A wise man told me years ago that there are some things you can’t get if you go after them directly. If you’ve ever watched someone trying to sound interesting, you’ll realize the truth of my friend’s observation. There are plenty of interesting people out there, of course, but they achieve that status by pursuing the things that interest them, and their enthusiasm attracts the interest of others.

At least in this respect, portfolio management sometimes imitates life. Factor indices come in many flavors – some tilt toward popularity and momentum, some toward unloved value names, and so on. One helpful division is between risk enhancers and risk mitigators. As the name suggests, risk mitigators have lower volatility levels than the parent indices from which their constituents are drawn. Familiar examples would include such factor families as low volatility, dividend aristocrats, and quality.

One of the remarkable things about these factors is that, over extended periods of time, they’ve all outperformed the S&P 500:

This is remarkable because none of these factors are designed for outperformance. The Dividend Aristocrats comprise consistent, committed dividend growers; Low Vol screens for low historical volatility; Quality looks for balance sheet strength and profitability. All three aim to provide protection in down markets and participation in rising markets; they (usually) outperform when the market falls and underperform when the markets rises.

Yet all three defensive factors have outperformed, at a time when the vast majority of actively-managed portfolios have lagged the S&P 500. They’ve achieved outperformance without going after it. One reason for this result is the way in which dispersion interacts with returns.

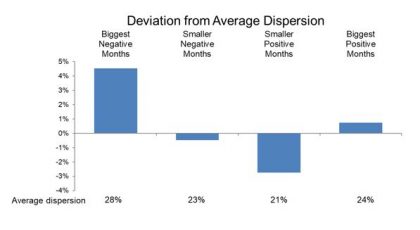

Dispersion measures the degree to which the constituents of an index produce similar results. If dispersion is low, the impact of deviations from an index – whether by active stock selection or factors tilts – is relatively small. When dispersion is high, returns are widely separated, and the opportunity for active managers – or factor indices – to add value grows commensurately. But dispersion varies as the market environment changes:

What the chart above illustrates is that when the market declines, dispersion tends to be high. When the market rises, dispersion tends to be relatively low. That means that defensive factors tend to outperform when the payoff for outperforming is above average, and to underperform when the penalty for underperformance is below average. This asymmetric pattern explains why defensive factors typically capture more of the market’s upside and less of its downside – and, serendipitously, why defensive factors generally outperform over long periods of time.

Readers interested in learning more about defensive factors are invited join our webinar on Wednesday April 29th at 2:00 PM EDT. You can register here.

The posts on this blog are opinions, not advice. Please read our Disclaimers.