The S&P/ASX 200 High Dividend Index measures a selection of high-dividend-yielding stocks, while the S&P/ASX 200 GARP Index (GARP standing for growth at a reasonable price) measures the performance of the top growth stocks with high quality and value composite scores selected from the respective underlying index universe. In this blog, we will explore how integrating these two index strategies potentially results in enhanced long-term risk-adjusted index performance based on hypothetical back-tested data.

Understanding the Indices

The S&P/ASX 200 High Dividend Index tracks the performance of 50 high-dividend-yielding companies from the S&P/ASX 200, after screening out A-REITS and low momentum stocks.1 Across back-tested time horizons, the S&P/ASX 200 High Dividend Index demonstrated a higher theoretical dividend yield and better total return performance than the S&P/ASX 200. Based on back-tested data, for the period July 31, 2011, to Aug. 31, 2025, the index would have had an average trailing 12-month dividend yield of 5.6% and an annual excess return of 1.91% when compared with the S&P/ASX 200.

On the other hand, the S&P/ASX 200 GARP Index could help to identify growth companies while considering valuation and quality. It starts with 150 stocks with high growth scores, then selects 50 stocks with the highest quality and value composite scores.2 Across back-tested time horizons, the S&P/ASX 200 GARP Index exhibited an ability to reflect growth opportunities. For the period from July 31, 2011, to Aug. 31, 2025, the S&P/ASX 200 GARP Index would have outperformed the S&P/ASX 200 by 2.05% per year.

Combination Results

While high-dividend index strategies are often concentrated in the Financials sector, the S&P/ASX 200 GARP Index tends to underweight Financials.3 As of Aug. 31, 2025, the Financials sector accounted for 43.6% and 6.6% of the S&P/ASX 200 High Dividend Index and S&P/ASX 200 GARP Index, respectively. Given these weights, the hypothetical combination of GARP and dividend index strategies would potentially complement sector weighting, demonstrate lower tracking error to the S&P/ASX 200 benchmark and ultimately improve risk-adjusted performance, all based on back-tested data.

We combined the two indices at various proportions moving from 100% in the S&P/ASX 200 High Dividend Index to 100% in the S&P/ASX 200 GARP Index by 10% increments, which resulted in 11 hypothetical combinations as illustrated in Exhibit 1. All hypothetical combinations are rebalanced semiannually. For the period July 31, 2011, to Aug. 31, 2025, a hypothetical composition of 50% in the S&P/ASX 200 GARP Index and 50% in the S&P/ASX High Dividend Index generated a higher total return at a lower volatility compared with either standalone index.

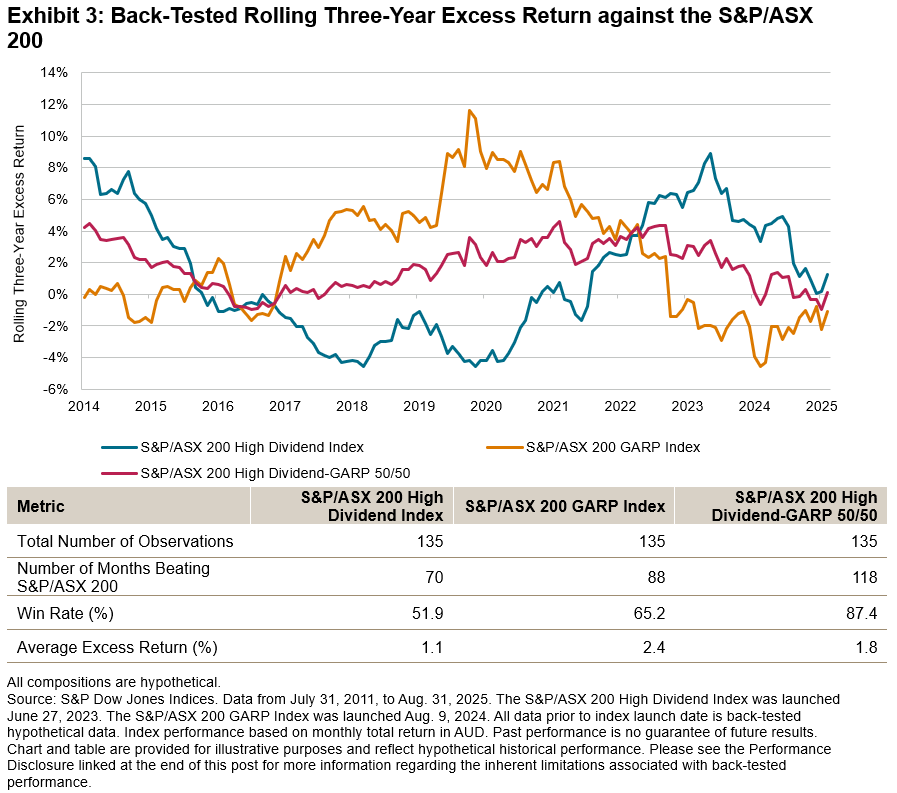

Comparing with the Regional Core Benchmark: S&P/ASX 200

Exhibit 2 shows the risk/performance profiles of the S&P/ASX 200, S&P/ASX 200 High Dividend Index, S&P/ASX 200 GARP Index and the 50/50 hypothetical composition. Across the back-tested time horizon from July 31, 2011, to Aug. 31, 2025, the 50/50 combination posted a higher annualized total return of 11.7% at a lower volatility of 12.82%, resulting in a better risk-adjusted return of 0.91. It outperformed the S&P/ASX 200 by 2.07% per year.

Exhibit 3 illustrates the rolling three-year back-tested performance of the S&P/ASX 200 High Dividend Index, S&P/ASX 200 GARP Index and a 50/50 hypothetical combination of the two indices. From the 135 samples observed from July 2011 to August 2025, the S&P/ASX 200 High Dividend Index and S&P/ASX 200 GARP Index would have outperformed the S&P/ASX 200 52% and 65% of the time, respectively. The outperformance rate was even higher after combining the indices. The 50/50 hypothetical composition outperformed the S&P/ASX 200 in 87% of the samples observed, with an average excess return of 1.8%. An outperformance rate of nearly 90% underscores the performance resilience of the 50/50 combination across various market conditions.

Thanks to diversification, a hypothetical 50/50 combination had a significantly lower tracking error against the S&P/ASX 200 than each component index. Exhibit 4 shows the rolling three-year tracking error. From July 31, 2011, to Aug. 31, 2025, the average tracking error of the 50/50 combination would have been 3.4%, which was lower than the 6.0% of the S&P/ASX 200 High Dividend Index and the 4.3% of the S&P/ASX 200 GARP Index.

![]()

In conclusion, the hypothetical combination of the S&P/ASX 200 High Dividend Index and the S&P/ASX 200 GARP resulted in a composition with a relatively low tracking error to its benchmark but better historical performance than the S&P/ASX 200, historically. This demonstrates the potential for factor index applications in the Australian market.

1 For index methodology, please refer to: https://www.spglobal.com/spdji/en/methodology/article/sp-high-dividend-indices-methodology/

2 For index methodology, please refer to: https://www.spglobal.com/spdji/en/methodology/article/sp-garp-indices-methodology/

3 Jason Ye (August 2025). Introducing the S&P/ASX 200 GARP Index

The posts on this blog are opinions, not advice. Please read our Disclaimers.