Active funds generally lagged their passive benchmarks in 2019, but the market environment in 2020 has already shifted radically. Volatility has skyrocketed as the S&P 500® and other indices have fallen. Ironically, it is precisely in a time such as this, when absolute returns are hard to come by, that relative returns might be most readily attainable. This is true not just for traditional stock pickers, but also for active managers looking to express tactical views on the business cycle through sector rotation.

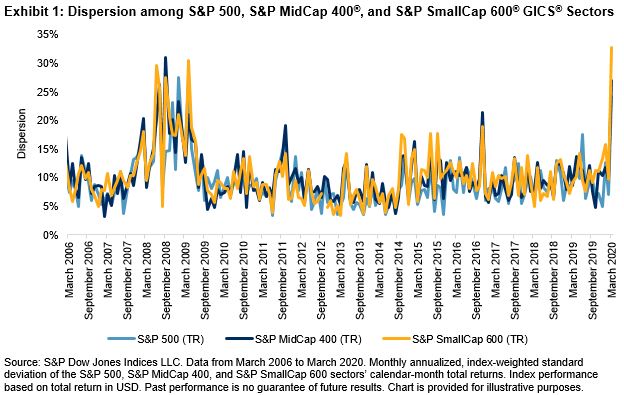

We can analyze the opportunities available by examining changes in dispersion among sectors and industries. The greater the level of dispersion, the more opportunity there is for active managers to display their skill in sector or industry rotation. Exhibit 1 shows that dispersion among S&P 500 sectors more than tripled in March 2020. We see similar trends for dispersion among mid- and small-cap sectors.

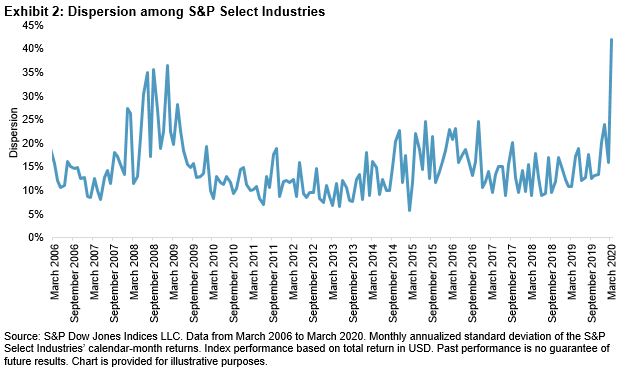

At a more granular level, we observe in Exhibit 2 that dispersion among S&P Select Industries skyrocketed in March, offering immense opportunities for active managers to display skill in tactically rotating among industries.

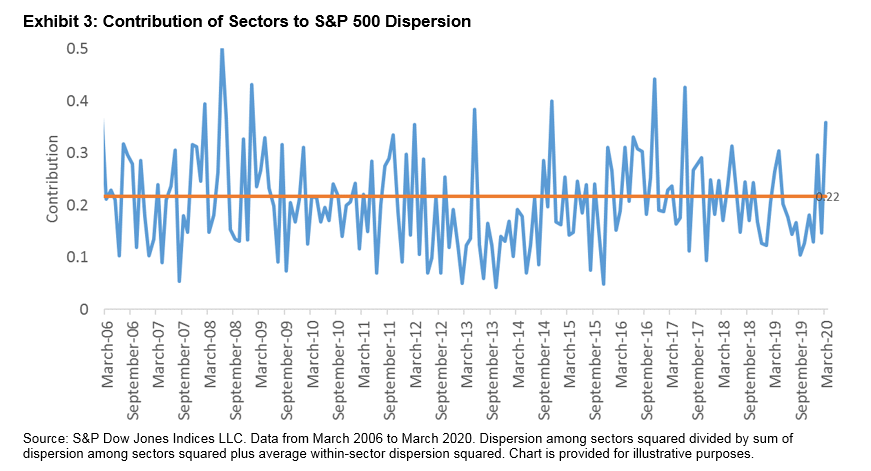

We can further understand the importance of sectors by decomposing total market dispersion into within-sector and cross-sector effects. Exhibit 3 demonstrates that the contribution of cross-sector effects to total S&P 500 dispersion more than doubled in March 2020, rising above its long-term average, implying that the rewards for skillful sector picks are increasing.

While active managers now have more potential to add value through sector and industry rotation, we caution that greater opportunity for outperformance does not equal actual outperformance. There is also greater opportunity for underperformance. Skill and luck will determine whether active managers achieve glory or embarrassment.

The posts on this blog are opinions, not advice. Please read our Disclaimers.