The Communication Services sector turns one year old on Sept. 24, 2019. A year ago, the Global Industry Classification Standard® (GICS®) replaced the old Telecommunication Services sector with a new Communication Services sector, which combined telecom with some companies that had formerly been classified in the Information Technology and Consumer Discretionary sectors. As a result, Telecommunication Services, once the ugly duckling comprising three stodgy phone companies, metamorphosed into a sector that included high-growth companies such as Alphabet, Facebook, and Netflix. Over the past 12 months, the sector outperformed the S&P 500®, up 8.55% versus the market’s 4.22%.

After this change, the average constituent volatility of Communication Services has been higher than that of the old Telecommunication Services. Some investors might therefore assume that the volatility of the new index is also higher than that of its predecessor, but this is paradoxically not the case. We predicted last year that the volatility of the new sector would be roughly the same as the old, resulting from the juxtaposition of two opposing forces: Communication Services’ higher dispersion, which drives volatility higher, is balanced by lower intra-sector correlations, which pull volatility lower.

A year later, our forecast has come to fruition. As seen in Exhibit 1, Communication Services’ average volatility (19.25%) is only slightly higher than that of Telecommunication Services (17.65%), and this increase came at a time when the S&P 500 overall was much more volatile. As predicted, Communication Services has higher average dispersion and much lower correlations than did Telecommunication Services.

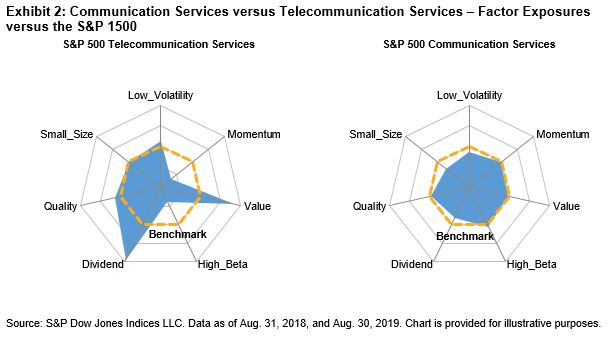

Based on the data from Exhibit 1, we observe that the volatility of Telecommunication Services was 69% higher than that of the S&P 500 in the year prior to the GICS changes. Since then, the volatility of Communication Services has been only 23% higher than that of the market, implying that Communication Services is much more market-like than its predecessor. We can see this firsthand through the factor exposures in Exhibit 2. Telecommunication Services had a high exposure to dividend yield and value. In stark contrast, Communication Services tilts away from dividend yield and low volatility, as well as away from small size, and is relatively more exposed to momentum and high beta. As a result, the sector now behaves more like the market.