S&P Dow Jones Indices recently published its fifth annual analysis of exchange-traded fund (ETF) usage by U.S. insurers in their general accounts. Regulatory filing data, which details the individual securities that insurers hold, showed that in 2019, ETF AUM in insurance general accounts grew to USD 31 billion—a 16% increase over 2018. While this headline figure shows the continued growth of ETFs in insurers’ portfolios, the trends that underlie this data are perhaps more interesting.

Insurers Sold ETFs That Weren’t Equity or Fixed Income

The number of ETF shares insurers held declined in 2019 to 398 million from 400 million in 2018, indicating that while AUM grew, insurers were net sellers of ETFs in 2019. If we break down the data in terms of asset class, however, we see that insurers bought equity and fixed income ETFs and sold ETFs classified as “other,” a category that includes currency, commodity, multi-asset, etc. Insurers’ holdings of non-equity and non-fixed income ETFs saw a 38% year-over-year decrease in AUM and a 45% decrease in shares. Exhibit 1 shows how each asset class contributed to the change in insurers’ ETF shares from 2018 to 2019.

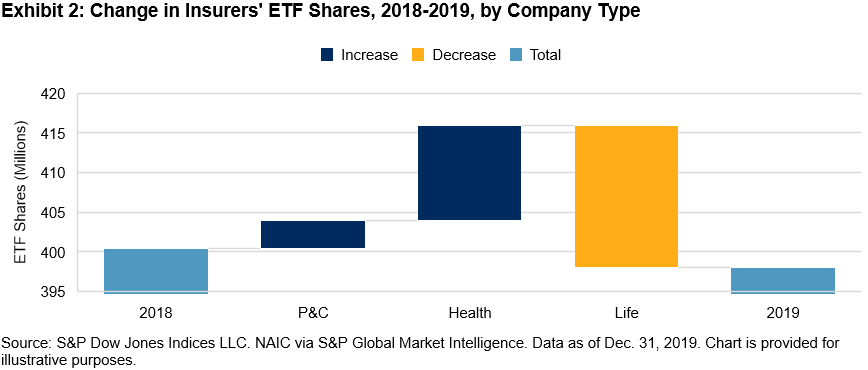

Life Insurers, in Particular, Sold ETFs

If we look at what drove the decline in insurers’ ETF shares now in terms of company type versus asset class, we see that while Property and Casualty (P&C) and Health companies were net buyers of ETFs in 2019, Life companies were net sellers (see Exhibit 2).

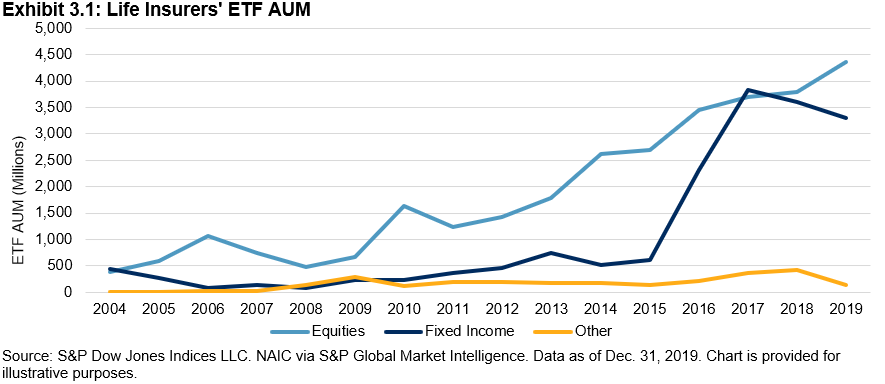

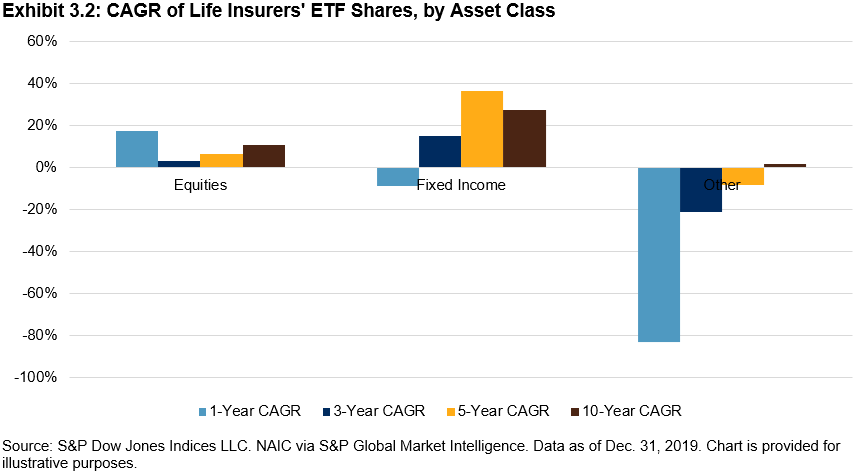

Life insurers sold fixed income ETFs last year, a reversal in the significant buying that took place between 2015 and 2017 (see Exhibits 3.1 and 3.2).

Most of Insurers’ Fixed Income ETF AUM Was in IG, but High Yield (HY) Gained Traction

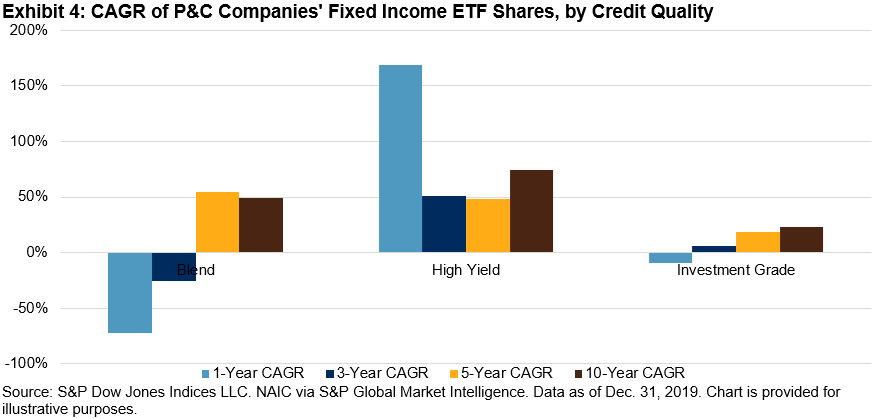

Fixed income ETF usage within insurance general accounts overall, however, continues to grow, with AUM up 13% year-over-year and shares up 11% year-over-year. While nearly 80% of insurers’ fixed income ETF AUM was in investment-grade bond ETFs, HY bond ETFs are gaining traction, particularly with P&C insurers, which increased their buying of HY bond ETFs by 169% in 2019 (see Exhibit 4).

HY bond ETFs comprised 38% of P&C insurers’ fixed income ETF holdings—more than four times the percentage of the broader insurance market’s HY bond ETF holdings.

We offer these insights with the caveat that much has changed this year in the financial markets, and as a result, insurers’ ETF holdings may look quite different today than they did at the end of 2019. We’ll be taking a closer look at the quarterly data and publishing a companion to this report to better understand how COVID-19 may have affected insurers’ holdings.

The posts on this blog are opinions, not advice. Please read our Disclaimers.