John C. Bogle is quoted as saying, “the idea that a bell rings to signal when investors should get into or out of the market is simply not credible. After nearly 50 years in this business, I do not know of anybody who has done it successfully and consistently. I don’t even know anybody who knows anybody who has done it successfully and consistently.”[1]

The current COVID-19 situation has created an unprecedented outlook that calls for reinvention and new solutions. Markets across asset classes are witnessing substantial volatility, which is making investment decisions more challenging. Each asset class with its own characteristics is highlighting trends, which is keeping investors perplexed.

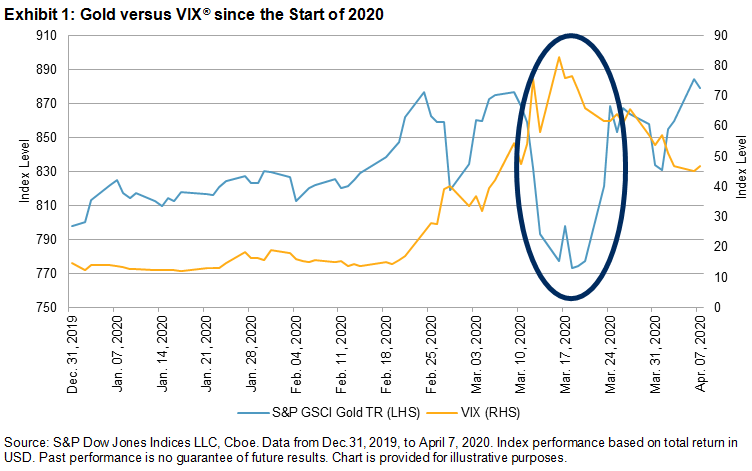

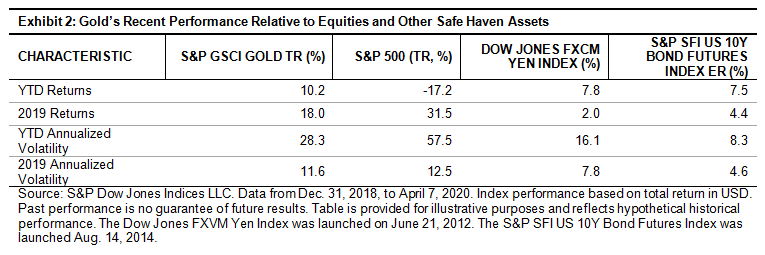

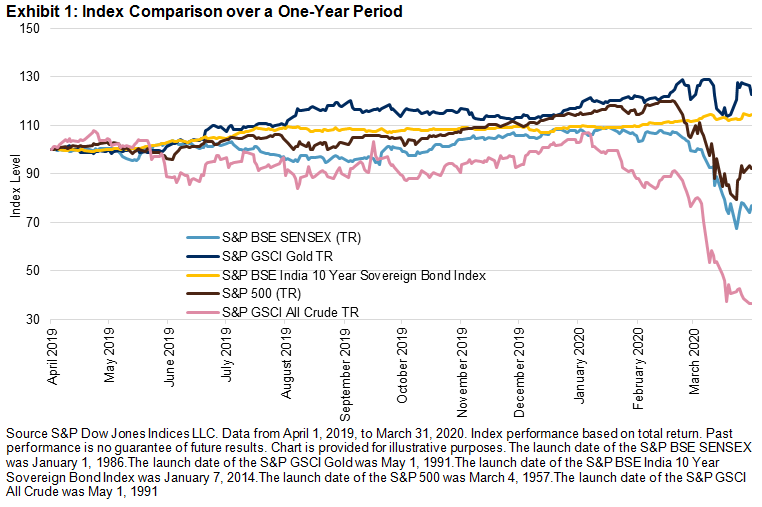

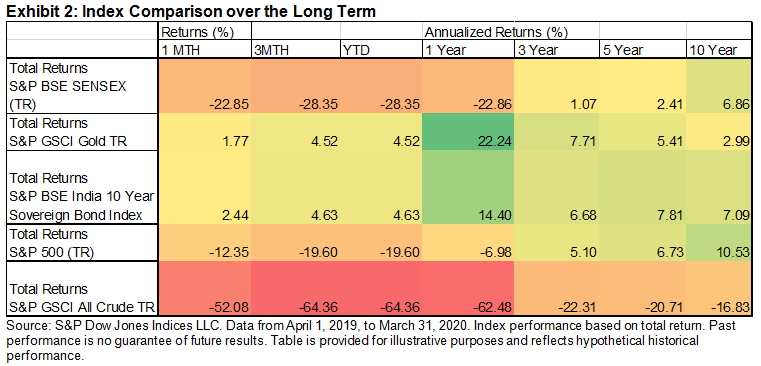

Comparing some global trends with those from India for the one-year period ending March 31, 2020, the S&P BSE SENSEX touched historical lows, just as other global indices such as the S&P 500® have. On the fixed income side, the S&P BSE India 10 Year Sovereign Bond Index has held its ground and been range-bound, though it has also seen some minimal declines. The S&P GSCI All Crude, a subindex of the S&P GSCI that is designed to measure the performance of the crude oil commodity market, recorded its 10-year low on April 1, 2020. The S&P GSCI Gold, a subindex of the S&P GSCI that is designed to measure the performance of COMEX gold futures, rose in March 2020 but with some volatility.

Selecting the best route or time to park funds in such times is a challenge for even the best professionals in the field with years of experience. Passive investing or index-based investing has many benefits that make it an evergreen option in asset allocation. Index-based investing provides allocation to a broadly diversified portfolio at a low cost. An index, based on transparent rules by an independent provider, offers a standard approach without the bias of a fund manager. Passive investing involves the buying and holding of a basket of securities in a particular index in proportion to the securities’ weight in the index, thereby offering protection from concentration risk.

A dilemma faced by many investors is the availability of a plethora of options around them and making the decision of what is the best choice. The best way to counter that is to make the process simple. Indices serve as transparent measures of market compositions and trends, making them essential for building investment confidence. In some cases, indices can make substantial contributions to democratizing market access. Indices define asset classes, geographies, strategies, and themes for the investment community and thereby form the basis of many index mutual funds and exchange-traded funds.

[1] Common Sense on Mutual Funds: New Imperatives for the Intelligent Investor

The posts on this blog are opinions, not advice. Please read our Disclaimers.