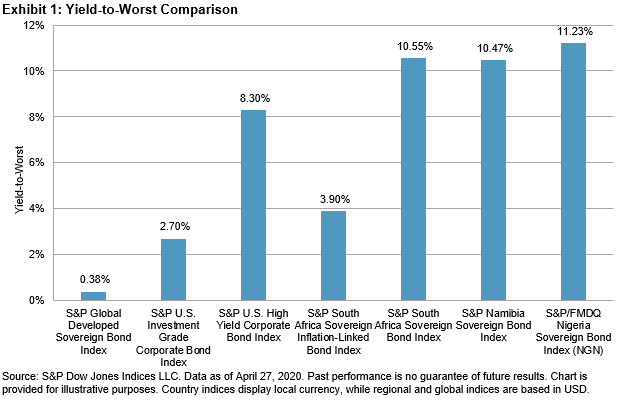

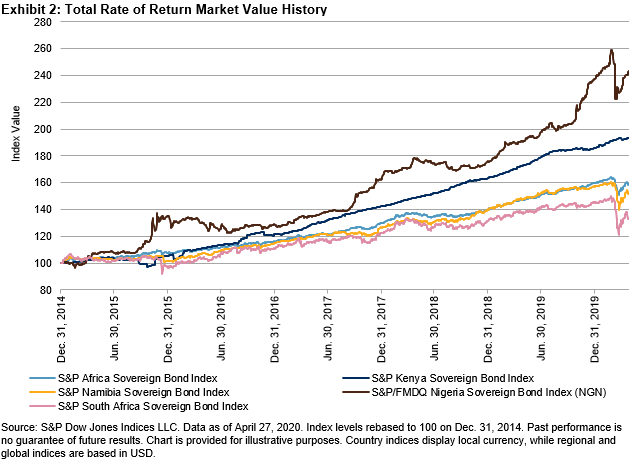

The exchanged-traded fund (ETF) structure has led to increased investment options within fixed income, and the African markets are a clear example of this. Over the past few years, several African ETFs have been introduced to the market, tracking indices provided by S&P Dow Jones Indices in South Africa, Nigeria, and Namibia, giving investors options to participate in this investment space. With transparent indices and tight-knit local ties, S&P Dow Jones Indices and ETF providers have opened asset classes that historically were only accessible to large and more sophisticated investors. Market segments such as high yield, emerging markets, and international markets, which were inaccessible just a few years ago, have become an investment opportunity for all market participants. In addition to accessibility, the yields of African sovereign bonds have tended to be higher than both investment-grade and high-yield corporate bonds in the U.S.

The ETF structure has been around since the early 1990s and has become a popular approach to investing for both equity and debt investments. ETFs are no longer considered a niche product and a growing number of organizations utilize this investment vehicle. The ETF structure has made it easier and cheaper to own and trade big groups of securities at once, on demand. Investors can diversify their exposure by buying entire baskets of securities without buying and selling the underlying individual securities. Because of these efficiencies and benefits, ETFs are being used by investors and traders around the globe.

The popularity of ETFs can be understood by the benefits provided across asset classes. ETFs provide transparency and efficiency as an exchange-traded product that is priced continuously intraday. This makes it easy for an investor to discover the value, gain diversification, and trade in a tactical way. The ETF structure also provides low transaction fees, leading to low management costs, and it can also present tax efficiencies. Recent volatile times have provided a test to ETFs not seen since the global financial crisis of 2008. Nevertheless, ETFs have held their own and have been observed to be an efficient price indicator in challenging markets.

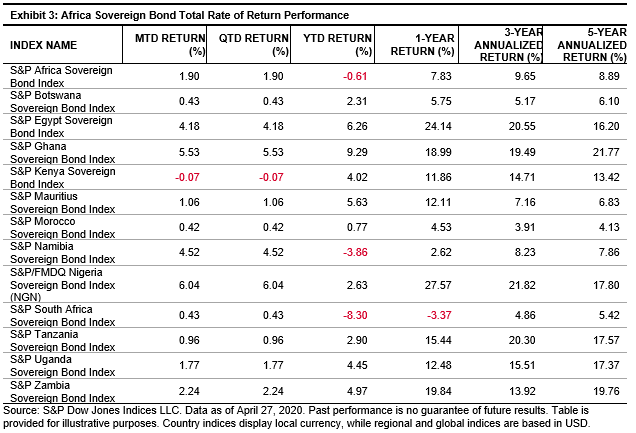

Despite the current economic challenges related to COVID-19, opportunities exist for investment in Africa. Over the past five years, Africa has gone from being a challenge in terms of its financial potential to an enticing prospect for emerging market investors.

A World Economic Forum study mentioned that by 2030, African household consumption is expected to reach USD 2.5 trillion. The study goes on to state: “Nearly half of that $2.5 trillion will be spent in three countries: Nigeria (20%), Egypt (17%), and South Africa (11%). But there will also be lucrative opportunities in Algeria, Angola, Ethiopia, Ghana, Kenya, Morocco, Sudan, and Tunisia. Any one of these countries would be a good bet for companies seeking to enter new markets.”

The African market continues to strengthen its position in the world by developing its economy, manufacturing capabilities, infrastructure, and technology. Additional investments will be required to keep African countries continually growing and achieving future expectations, but the efficiencies of an ETF can assist in making such an investment possible.

The posts on this blog are opinions, not advice. Please read our Disclaimers.