We’ve all heard it often—that volatility is a “feature” of Bitcoin and, by extension, the cryptocurrency market in general.

While not all of us would agree with calling it a feature, most would agree that there is a significant amount of volatility in the cryptocurrency market. And, depending on your role—trader, asset manager, advisor, observer—you may either want to capitalize on that volatility or try to reduce it.

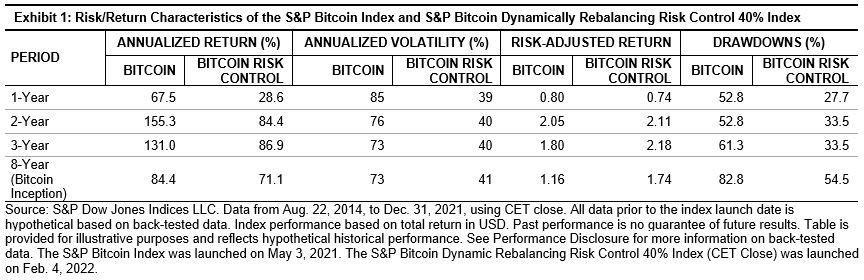

The initial S&P Cryptocurrency Indices, as reported in our whitepaper and based on back-tested data, experienced high annualized returns for the period studied (see Exhibit 1), accompanied by significant volatility and downside risk. If we look at the S&P Bitcoin Index specifically, we can see the annualized back-tested returns are characterized by high volatility.

Using the S&P 500® as a point of comparison, over the three-year period ending Dec. 31, 2021, the annualized return was 26%, annualized risk-adjusted return was 1.5, and annualized volatility was 17.4%.

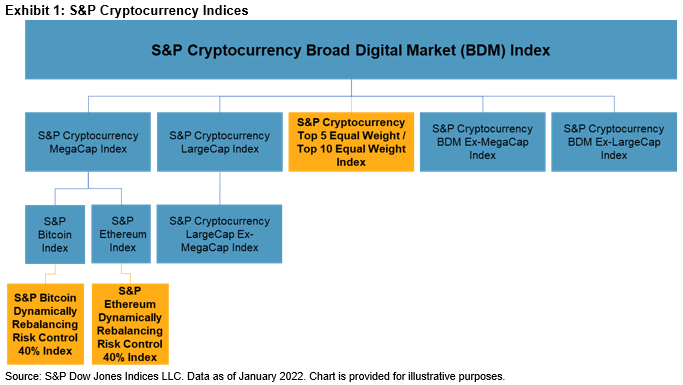

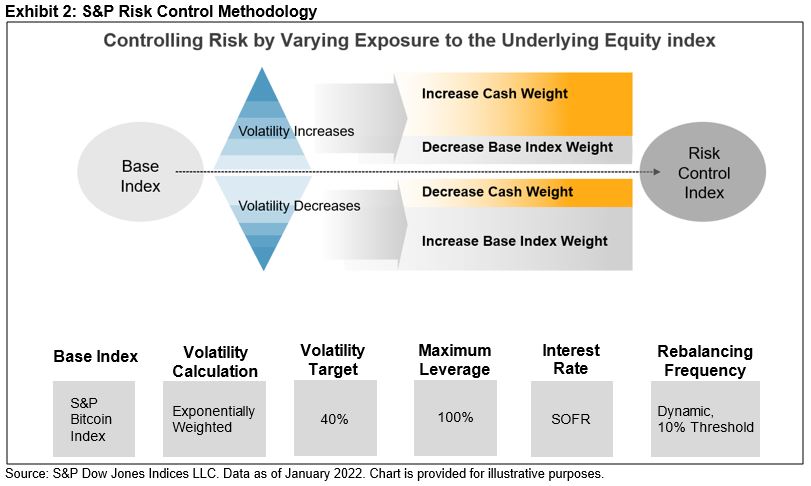

For those looking to mitigate volatility in the cryptocurrency market, we are excited to provide a new potential index solution: the S&P Cryptocurrency Dynamic Rebalancing Risk Control 40% Indices. These indices are designed to measure a more controlled volatility and potentially smoother index returns. Risk control indices are now available for Bitcoin and Ethereum (S&P Risk Control Indices are also available for traditional asset classes—equities, commodities, and more). Exhibit 2 illustrates conceptually how risk control indices work.

For cryptocurrencies, these new indices seek to limit the volatility of the underlying S&P Cryptocurrency Indices to a target level of 40% by adjusting the exposure to the underlying index and allocating to U.S. dollars. The index is rebalanced on a dynamic basis; that is, when the 10% threshold based on exposure is crossed.

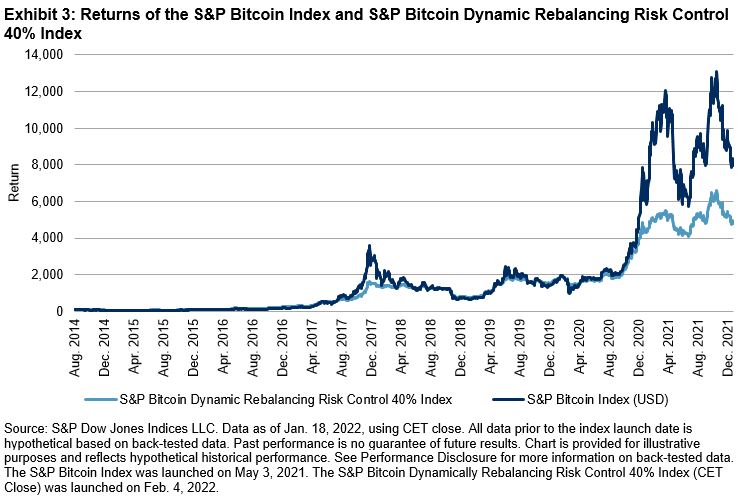

This sounds complicated, so it’s best to show the data. Exhibit 1 displays characteristics of the Bitcoin risk control index, while Exhibit 3 illustrates the performance. One can see that, while the annualized return was lower for the risk control index, the annualized volatility and drawdowns were significantly reduced. The average number of rebalances triggered per year in the back-test was 12, and the average turnover at rebalance was 13.7%. Notably, risk-adjusted return over time exceeded that of the underlying S&P Bitcoin Index.

For additional details, please refer to S&P Risk Control Indices Methodology & Parameters for current parameters and to the S&P Risk Control Indices section of the S&P DJI Index Mathematics Methodology.

For S&P DJI, this is another innovative way to bring tools and transparency to this emerging asset class.

Stay tuned for additional crypto indices launching soon!

The posts on this blog are opinions, not advice. Please read our Disclaimers.