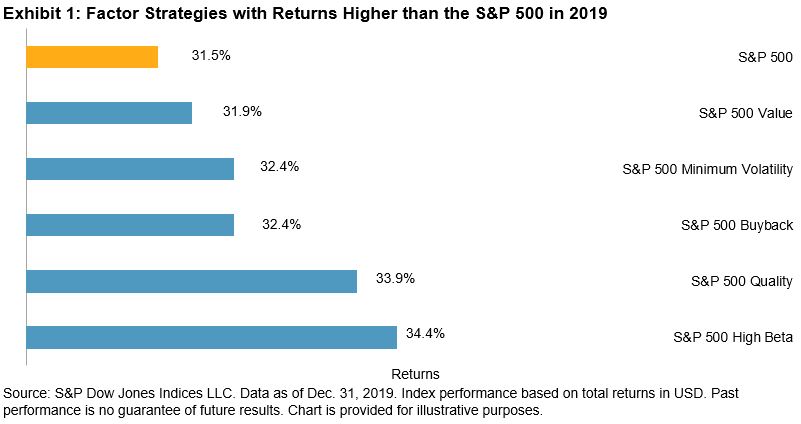

In 2019, U.S. equities posted double digit gains, with the S&P 500® returning 31.49%—its best year since 2013 and second-best in a decade. This continued strong performance highlights the potential difficulty of beating the S&P 500.[1] The question then arises: what strategy (if any) outperformed the S&P 500 in 2019?

Our latest S&P 500 Factor Indices Dashboard details the performance of various passive factor strategies across multiple time horizons. Five factor-based strategies outperformed the S&P 500 in 2019—high beta, quality, buyback, minimum volatility, and value (see Exhibit 1).

We focus on quality—the second-best-performing factor—in this blog. High beta, by definition, tends to deliver higher returns than the broad market in a bullish environment. Because of this, its standing as the best-performing factor in 2019 comes as no surprise. Quality, on the other hand, is a frequently debated factor for which definitions can vary greatly and performance can be cyclical.[2] Therefore, its outperformance in 2019 merits additional insight and analysis.

S&P DJI’s definition of high-quality companies is consistent with Graham and Dodd’s definition of “sustainable earnings power.”[3] We measure quality as a composite score of profitability (ROE), low earnings accruals, and prudent usage of leverage (debt/equity). Back-testing, as well as live performance data, show that over a long-term investment horizon, higher-quality companies in the S&P 500 outperformed lower-quality companies and the broad market on both an absolute and risk-adjusted return basis.[4]

Given that the S&P 500 High Quality Index comprises three fundamental ratios, we sought to understand which ratio contributed the most to the index returns. Exhibit 2 shows the performance of each of the underlying ratios—ROE, accruals, and debt-to-equity—in 2019.

The market rewarded profitable companies handsomely in 2019. ROE was the best-performing ratio of the three (38.2%), followed by accruals (29.8%), and then leverage (28.1%). In fact, the portfolio of the highest ROE companies outperformed the S&P 500 by nearly 670 bps.

Given quality’s performance against the S&P 500 in 2019, we wanted to dig deeper into multi-factor strategies that incorporate elements of quality in their index construction. For instance, the S&P 500 GARP Index—which combines growth, value, and quality scores to arrive at a portfolio of 75 growth securities with relatively high earnings quality and reasonable valuations—kept pace with the S&P 500 in 2019, returning 31.5%. On the other hand, the S&P 500 Quality, Value & Momentum Multi-Factor Index lagged the S&P 500 and returned 26.2%. The index’s underperformance is partly driven by exposure to the momentum factor (26.25%), which returned less than the broad market in 2019.

In sum, 2019 was a strong year for domestic equities. The S&P 500, a market barometer for large-cap U.S. equities, posted its second-best year in a decade. Quality was one of the few factors that managed to deliver higher returns than the S&P 500. Upon deeper examination, we found that profitability was the biggest return contributor to the quality factor, posting significantly higher returns than the S&P 500. While it may seem like 2019 was a difficult period to beat the S&P 500, our blog highlights that passive factor strategies with exposure to quality performed even better than the S&P 500 in 2019.

[1] Chris Bennett, “https://www.indexologyblog.com/2020/01/07/from-hard-to-beat-to-nigh-on-impossible/”

[2] Aye Soe, “https://www.indexologyblog.com/2018/05/23/quality-part-i-defining-the-quality-factor/”

[3] Daniel Ung, Priscilla Luk, and Xiaowei Kang. “Quality: A Practitioner’s Guide?”. S&P Dow Jones Indices.

[4] ibid.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

Taking market performance as a measure, there has been little visible dent to investors’ confidence from the most recent geopolitical flare up. Have market participants, irrespective of asset class, grown complacent to geopolitical risks, or have they decided that the overall threat to the global economy of further incremental deterioration in U.S.-Iranian relations and more broadly, Middle Eastern stability, is relatively contained?

Taking market performance as a measure, there has been little visible dent to investors’ confidence from the most recent geopolitical flare up. Have market participants, irrespective of asset class, grown complacent to geopolitical risks, or have they decided that the overall threat to the global economy of further incremental deterioration in U.S.-Iranian relations and more broadly, Middle Eastern stability, is relatively contained?