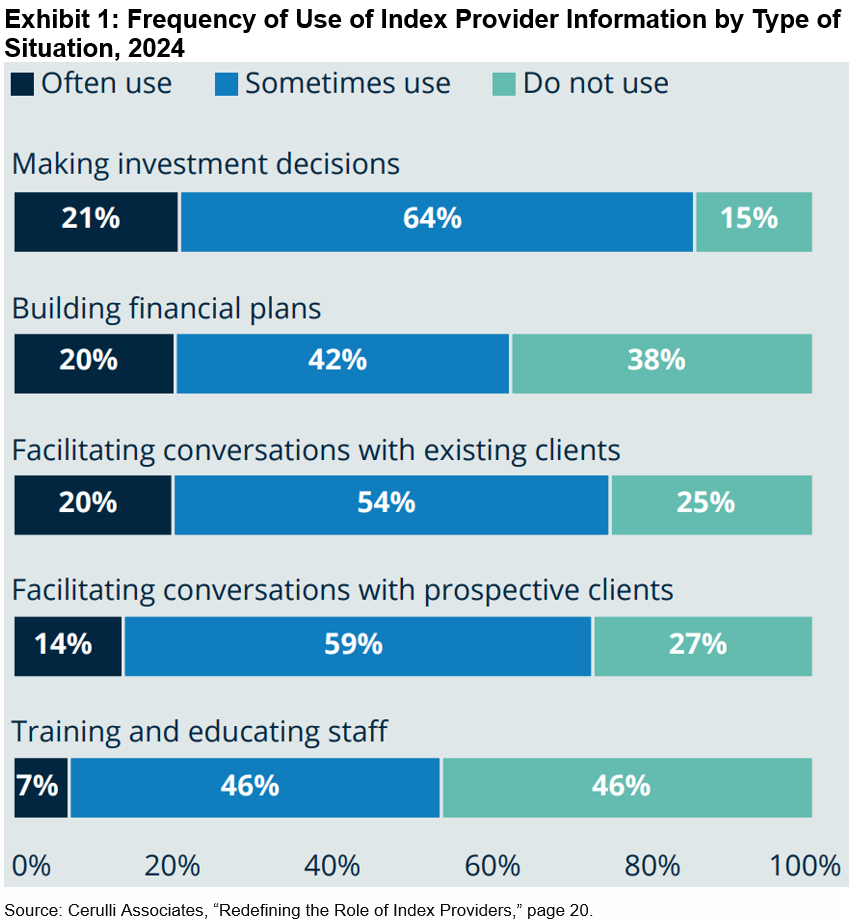

Advisors are using data, thought leadership and methodology documentation as they carry out a range of advisory functions. As shown in Exhibit 1, the most common use cases are to make investment decisions (85%) and facilitate conversations with clients (74%) and prospects (73%). Some advisors are also using content as they build financial plans (62%) and train and educate their staff (53%).2 As an independent RIA interviewed by Cerulli noted, “I rely on the S&P Persistence Scorecards and an index scorecard. I am informed by some of that data.”2

These practices illustrate how index providers can potentially play a broader role in educating wealth managers by offering resources that help advisors articulate the potential value of index-based strategies to their clientele.

Commonly Used Index-Based Product Information

Cerulli finds that advisors prefer a range of content formats, depending on the context. For longer-form education and training, advisors tend to gravitate toward in-person meetings, whitepapers and webinars delivered on a quarterly or annual basis. Advisors are more likely to read emails, newsletters and blogs on at least a monthly basis.

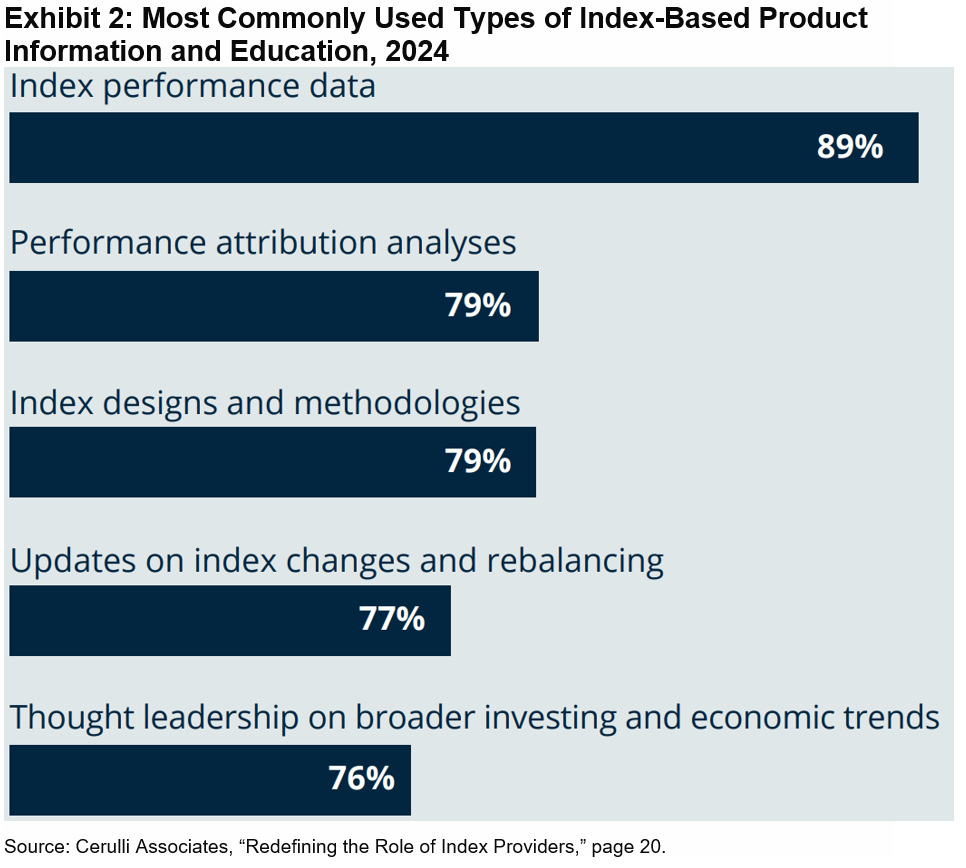

As shown in Exhibit 2, the most commonly used types of index-based product information and education by these advisors are index performance data (89%), performance attribution analyses (79%) and documentation on index designs and methodologies (79%). Advisors also report using updates related to index changes and rebalancing (77%), as well as thought leadership on broader investing and economic trends (76%).2

Turning Insights into Differentiation

The survey results and interviews with advisors suggest that index providers can play a valuable role in expanding the index education content ecosystem by providing an independent and differentiated perspective. “It might be helpful to hear from [index providers] because asset managers are incentivized to push products and are not always the best purveyors of information,” one wirehouse advisor said.3

By offering accessible, client-facing materials that explain index design, methodology and performance, index providers deliver content that may inform advisors’ conversations with clients and prospects alike. As more advisors seek to explain how and why index-based strategies work, the ability to tap into credible, easy-to-use materials may become a key differentiator in growing their practices.

To learn more about how financial advisors are using index provider resources and related implications, explore the full Cerulli whitepaper, “Redefining the Role of Index Providers.”

1 The Cerulli Associates whitepaper “Redefining the Role of Index Providers” was sponsored by S&P Dow Jones Indices.

2 Please see page 20 of Cerulli Associates’ “Redefining the Role of Index Providers.”

3 Please see page 15 of Cerulli Associates’ “Redefining the Role of Index Providers.”

The posts on this blog are opinions, not advice. Please read our Disclaimers.