One of the main risks for retirees is not having enough inflation-adjusted income in retirement to support their desired standard of living. The S&P STRIDE (S&P Shift to Retirement Income and Decumulation) Indices attempt to solve this problem by focusing explicitly on reducing the volatility of income rather than reducing the volatility of returns.

In order to help market participants track the cost of a stream of inflation-adjusted retirement income, we recently published our first Cost of Retirement Income dashboard. (You can sign up for future editions here.) The dashboard uses the same cost of retirement income measure as our STRIDE indices: the present value of an inflation-adjusted stream of cash flows equal to $1 per year, starting at various retirement dates (vintages) and ending 25 years later.

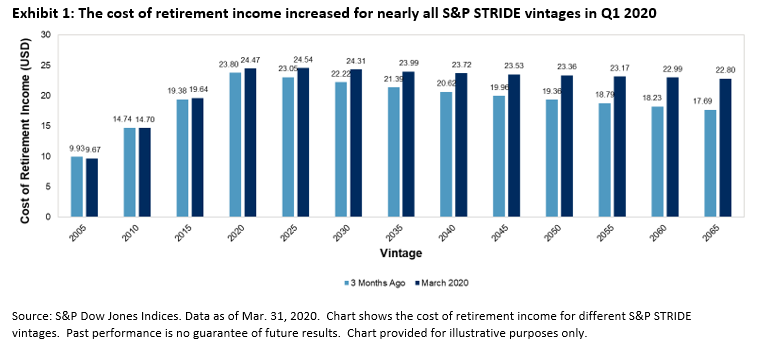

Exhibit 1 shows that the cost of retirement income increased for all but two S&P STRIDE vintages in the last three months. For example, the cost of 25 years of retirement income beginning in January 2025 increased from $23.05 to $24.54 in Q1 2020. Significant market drawdowns in Q1 2020, coupled with declines in U.S. Treasury yields, presented severe challenges for market participants looking to secure a desired level of inflation-adjusted retirement income. Pre-retirees were particularly impacted given the greater sensitivity of longer-dated vintages to real interest rates, which declined as the U.S. Federal Reserve cut its policy rate in response to the spread of COVID-19.

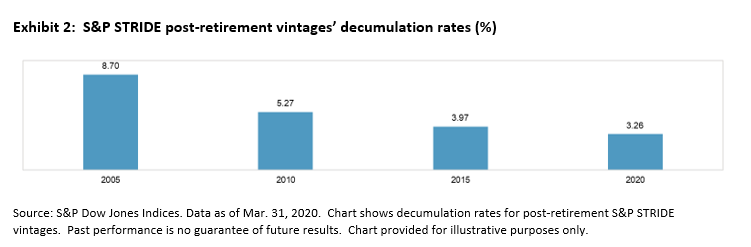

The dashboard also tracks the hypothetical distributions from post-retirement vintages of the S&P STRIDE indices (see Exhibit 2). For example, the annualized proportion of last month’s hypothetical distributions – in terms of decumulation points – to the index’s beginning value was 3.26%. Notably, the decumulation rate is higher than the S&P 500’s 2.34% indicated dividend yield.

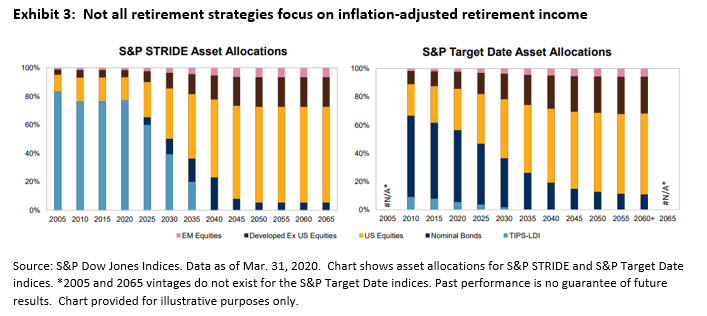

Finally, the dashboard reminds us that not all retirement strategies have an explicit focus on providing inflation-adjusted retirement income. Exhibit 3 shows that nearer-dated S&P STRIDE indices had significantly higher allocations to Treasury Inflation-Protected Securities (TIPS) than the consensus asset mix embodied in the S&P Target Date Indices. For example, the S&P STRIDE 2020 index’s TIPS allocation (77.2%) was 14 times higher than the S&P Target Date 2020 index (5.5%) at the end of March 2020. This is a result of the S&P STRIDE indices’ focus on income rather than return volatility, and it impacts asset allocations across the traditional glidepath approach.

For more information, please see the S&P STRIDE Index Series Methodology and the S&P STRIDE Supplemental Data Guide.

The posts on this blog are opinions, not advice. Please read our Disclaimers.